Part of our Shareholder Equity guide

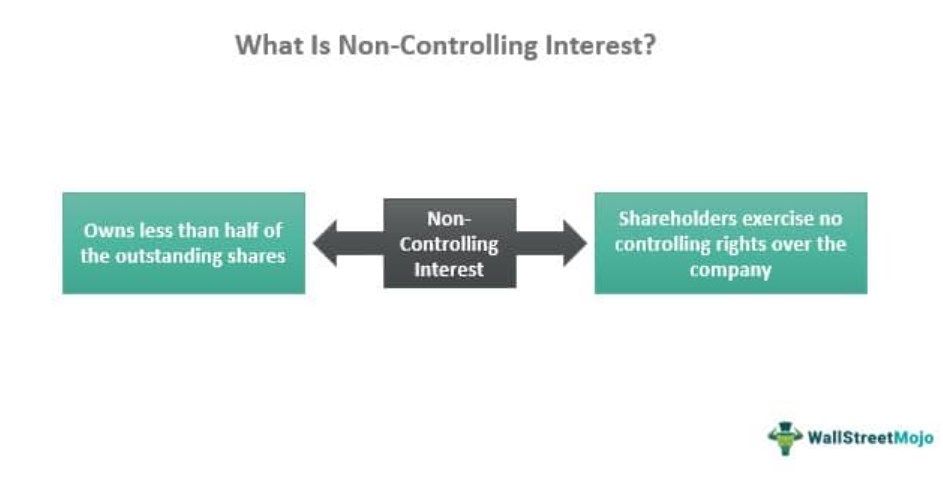

What Is Non-Controlling Interest?

Non-controlling interest refers to the minority shareholders of the company who own less than 50% of the overall share capital and therefore don’t have control over the company’s decision-making process.

Generally, in the case of publicly traded companies, most shareholders are minority shareholders, and only promoters could be categorized as majority or controlling shareholders. In the case of consolidation of accounts, the amount attributable to the minority, based on net assets value, is shown separately as a Non-controlling interest in the Balance Sheet reserves and a surplus of the entity.

- The term “non-controlling interest” describes the company’s minority shareholders. They don’t have power over the corporation’s decisions because they own less than 50% of the total share capital.

- Minority interest is taken into account when the controlling company consolidates its books of accounts. The process of combining the financial accounts of two or more companies into a single set of financials is called consolidation.

- The net asset value of the shares held by the minority shareholders is recognized as a Minority interest in the reserves and surplus in the consolidated financial statements while combining the financial accounts of the subsidiary company with the parent company.

Non-Controlling Interest Explained

A non-controlling interest is where shareholders have ownership of less than half of the outstanding shares. It occurs when an entity, which is a parent company decides to invest and own more than 50% but less than 100% shares of another entity, which is a subsidiary company.

As the name suggests, having an ownership of less than 50% does not make them qualify for controlling rights over it. This is what makes them the minority players in the ownership game.

Types

There are two types – Direct and Indirect.

#1 – Direct

It is one where the minority shareholders get their share in the recorded equity of the subsidiary company. All recorded equity here means both pre and post acquisitions amounts.

For Example:

Company B has reserved as on 31.03.2018, aggregating to $ 550,000. On 01.04.2018, Mr. X bought 10% shares of company B. Since it is a case of Direct Non-controlling interest, Mr. X would be entitled to 10% of pre-existing/past profits of Company B, in addition to the future profits accruing post 01.04.2018.

#2 – Indirect

It is one where the minority shareholders receive a proportionate allocation of post-acquisition profits only, i.e., he would not receive a share in the pre-existing profits of the company.

For Example:

Company A holds 20% shares in Company B, and Company A also acquired 60% shares of Company P, which holds 70% of the shares of Company B. Thus, the shareholding of Company P and Company B would look as under, post-acquisition:

Company P:

- Shares held by Company A: 60%

- Direct Non-controlling interest: 40%

Company B:

- Shares held by Company A: 62%

- Direct Non-controlling interest: 40%

Indirect Non-controlling interest: It is calculated using the direct interest on the Balance Sheet of P ltd, i.e., 40% * 70% = 28%

Examples

Let us consider the following examples to understand the non-controlling interest meaning and type of entry made.

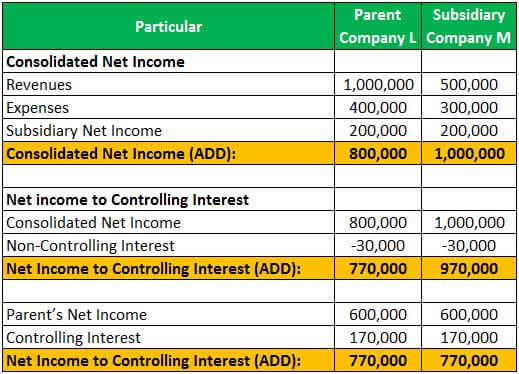

Example #1

Company L acquired 85% of the shares outstanding of Company M. Thus, the remaining shares held by minority shareholders were 15%. At the end of the year, Company M reported revenues of $ 500,000 and expenses of $ 300,000, whereas Company L reported revenues of $ 1,000,000 and expenses of $ 400,000.

