Table Of Contents

What Is An Offset Account?

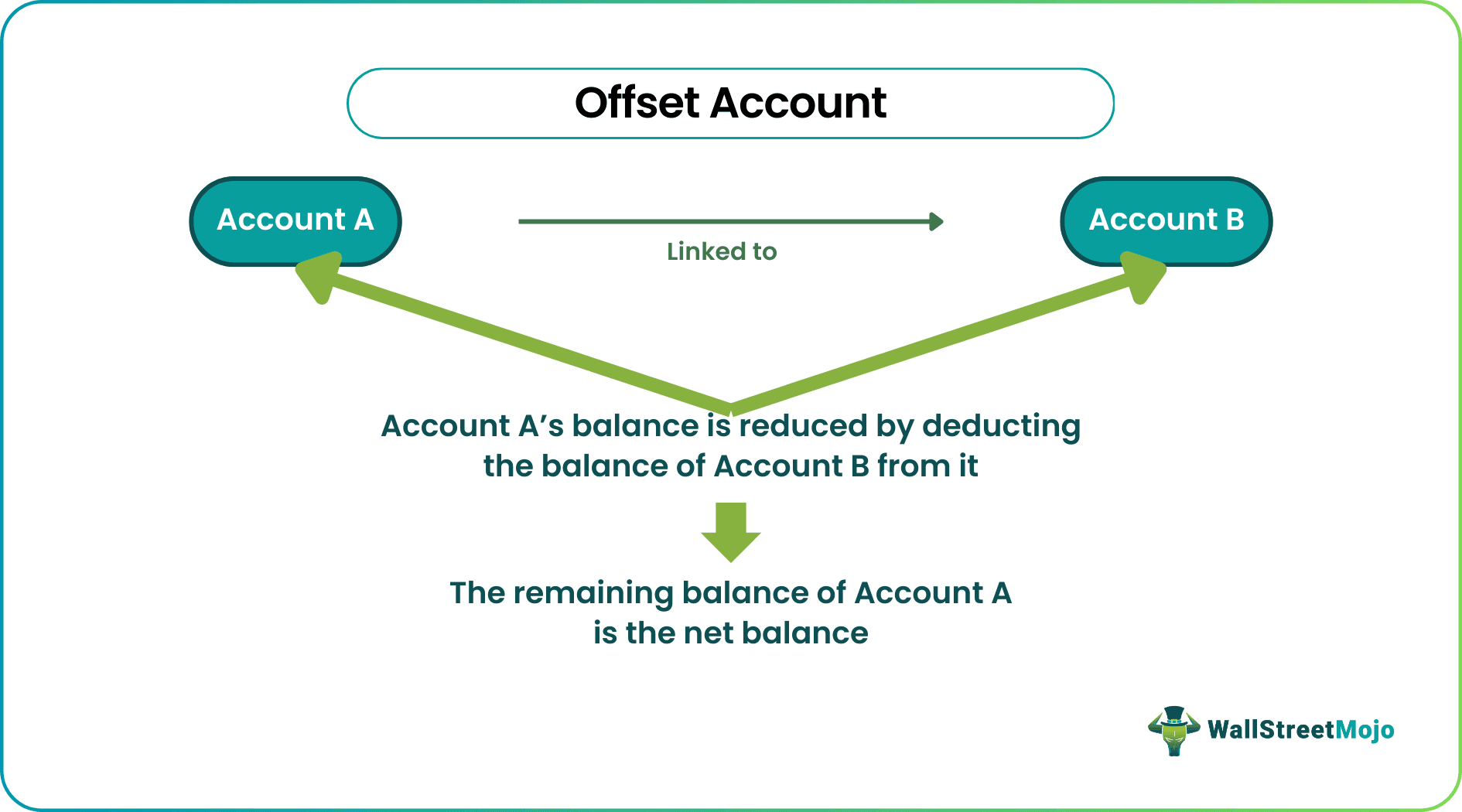

An offset account is an account that is directly or indirectly related to another account, and it reduces the balance of the related account to give us a net balance which is used for calculation, valuation, interpretation, and application in financial statements as the requirement may arise in the course of business and statutory requirements.

An organization looking for a robust accounting process must include offsetting accounts reporting to present an accurate and fair view of financial statements. They are also the result of globally accepted accounting principles for accurate reporting of financial numbers, as reporting offset accounts helps in a better understanding of the financial statements of any organization.

Table of contents

- What Is An Offset Account?

- Offset accounts are used to reduce the balance of the related account, such as allowance for bad and doubtful debts, and drawings.

- Offset accounts can be related to various accounts, such as fixed assets, sundry debtors, capital, and inventory on hand. They are used to show reductions in specific accounts and help create reserves.

- Offset accounts help in the quick calculation of net book value, aid in preparing annual reports, facilitate audits and filings, and are globally accepted as a standard accounting practice.

- Implementing offset accounts can be time-consuming and may require a robust accounting system.

How Does Offset Account Work?

The offset account in accounting is a type of account in the financial system where two accounts are paired with one another and ne offsets the other. As a result, the balance of the main account reduces as the second account balance is offset using the main account. We get a net balance in the main account.

