Part of our Balance Sheet guide

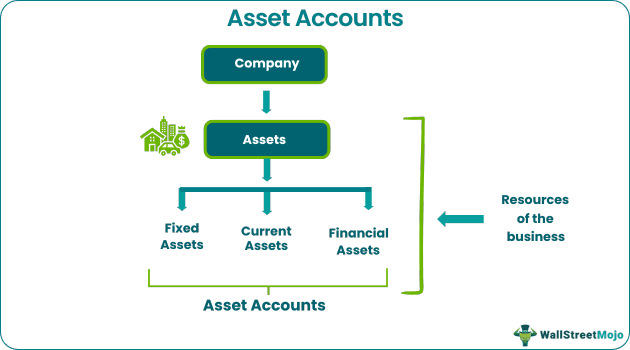

Asset Accounts Definition

Asset Accounts are used to identify the exact usage of stakeholders’ capital (Debt + Equity). They are reported at book values and are depreciated/amortized in the case of fixed assets and provisioned/expensed for current assets in the P&L.

It shows the stakeholders what the business owns and informs them about its resources through a summary in the balance sheet. These include items like cash, building, goodwill, plant and machiney inventory, accounts receivable, etc. At the end of every financial year, each balances are closed and transfer to the next year as opening balance.

- Asset accounts are employed to pinpoint the precise use of stakeholders’ capital (debt plus equity). In the P&L, they are provisioned/expensed for current assets and depreciated/amortized for fixed assets. They are presented at book values.

- It’s crucial to comprehend how investors compare the asset accounts of different companies to those of the industry to spot operating patterns if you understand how asset changes are reflected on the Financial Statements.

- It is typically regarded as “CAPEX” and an investment the business hopes will result in substantial profits. The life cycle of the industry and the potential return on capital are considered when deciding whether or not to incur Capex.

- Both Non-current and Current Assets are used to report the financial assets account. Determining whether an investment is long-term or short-term is the purpose of the word current.

Asset Accounts Explained

Asset accounts are the items tht show the stakeholders what assets the company owns as resources. Assets Accounts belong to the stakeholders, who are the debt and equity investors in the company. It is the responsibility of an investor to look at the assets reported by the company and understand its way of conducting business and if it will maximize value to shareholders in the future.

Many companies are analyzed based on the asset accounts list they have on the books. The most common example is banks, as the bank’s intrinsic value is the interest it can generate from giving loans. Hence all these loans are assets for a bank, and the value of the bank is determined by its Price to Book ratio relative to other banks.

The book in this context is the book value of equity, which is the book value of assets.

Changes in current and non current asset accounts asset values on a company’s books have to reflect in either the Profit and Loss Statement or the Cash Flow Statement. An example would be if accounts receivable increased on the books; it meant an outflow of cash on the Cash Flow Statement. Similarly, if inventories decreased in the books, it means an inflow of cash due to products getting sold. A decrease in the gross block is expensed on the P&L through depreciation, and an increase in the gross block is reflected by Capex capital expenditures under the Cash Flow Statement.

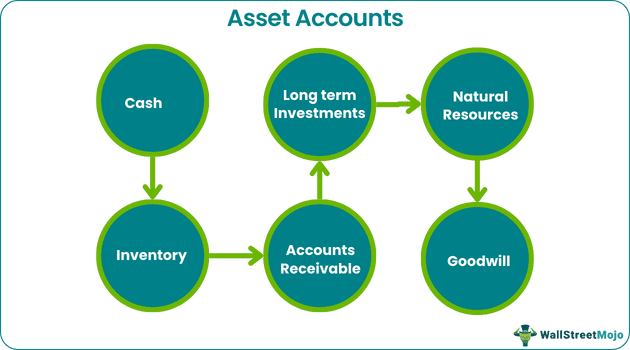

List Of Asset Accounts

Given below is an asset accounts list.

- Cash

- Short Term Investments (Cash Equivalents)

- Accounts Receivables

- Inventory

- Prepaid Expenses

- Long term Investments

- Property Plant & Equipment

- Natural Resources

- Intangible Assets like Patents / Copyrights

- Goodwill

Examples

Let us understand the concept with some examples.

