Part of our Options Trading guide

What Is Interest Rate Option (IRO)?

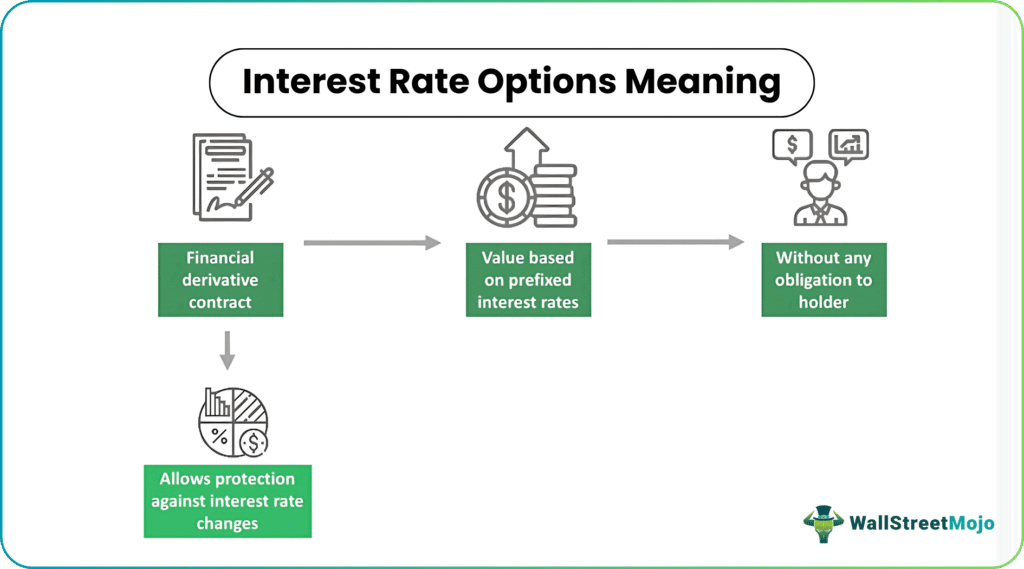

An Interest Rate Options (IRO) refers to a financial derivative contract giving the holder the right to trade the underlying interest rate instrument at the prefixed rate on a future date without any obligations. It provides protection against any possible interest rate changes and allows the holder benefit from them.

Any entity or investors exposed to interest rate fluctuations use IRO commonly. It has wider implications for investors by deferring the harmful impact of interest rate fluctuation on borrowing costs, financial performance, and investment returns. The settlement of IRO usually takes place in cash, but investors could exercise interest rate options like European-style provisions.

Key Takeaways

- Interest Rate Options (IROs) are financial contracts that grant the holder the right, but not the obligation, to trade an underlying interest rate instrument at a predetermined rate in the future.

- They are useful for hedging against the risk of interest rate fluctuations or taking advantage of potential changes in interest rates, providing protection and potential benefits to investors.

- IROs encompass various types used in financial markets, such as Caps, Floors, Collars, Swaptions, Bermudan Options, and Digital Options.

- Interest Rate Options (IROs) offer advantages such as risk management, customization, lower upfront cost, and speculative trading opportunities. At the same time, their disadvantages include the potential loss of value and counterparty risks.

How Does The Interest Rate Option Work?

Interest rate options are financial instruments that derive their value from changes in interest rates. These options are typically linked to interest-rate products such as treasury notes. They are traded on exchanges where they are offered in various formats and types to cater to different investor needs. Investors opting for call options get the right to trade in the absence of any obligation.

Their values get linked with interest rate instruments like futures contracts and treasury bonds. Any investor who buys the option of interest rate call option gets the right to buy the underlying asset based on its strike price before it expires. It proves beneficial to them as they get set to buy the assets at a lower prefixed price when the interest rate rises.

Furthermore, any investor who buys the interest rate put option gets the right to sell the underlying asset based on its strike price before it expires. It proves beneficial to them as they get set to sell the assets at a higher prefixed price when the interest rate falls, but still are not completely risk-free options.

Moreover, investors get the flexibility to hedge against the risk of interest rates toward any future interest rate movements in interest rate options. Many investors and analysts use it to manage their bond portfolios’ interest rate exposure, safeguard their investments against interest rate fluctuations and take the benefits from forecasted market trends.

Types

The different types of IROs in financial markets include caps, floors, collars, swaptions, digital options, Bermuda options, etc.