In the balance sheet, both the accounts can be shown as a single item by merging them.

An ideal example of such a case is the allowance for bad debt, which is set off against the accounts receivable balance and we get a net receivable balance.

Nowadays, with the development of a computerized accounting system, it is easy and quick to prepare and maintain the offset account in accounting as the system does all the calculations. However, an accountant or person in charge must ensure that any change in the value of the assets due to revaluation or impairment must be considered. Accordingly, the value of such an account will change.

Also, with IFRS (International Financial Reporting Standards) asking to report the offset account in a particular way, the accountants must be updated with recent changes to how it should appear in the books of accounts.

Due to globalization, companies are not restricted to only their home country. They are spreading into different countries in order to expand and grow. Therefore it is important to prepare financial statements that match the global standards and compatible with the rules and regulations of the countries in which the company is operating.

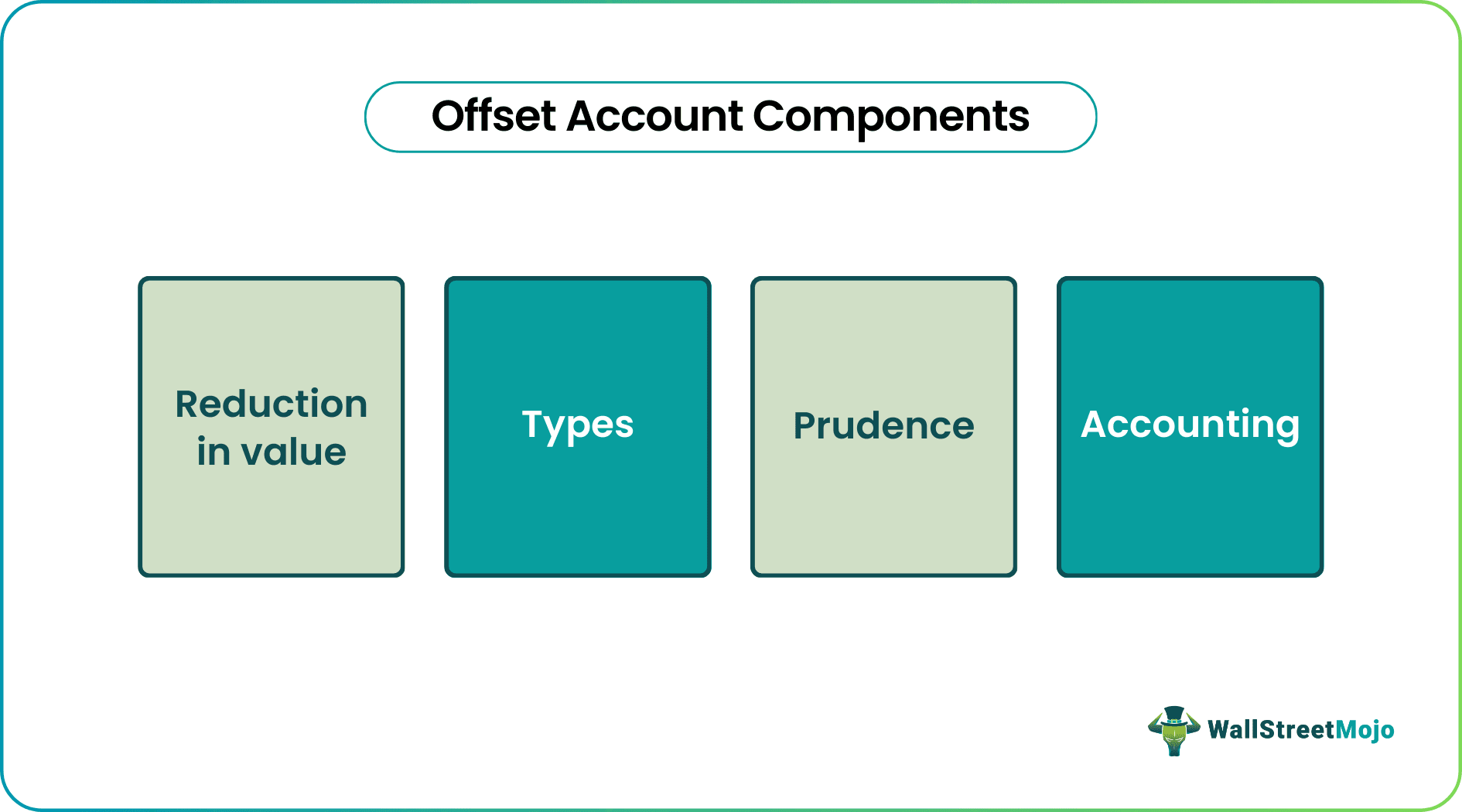

Components

#1 - Reduction in Value

Offset account limit, in most cases, goes on to reduce the balance of the account to which it is related. For example, let's say we expect 3% of our total receivable of $100,000 has gone bad, so we show $3,000 ($100,000*3%) as provision for doubtful debts, which is a reduction from debtors value and here provision for doubtful debts is offset account for debtors. Also, in a sole proprietorship business, when the owner withdraws the funds for personal use, called drawings, it is an offset account for capital. So, for example, if the initial contribution from the owner was $50,000, and the withdrawal for the period is $5,000, it is interpreted that the net capital balance is $45,000 ($50000 – $5000).

