What Is An Integrated Audit?

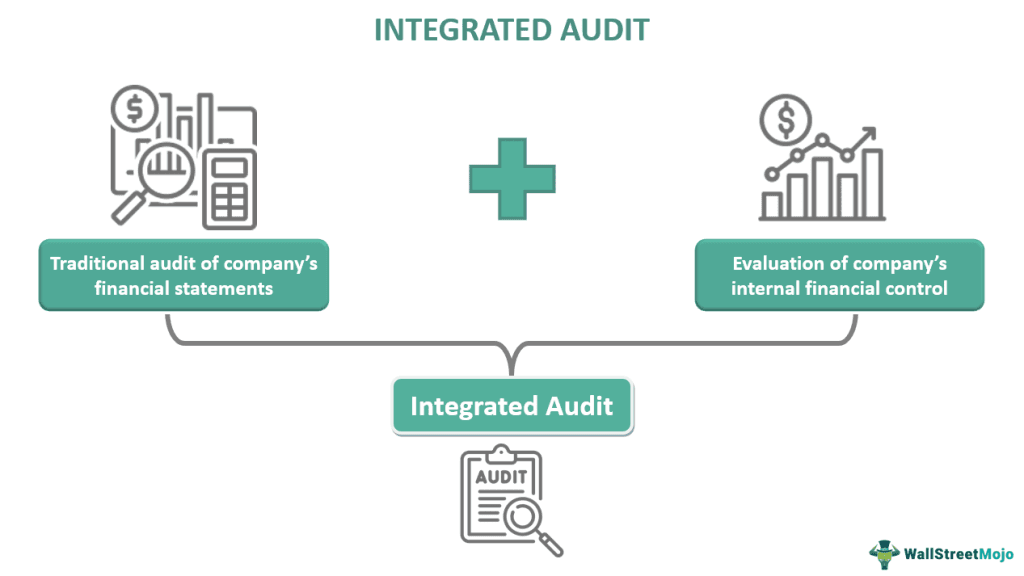

An integrated audit consists of an audit of a company’s financial statements and an assessment of its internal financial control. An integrated audit approach analyzes a firm’s internal controls that affect its financial health. It also helps to pinpoint any significant weakness in a business’s internal controls.

An integrated audit report combines the traditional audit method, where only a company’s financial statements are audited, with an evaluation of its internal economic control. First, the auditor reviews the economic decisions that impact a company’s financial position. In addition, the integrated audit machinery tracks down the deficiencies in a firm’s internal management system.

- An integrated audit is a process where the company’s internal financial control is evaluated along with the assessment of its financial statements.

- This method ensures that the significant weaknesses in the control systems are identified and resolved.

- This audit focuses on determining and eliminating the risks in the control system that can cause material misstatements in the financial records.

- In this audit, the auditor reviews several aspects of the business, which include employee benefits, operations, performance, and information systems. All larger publicly traded companies must perform this audit.

Integrated Audit Explained

An integrated audit is a type of auditing in which a company’s financial statements and internal business controls are evaluated. The integrated audit machinery is a step ahead of traditional audits. In a conventional audit, an auditor assesses a company’s financial records. Then, the external auditor evaluates the accuracy of the balance sheet, cash flow statement, and income statement to find out if there is any material misstatement. This method only highlights any discrepancies in the financial numbers.

However, a firm’s management system also impacts its economic standing. Therefore, the integrated audit approach also reviews the business’s internal financial control system. It involves an extensive understanding of the company’s control systems. The auditor evaluates several aspects of the business operations, employee benefits, performance, and information systems. This process gauges the efficiency of the internal control mechanism and points out any crucial weaknesses in the management system that may affect the firm’s financial numbers.

The auditors prepare the integrated audit report by following procedures that evaluate the firm’s control design and its efficacy. In addition, the standards set by the Public Company Accounting Oversight Board, or PCAOB, require this audit to include the following steps:

- Conducting comprehensive research about the business and its existing control system.

- Determining the areas in the business that pose the most significant material misstatement risks and examining them thoroughly.

- Measuring the company’s size and performance complexity to ascertain how they impact the overall financial control.

- Reviewing the potential risks from fraud that could affect the control system adversely.

Examples

Let us understand the concept with the following examples:

Example #1

Suppose Nordic Powers is a public company that provides power supply to a city. On March 2022, at the end of the fiscal year, the audit reports of Nordic Powers were published. The statements included the following observation and recommendations:

- Observation: Non-maintenance of the worker’s logbook.

- Implication: Non-maintenance of the worker’s logbook makes it challenging to track a worker’s attendance and the work hours they are putting in. The management is lenient in monitoring the worker’s attendance and productivity. This issue may lead to underproductivity by workers. Furthermore, it could increase the risk of absenteeism.

- Recommendation: The management must introduce a systematic procedure to maintain the worker’s logbook. The company policy must include stringent rules regarding absenteeism. The management should officially convey the work hours to all the employees.

This is an integrated audit report example.

Example #2

SAP announced that the entity had filed its Annual Report on Form 20-F for the fiscal year 2022 with the United States Securities and Exchange Commission. It has also announced that its integrated reports are also available online. This report includes the organization’s financial, social, and environmental performance. It is the organization’s 11th published integrated report. This is an integrated audit report example.

Benefits

The benefits of this audit are as follows:

- It helps identify the critical weaknesses in the company’s internal financial control that could lead to substantial misstatements.

- It saves time and cost.

- An auditor’s clean opinion would increase the company’s worth in an acquisition. In addition, it implies an increased sales price as the company has a robust control system.

- It is instrumental in determining the relationship between different business processes. In addition, it helps in understanding how the functions in one process can impact another process.

- It is a crucial tool in identifying the key risk areas in a business.

Integrated vs Non-Integrated Audit

The differences are as follows:

- Integrated audit – this type of audit involves combining the traditional non-integrated auditing method and evaluating a business’s internal financial control. This audit is mandatory for all large public companies. This audit focuses on the control system’s effectiveness, which impacts a company’s economic position or can cause material misstatements in the financial records. In addition, it determines the risks associated with significant deficiencies in the control system.

- Non-integrated audit – this type of audit includes evaluating a company’s financial statements like the income statement, balance sheet, and cash flow statement. All companies need to perform non-integrated audits. This audit focuses on reviewing the transactions that the financial statements constitute. It helps in identifying material misstatements in financial records. The non-integrated audit aims to identify the inaccuracies in the economic numbers.

Frequently Asked Questions (FAQs)

Who is required to have an integrated audit?

Publicly held companies require this audit. According to the Sarbanes-Oxley Act, enacted in 2022, the executives of all larger publicly owned companies must set up, implement and record the business’s internal controls. The auditor performing this audit reviews the reports presented by the management. Smaller public companies and private companies do not require to perform this audit. However, they can opt for this audit as it is time and cost-effective. Furthermore, it increases the company’s sales price in case of acquisition and can be beneficial for attracting investors if required.

Which type of auditor can perform an integrated audit of a public company?

Only a Certified Public Accountant (CPA) can perform this audit in a public company. A company must include the CPA firm’s opinion on the management’s internal control report while filing the annual reports with SEC.

What is an integrated audit top-down approach?

In the top-down approach, the auditor initiates the process by understanding the internal control system’s overall risks over the company’s financial statements. Then they move on to the entity-level controls and the critical accounts and their disclosures.

Recommended Articles

This has been a guide to what is Integrated Audit and its definition. We compare it with non-integrated audit, explain it with its examples, and benefits. You can learn more about from the following articles –