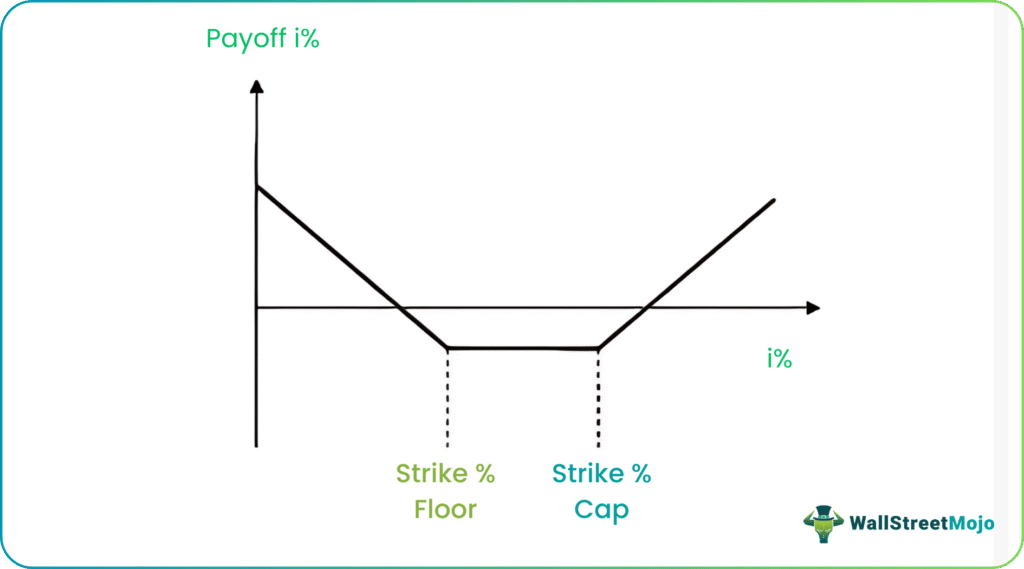

#1 – Caps

It allows the buyer to have the right to get payments if a reference interest rate exceeds more than the prefixed or cap rate for a certain timeframe. One can use it for protection from rising interest rates on floating-rate loans or investments.

#2 – Floors

It allows the buyer to have the right to get payments if a reference interest rate falls below the prefixed or cap rate for a certain timeframe. One can use it for protection from falling interest rates on floating-rate loans or investments.

In the diagram below, the payoff for caps and floors is explained. In the diagram, if the interest rates move or cross the strike prices on either side, the trader earns a profit if the payoff compensates and is more than the premium paid, which is a combined amount of cap and floor. This is a strangle strategy, and the trader can earn a profit if the interest rate is very volatile. However, if the interest rates are stable and move within the strikes, the trader will lose the premium. The underlying asset can be any type in this case.

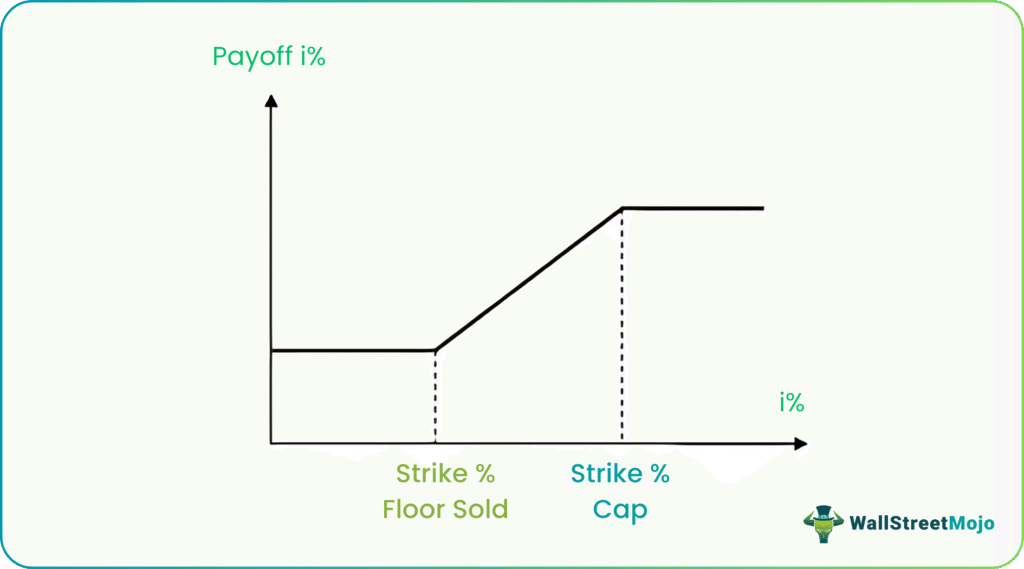

#3 – Collars

It has the combined feature of both floors and caps. It works by simultaneous buying of a cap and selling of a floor. As a result of this strategy, investors limit their upside and downside interest rate risk under a specified timeframe.