Example #1

Once we understand how changes in assets reflect on the Financial Statements, it is important to understand how investors look at asset account format of individual companies and match them with the industry to identify operating trends. For example, we can compare companies operating across different industries and compare how much $ of revenue a tech company generates for every $ of capital invested vs. a manufacturing company.

Example #2

We can also compare companies operating in the same industry as Walmart, Target, and Costco to determine which are converting products to cash the fastest and most efficiently. Investors can also identify trends across the entire industry. E.g., An agrochemical company’s receivables could be continuously increasing due to the declining profitability of farmers. Such a trend would be visible across the Balance Sheet of the entire spectrum of agrochemical companies, and it helps an investor identify that the industry is going through stress.

Types

Fixed Assets Account

- Also known as Non Current or Gross Block. These are investments made by the company in tangible and intangible assets, which the company believes will generate revenues in the future.

- Tangible assets include property, machinery, equipment, land, and buildings. Intangible assets include patents, registrations, trademarks, and software.

- It is generally treated as “CAPEX” and is an investment that the company believes will generate meaningful retained asset accounts. A decision to incur Capex or not is based on the industry’s life cycle, as well as the return on capital that can be generated.

How To Analyze?

- The fixed asset can be used to compare companies operating in the same industry and different industries. E.g., a company with an asset-light model like recruitment could generate equal revenues as a manufacturing company, requiring lots of investment in plant, machinery, etc. It gives the company the asset-light model a high asset turnover ratio, measured by Sales/Average Non-Current Assets.

- However, the company generating higher revenue per dollar of non current asset accounts doesn’t need to be a better investment. Manufacturing brings with its stickiness and a sustainable advantage; hence an investor must look at the overall scheme of things and retained asset accounts in the balance sheet and not one line item while making an investment decision.

Current Assets

- The current asset includes working capital investments for inventory, receivables that need to be collected from customers, and other liquid assets like current investments, fixed deposits, cash, and bank balances.

- Working capital is essential for every business and is necessary to carry out all the operations effectively. A company’s bargaining power can impact its working capital requirements.

- Suppose the company commands superior pricing power over its customers and suppliers. In that case, it will be able to collect cash from its customers first and then pay its suppliers later, which will result in a positive net working capital.

How To Analyze?

- Current assets account to reflect what is going on with the company’s day-to-day operations. The amount is reported once every quarter in the SEC 10-Q filing in public entities. It is extremely important to look at current assets as it indicates whether growth in revenues is being translated into cash or not. Most analysts make the mistake of ignoring the Balance Sheet and focusing on the P&L. Do not be that one!!

- So, if a company’s P&L indicates that it has grown revenues by 35% YoY and the receivables have also increased by a similar proportion, the company has sold all its products on credit and has not yet collected the cash. The increase in receivables is an asset account format that the company believes will materialize in the future. It is a common practice in companies operating across working capital-intensive industries. In that instance, we must compare firms by examining their cash conversion cycle (days in receivables + days of inventory on hand – days in payables).

Financial Assets Account

The financial assets account is reported under Non-current as well as Current assets. The idea of the word current is to determine if it’s a short-term investment or a long-term investment. Generally, liquid investments are reported under current assets, whereas non-liquid investments are reported under Non-current assets. Other [types of assets include goodwill and deferred tax liabilities.

Frequently Asked Questions (FAQs)

Why is the asset account deducted?

Natural debit balances exist for both assets and expenses. It indicates that positive asset and expense values are debited, and negative balances are credited. For instance, a journal entry upon receiving $1,000 in cash would also include a $1,000 debit to the balance sheet’s cash account because cash is increasing.

What causes credit to the liabilities account?

Liability accounts are sections of the company’s books that display its debt. When a liability account is debited, the amount owed by the company is reduced (i.e., the liability increases). When a liability account is credited, the amount the company owes (i.e., increases the liability).

How come a cost is credited?

A portion of the amount is now recorded in an expenditure account whenever an adjustment is made to defer (until a later accounting period). Reclassify a sum from the incorrect expense account to the right account while making a corrective entry.

Recommended Articles

This article has been a guide to Asset Accounts definition. We explain it along with examples, its various types, and a list of such accounts. You can learn more about accounting with the following articles –