#2 - Types

Accumulated Depreciation, allowance for bad and doubtful debts, and Drawings are examples that relate to Fixed Assets, Sundry Debtors, and Capital, respectively. Provision for obsolete Inventory is also an example that reduces the balance of Inventory on Hand.

#3 - Prudence

Financial statements must show an accurate and fair view of the picture. So, it is always prudent to show this account separately, and at any point, it gives us the netbook value explaining what the actual cost was and how much of that has been depreciated. It also helps create reserves, and later any change in the expected number can be adjusted through allowances and reserves.

#4 - Accounting

Let us understand how the accounting entry is posted for the offset account limit and how it is shown in the books. First, let us consider that ABC Ltd. recently bought machinery for $200,000, and it plans to depreciate the machinery over five years by using the Straight Line Method. In this case, the depreciation each year for this machinery will be $200,000/5 = $40,000.

Accounting

By the end of the first-year machinery, the balance will be $200,000, and accumulated depreciation will show $40,000. By the end of 2nd-year, the machinery balance will still be $200,000, and accumulated depreciation will show $80,000. The netbook value of the machinery by the end of the first year will be $160,000 ($200,000-$40,000) and $120,000 ($200,000-$80,000) by the end of the second year. This method helps a third person identify what the book value was at the time of purchase and the remaining value of an asset. If we just show $120,000 as an asset in the third year, it will be challenging to understand whether $120,000 is all new purchases or the remaining value of an asset. This account helps all the stakeholders understand the financial numbers accurately.

Example

Let us look at an offset account example to understand the concept. This concept is used in the banking sector for interest calculation on the loan amount. The net loan amount is calculated by deducting the balance in a savings account from the loan account, and this net balance is used for interest calculation for the month or year as agreed by the bank and customer. For example, let's say Mr. Ricky has taken $400,000 as a mortgage loan from Bank of America in Washington DC, and he recently received $100,000 from sale proceeds of property in Georgia. He has kept $100,000 in the bank account linked to his loan account with Bank of America. As the net balance of the loan is $300,000 ($400,000 – $100,000), the bank will charge the interest only on $300,000 for that period. In this offset account example, a $100,000 balance is a savings account that offsets the loan balance and reduces the interest liability of Mr. Ricky.

Benefits

- The purpose of offset account is to help in quick calculation of net book value. Since one account is offsetting the other the value we get is a net amount which is easy to interpret and use.

- The annual reports are prepared for various parties; some of them might not be accounting versed; they help identify the reduction in total value. This is important because here the accountant is able to present a clear picture of why the value of a particular account has gone down. This also helps the department in the auditing purpose.

- The purpose of offset account is to help in audit facilitation and annual filings. As mentioned in the above point, this process helps in the audit purpose because a clear, step by step accounting is done to understand and keep record of how the balance of one account has reduced.

- It is a globally accepted policy to maintain offset accounts to show related accounts' reduction and net balances.

Limitations

- It is a time-consuming process. This is because it is compulsory to prepare two separate accounts but then again the set off has to be done against the correct account. Such processes require meticulous calculation and error free implementation which takes time.

- Many organizations find it challenging to implement. because it requires clear knowledge and understanding about the accounting process and a strong system

- Need a robust accounting system; else, operational difficulties may arise. If the accounting system is not transparent, clear and if it cannot be easily handled or used, them the accounting department will not be able to implement the process and prepare the required accounts.

Offset Account Vs Redraw

- The former is a separate account in itself but the latter is not a separate account.

- The former is not necessarily related to loan but the latter is related to the loan.

- The redraw account offers a facility but offset account offers a process of accounting.

- The tax implications are different fro both of them.

- The redraw account reduces the interest part of the loan, whereas the offset account does not help in such cases.

Frequently Asked Questions (FAQs)

An offset account is a transaction account linked to a mortgage account that allows the balance in the account to offset against the outstanding mortgage balance, reducing the interest payable on the loan. On the other hand, a savings account is a deposit account that allows individuals to save money and earn interest on the deposited funds. Still, it is separate from a mortgage or home loan and does not directly offset the loan balance.

An offset account is a transaction account linked to a mortgage account where the balance in the account offsets the outstanding mortgage balance. On the other hand, extra repayments refer to additional payments made towards the principal amount of a mortgage or home loan, which directly reduces the outstanding loan balance.

A home loan offset account is a specialized transaction account linked to a mortgage account. The balance in the offset account is offset against the outstanding balance of the mortgage to reduce the interest payable on the loan, effectively reducing the interest cost and shortening the loan term.

Recommended Articles

This article has been a guide to what is Offset Account . We explain it along with example, benefits, differences with redraw account, accounting & components. You can learn more about accounting from the following articles –