In the diagram below, which shows the payoff for the collar, in case of a rise in the interest rates and it crosses the strike of the cap, the collar buyer will have to pay a fixed interest rate that will be equal to the cap’s strike price. In case of a fall in interest rates, if the rate falls below the strike of the floor, the collar buyer will again pay a fixed rate, but it will be lower.

#4 – Swaptions

It means an option on an interest rate swap. Investors get the right to enter into an interest swap at predetermined future dates and terms. It gives the flexibility of the investors to speculate or hedge against unpredictable interest rate movements.

#5 – Bermudan Options

These IROs have to be exercised at particular dates prior to their expiry date. They have more flexibility than the European option, which can be exercised only at expiration.

#6 – Digital Options

Here IRO gives out a fixed payout to the investor only if certain specified conditions of interest rate get met. During the term of the option, if the interest rate hits a specific level, then the option of one-touch pays out.

Examples

Let us study a few examples to understand the topic.

Example #1

Suppose a manufacturing company wants to maintain stable cash flows. It limits its interest expense even during the rise of interest rates. Therefore, it buys multiple interest caps options so that it gets protection if the reference interest rate on its debt goes beyond a certain level.

Example #2

Let us assume a homeowner wants to ensure predictable mortgage payments and also get protection against lower interest rates. In that case, the homeowner would opt for mortgage rate protection by buying minimum interest guaranteeing an interest rate floor. As a result, whenever the interest rate falls under the floor rate, the homeowner gets payments to compensate for the difference.

Advantages And Disadvantages

Let us discuss the advantages and disadvantages of IRO in the points below.

The following are its advantages:

- It is beneficial as a tool for managing interest rate risk. It helps investors reduce their investment from a negative movement of interest rate, thus saving their profitable positions.

- It can also be customized to various needs, like selecting expiration date and strike rate, adding extra flexibility for designing risk management strategies.

- It requires lesser upfront cost in comparison to other instruments of interest rate hedging instruments like interest rate swaps. As a result, a wider range of market investors get access to it quite easily.

- IRO benefits traders with the opportunity to make profits through the provision of speculative trading by the use of anticipated interest rate movements.

The following are its disadvantages:

- IRO loses its value if its interest rate movement does do to occur as expected before its expiration date within a particular time frame.

- IRO value steadily declines over time if the interest rate does not change or remain stable, leading to losses to investors related to the option holder.

- For full utilization of IROs, one must have the knowledge of complex strategies and options pricing models that may be quite difficult for new or inexperienced market participants or investors.

- IRO carries the burden of counterparty risks just like other derivative contracts, which means that the option buyer is dependent on the seller for the fulfillment of contractual obligations. If the seller defaults on an obligation, the option holder loses their investment.

Frequently Asked Questions (FAQs)

1. How are interest rate options priced?

IRO gets priced based on different mathematical models like the Black 76 Model, which is the most widely used one. It acts as an extension to the Black-Scholes model for pricing interest rate futures. Moreover, it uses the below factors to price:

– the option’s strike price

– underlying interest rate

– time to expiration

– the volatility of interest rates

Furthermore, other models, such as the BGM model & the HJM model, also get used for pricing of interest rate options, but they use far more complex market conditions and interest rate dynamics.

2. How do interest rate options benefit investors?

Investors can enjoy various advantages through interest rate options. These options serve as tools for hedging against and speculating on interest rate fluctuations, enabling investors to mitigate risks and capitalize on market changes. Moreover, they offer flexibility when building investment portfolios, providing opportunities for strategic positioning and diversification.

3. What is the difference between interest rate options and futures?

Interest rate options and futures differ in terms of their contractual obligations. Interest rate options provide the holder with the choice to buy or sell an underlying interest-rate asset without any obligation to do so. In contrast, futures contracts impose a binding obligation on both parties involved to buy or sell the underlying asset at a predetermined price and date.

Recommended Articles

This article has been a guide to what is Interest Rate Options (IRO). Here, we explain the topic in detail with its examples, types, advantages, and disadvantages. You may also find some useful articles here –