Stockholder’s Equity Statement Definition

A stockholder’s equity statement is a financial report which forms part of the financial statements that capture the changes in the equity value of the company (i.e.) increase or decrease in equity value from the commencement of a given financial period to the end of that period. It contains share capital and retained earnings.

Stockholders’ equity is the company that has settled the value of assets available to the shareholders after all liabilities. It indicates the company’s worth. It is also known as Shareholder’s Equity. It provides information relating to equity-related activity to the users of financial statements and it is one of the financial elements used by analysts to understand the company’s financial progress.

Components of Stockholder’s Equity Statement

The following are the components of the stockholder’s equity statement.

#1 – Share Capital

It contains the capital invested by the investors of the company. The investors’ ownership is indicated by way of the shares/stock. Companies generally issue common stock or preferred stock. Movement or changes in the capital structure and value is captured in the Stockholders’ equity statement.

Common Stock

The common stockholders have more rights in the company in terms of voting on the company’s decision, but when it comes to payment, they are the last ones on the priority list. In case of liquidation, common stockholders will be paid only after settling the outside liabilities, then bondholders and preference shareholders. The remaining will be paid to the common stockholders.

Preference Stock

The preference stock enjoys a higher claim in the company’s earnings and assets than the common stockholders. They will be entitled to dividend payments before the common stockholders receive theirs. They don’t carry voting rights.

Treasury Stock

Treasury Stock is the value of shares bought back/ repurchased by the company. It acts as a reduction to the share capital. It is the difference between Shares issued and shares outstanding.

Video Explanation of Shareholder’s Equity Statement

#2 – Retained Earnings

Retained earnings are the total profits/earnings of the company accumulated over the years. The company uses it to manage the working capital position, procure assets, repay debt, etc. These are not yet distributed to the stockholders and retained by the company for investing in the business.

A profitable company retained earnings will show an increasing trend if not distributed to shareholders. The stockholder’s equity statement captures the movement of retained earnings.

Retained Earnings= Retained Earnings at the beginning of the period (+) net income /loss during the current reporting period (-) Dividends paid to stockholders.

#3 – Net Profit and Dividend Payment

Net profit/ Net income is the money earned by the company in the reporting period. It adds up to the opening retained earnings available. The company makes dividend payments from the amount available in retained earnings. The dividend payment is at the company’s option, and it is not mandatory.

#4 – Other Comprehensive Income

Investments made foreign currency transactions and hedging transactions. It captures the unrealized gains and losses that are not reported in the income statement. It is not realized, and it is a national impact. It may arise because of pension liabilities.

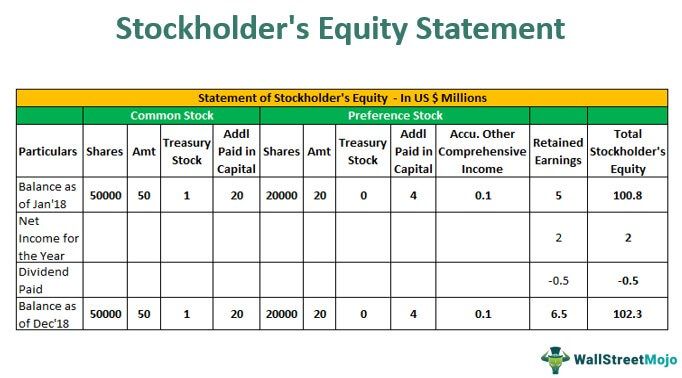

Example of Stockholders Equity Statement

Below is an example of the Stockholders equity statement.

The following are the details about XYZ Corp as of 31st December 2018.

| Particulars | In ($) |

|---|---|

| No of Common Stock | 50000 |

| No of Preferred Stock | 20000 |

| Stock Price (Common Stock) | 140 per share |

| Stock Price (Preferred Stock) | 120 per share |

| Par Value (Common Stock) | 100 per share |

| Par Value (Preferred Stock) | 100 per share |

| Treasury Stock – Common Stock | 100000 |

| Retained Earnings at Beginning | 500000 |

| Net Income of Year | 200000 |

| Dividend Paid | 50000 |

| Accu. Other Comprehensive Income | 10000 |

Stockholders Equity Statement Format

Below is the format of the stockholder’s equity statement

Calculation of Additional Paid-in Capital of Common Stock

- =50000*40

- =2000000

Calculation of Additional Paid-in Capital of Preferred Stock

- =20000*20

- =400000

Conclusion

Stockholders’ equity statements form part of the balance sheet in the financial statements. The three main events which impact the equity of the business are changes in the share capital either by the issue of shares or by selling or repurchasing, changes in retained earnings which are influenced by current period profit or loss, and the dividend payout; and the movement of other comprehensive income.

Users of financial statements can understand the movement of equity value. It helps to understand the business’s performance, financial health, and the company’s decisions in terms of share capital, dividend, etc.

Shareholders’ equity can either be positive or negative. If it is positive, it indicates that the company’s assets are more than its liabilities. If negative, it indicates that the liabilities are more than its assets. Negativity may arise due to buyback of shares; Writedowns, and Continuous losses. If the negativity continues for longer, the company may go insolvent due to poor financial health.

Financial health can be understood by analyzing the statement of equity as it gives a broad picture of the performance.

Recommended Articles

This article has been a guide to Stockholders Equity Statement and its definition. Here we discuss components of the stockholder’s equity statement and an example. You may learn more about accounting from the following articles –