Part of our Mergers & Acquisitions guide

What is Reverse Morris Trust?

Reverse Morris Trust is a technique used in mergers and acquisitions to avoid the tax implications by spin-off that results in reorganization and transfer of assets and liabilities in a tax-efficient manner. It is very prevalent in the United States.

- Reverse Morris Trust is an approach that one may use during mergers and acquisitions to avert the tax implications by spin-off that gives an outcome in reorganization and transfer of assets and liabilities in a tax-efficient manner. It is usual in the United States.

- Morris Trust was built as a result of the U.S. Court of Appeals ruling in 1966 in the case of Commissioner v. Mary Archer W. Morris Trust.

- The parent company must possess at least 80% of the subsidiary’s assets, which they want to derive.

How does Reverse Morris Trust Work?

- There must be a parent-subsidiary structure.

- By fulfilling various conditions provided under Section 355 of the Internal Revenue Code. The parent company wants to sell the subsidiary tax-efficiently.

- Parent company spin-offs the subsidiary to the shareholder of the parent company.

- A subsidiary company is merged with the 3rd company. Such a 3rd party must look smaller as compared to a subsidiary company. As a result minority stake will be less than 50%. The assets to be acquired are spun off and promptly merged with the buyer.

- 51% of the shareholding of the merged company must be owned by the original parent entity’s shareholder only.

However, one must ensure that all conditions prescribed under Section 355 should be adequately fulfilled for at least two years post-merger.

History

In the world of mergers and acquisitions, each structure is either the result of some loophole in the law or based on the judgment by the court of the land. For example, Morris Trust structures result from a ruling by the U.S. Court of Appeals in 1966 in the case of Commissioner v. Mary Archer W. Morris Trust.

Based on this judgment, people started leveraging the advantages. As a result, the Internal Revenue Service formulated section 355 in 1977 for the Reverse Morris trust giving various conditions needed to be complied with for getting the tax benefits.

Example

To comply with the tax requirement, ABC Co. planned the Reverse Morris structure in the following manner. First, ABC Co. wanted to sell its XYZ Co, owning manufacturing operations for a specific geography, to PQR Co. Accordingly, ABC CO. transferred assets of XYZ Co. to a separate subsidiary. Also, ABC Co. sells the share of XYZ Co. to its shareholders.

Then, ABC Co. completed a Reverse Morris Trust reorganization with PQR Co. As a result, shareholders of ABC Co. had the majority stake in the newly merged company. In contrast, PQR Co.’s shareholders and management will have a minority stake in the company.

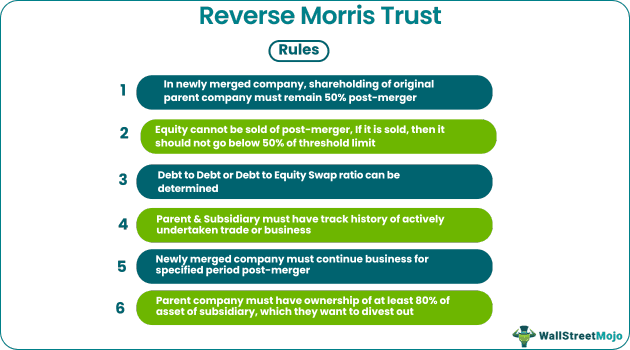

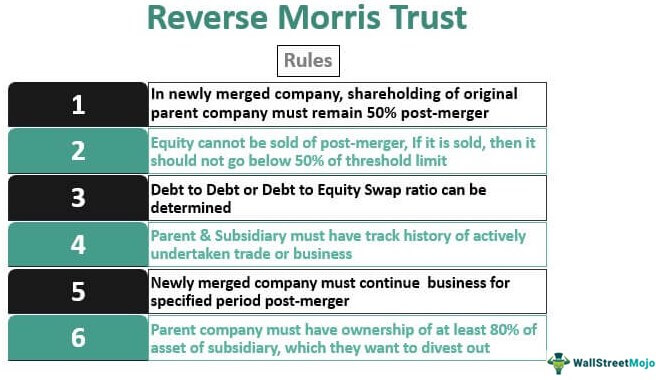

Rules of Reverse Morris Trust

The following conditions under Section 355 must be met to be eligible for tax benefits under the Reverse Morris Trust structure:

- Ownership test: In the newly merged company, the shareholding of the original parent company must remain 50% post-merger.

- The company cannot sell equity post-merger. It should not go below 50% of the threshold limit if sold.

- Determining the Debt to Debt or Debt to Equity Swap ratio can be done. However, that must be within the given criteria of 50% ownership.

- Parent and subsidiary companies must have a history of actively undertaking trade or business for five years before initiating the Reverse Morris Trust structure.

- The newly merged company must continue the business for a specified period post-merger.

- Asset test: The parent company must own at least 80% of the subsidiary’s assets, which they want to divest out.

Advantages

- Avoids Corporate Taxes on Gains – Main advantage of the Reverse Morris Trust structure is that it enables the way of doing tax planning within the legal boundaries of tax laws.

- Consideration Paid is the Acquirer’s Stock – Buyer can give the consideration even in equity shares, making it very attractive in the corporate world.

- Net Book Value of the Transmission Assets Remains the Same for Old and New Owner – Under the Reverse Morris Trust structure, the company must transfer all the assets to the 3rd company at the book value. As a result, it does not result in an irrelevant increase in the overvaluation of the assets.

- Silent Movement of Assets –The assets’ spin-off will be happening immediately after selling the shares to the shareholders. It will enable the free movement of assets as no further approvals are needed.

- There will be the same management, employees, workforce, and assets with the same ideology to do the business. It will not have any impact on the day-to-day business of the business. Hence, it is considered a silent transfer of subsidiaries.

Disadvantages

- Limited Scope for Issue of Consideration in Cash – Consideration will be restricted to equity as the equity threshold must be maintained. Hence, there exists a minimal scope of monetary issuance of consideration.

- Limited Scope for Issue of Equity Post-Merger – 51% of the ownership of the original shareholder of the parent company is needed to be maintained thoroughly post-merger. It does not give room to issue post-merger as well.

Frequently Asked Questions (FAQs)

How does a Reverse Morris Trust work?

A Reverse Morris Trust (RMT) is a tax-optimization approach in which a company desires a spin-off. Later, they sell assets to an interested party without bearing any taxes on profits earned from the disposition.

What is Reverse Morris Trust transaction?

A Reverse Morris Trust transaction is a divestiture form that blends a spin-off or split-off with a merger. Since it is complex, it is a business divesting tax-efficient method. In addition, this structure is completed under U.S. tax laws.

Is a Reverse Morris Trust good for shareholders?

Reverse Morris Trust enables the parent company to elevate funds and help lessen the debt while selling unused business assets. Such a transaction is helpful to exceedingly indebted companies.

What is the Reverse Morris Trust vs Morris Trust?

The difference between a Morris trust and a Reverse Morris Trust is that the parent company amalgamates with the target company in a Morris trust. Moreover, no subsidiary is formed.

Recommended Articles

This has been a guide to Reverse Morris Trust and its definition. Here we discuss examples, rules, and how it works along with advantages and disadvantages. You may learn more about financing from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.