Net income of Company L and M can be computed as under:

Allocation of net income of Company M, between controlling and non-controlling interest, is as under:

Consolidated net income can be computed as under:

Example #2

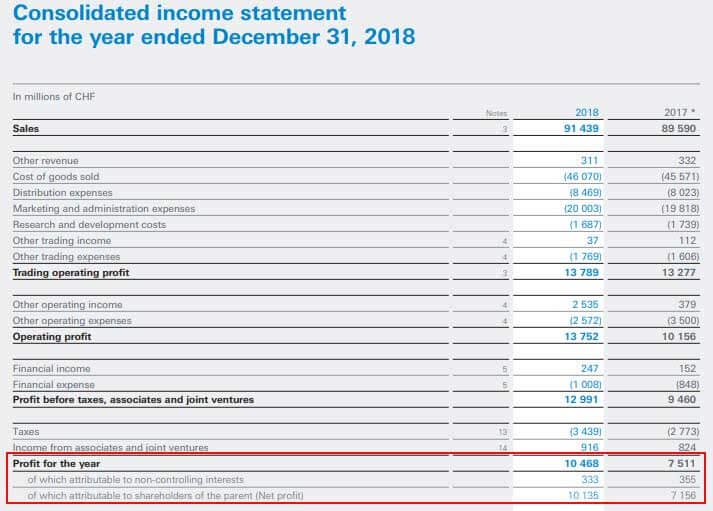

The following extract is from the Financial statements of Nestle for the year ended 31st December 2018, which shows the profit is attributed to the non-controlling interest and shareholders of the parent:

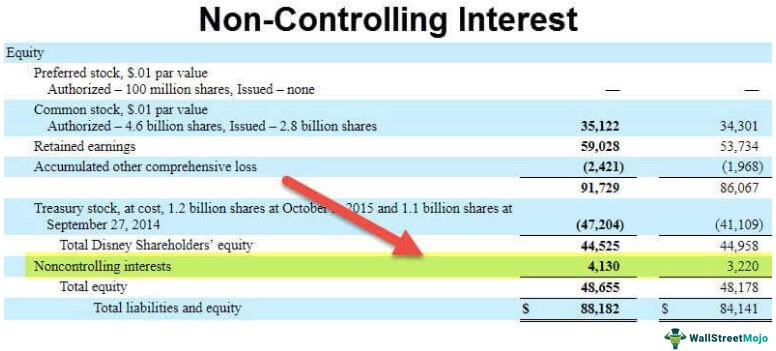

Following is the extract of the consolidated balance sheet of Nestle, which shows the amount attributable to Non-controlling interest:

Source: www.nestle.com

It thus represents the amount attributable to shareholders who are not the company’s significant shareholders and have no authority over decision-making in the company. The amounts attributable to NCI are shown separately in the consolidated financial statements, as it is the amount that doesn’t belong to the parent entity and is attributable to minority shareholders.

Accounting on the Balance Sheet

→ Explore all 93 Balance Sheet articles

Non-controlling interest on the balance sheet is a consolidation of books of accounts by the holding company. Consolidation refers to the process by which financial statements of two or more companies are combined to form one set of financials.

Consolidation applies when an entity holds the majority stake in another entity, known as the subsidiary entity. As consolidation combines sets of financial statements, it allows stakeholders, like investors, creditors, lenders, etc., to view the combined financial statements of all three entities as one.

While consolidating the financial statements of the subsidiary company with the holding company, the net assets value of the shares held by the minority shareholders is recognized as a Minority interest in the reserves and surplus in the consolidated financial statements.

Frequently Asked Questions (FAQs)

What does the accounting term NCI mean?

When an organization does not own 100% of a subsidiary organization, it is said to have a non-controlling interest (also written as a minority, non-controlling, or non-controlling interest). It is because the organization owns only a portion of the subsidiary.

What kinds of interests have non-controlling status?

Non-controlling interests typically fall into one of two categories: direct non-controlling interests or indirect non-controlling interests. The total recorded equity of a subsidiary (including pre-and post-acquisition sums) is allocated proportionately to each direct non-controlling interest.

What is the balance of non-controlling interest?

NCI can be a debit balance in this scenario. the parent stockholders hold equity between NCI and the parent’s shareholders. Both contracting parties are powerless to control.

Recommended Articles

This article is a guide to What is Non-Controlling Interest and its Definition. Here we discuss the two types of non-controlling interest on the balance sheet and its accounting while consolidating the books with examples. You can learn more about accounting from the following articles –