What Are Non Current Assets?

Non Current Assets are long-term assets bought to use in the business, and their benefits are likely to accrue for several years. These Assets reveal information about a company’s investing activities and can be either Tangible or Intangible.

Examples include Fixed Assets such as Property, Plant, Equipment, Land & Building, Long-term investment in bonds and stocks, goodwill, patents, trademarks, etc. They are not repeatedly purchased in a year and benefit the entity by earning income for a long term, which is more than a year. However, they cannot be converted to cash easily..

- Non-Current Assets are long-term investments made for use in the firm and are likely to produce advantages for several years. These assets, which might be actual or intangible, provide insight into a company’s investing activity.

- An intangible asset may be created internally by the company or purchased separately (through mergers vs. Acquisitions, etc.). Examples of intangible assets are goodwill, patents, trademarks, etc. The cost or revaluation model records intangible assets in the balance sheet.

- Any future revaluation gain would be included in the income statement to the same amount as the loss that had been previously disclosed. Revaluation Surplus, the excess revaluation gain over the initial loss, is recorded in the shareholders’ equity.

- Any business needs non-current assets to function. They serve as the engine that keeps the company operating smoothly. Businesses in capital-intensive industries, including oil production, telecommunication, automotive, etc., typically have a higher proportion of long-term assets in their asset base than those in the financial sector.

Non Current Assets Explained

Non current assets are the ones that an entity purchases for the purpose of gaining benefits for more than one year. They cannot be converted to cash easily.

Non Current Assets are an integral part of any business. They act as the wheels for the smooth running of the business. However, the portion of the asset base comprising long-term assets varies industry-wise. Usually, Capital Intensive Industries, such as Oil Production, Telecommunication, Automotive, etc., will have a higher composition of their asset base of long-term assets than companies in the financial sector.

Accounting for non current assets is done over a number of years and they are shown in the balance sheet of the entity, which represents the years for which they can be used. These type of assets are also known as long term assets and has to be capitalized, not expensed.

The total non current assets can be calculated by adding values of all the non current assets displayed in an entity’s balance sheet. These assets are disposed of over time due to their operational efficiency and wear and tear loss. Thus disposal of non current assets is an integral part of the business, in which the depreciation is taken in total and subtracted from the cost price. After the sale, the difference between the sales price and the cost price is the profit of selling the asset.

Video on Non-Current Assets

Types

Non Current Assets are usually classified into three parts:

#1 – Tangible Assets

Assets that physically exist, i.e., which can be touched. Tangible Assets are usually valued at Cost Less Depreciation. Tangible Assets Examples include Land, Property, Machinery, Vehicles, etc. However, it is worth noting that not all Tangible Assets depreciate. For example, the land is often revalued over a period in the Balance Sheet of the Company. Also, have a look at Net Tangible Assets

#2 – Natural Resources

These assets have an economic value derived from Earth and are used up over time. Examples include Oil fields, mines, etc.

#3 – Intangible Assets

Assets that do not physically exist but have economic value fall under this category. For an asset to be categorized as Intangible, the following criteria must be satisfied:

- It must be Identifiable.

- The organization must have the means to obtain economic benefits from such an asset.

An intangible asset can be generated internally by the business or acquired through separate purchases (through mergers vs. Acquisitions, etc.). Intangible Assets Examples include Goodwill, Patent Trademark, etc. Intangible Assets are recorded in the Balance Sheet according to the cost or Revaluation Model (Discussed in detail below). However, it is pertinent to note that Goodwill is not amortized but tested for impairment at least annually. An impairment loss is recognized in cases where the carrying value exceeds the intangible asset’s fair value.

Examples

Let us look at some examples of non current assets.

#1 – Property Plan And Equipment

Property, Plant, and Equipment (PP&E) are long-lived non current assets used to produce or sell other assets.

The cost of PP&E includes all expenditures (transportation, insurance, installation, broker cost, search cost, legal cost) that are necessary to acquire and ready for use. In addition, if the plant is constructed, all the material, labor cost, overheads, and interest costs during construction are included in the Cost of PP&E.

#2 – Natural Resources

These include natural resources like Oil and Gas, Metals like Gold, Silver, Bronze, Copper, and more.

source: bp.com

#3 – Intangible Assets Like Patents, Copyrights, etc

“Other intangible assets” examples primarily include corporate intellectual property such as patents, trademarks, copyrights & business methodologies. Intangible Assets on the balance sheet are recognized only when bought from an external entity, not if they are developed internally. Note that “other intangible assets” are amortized.

source: Alphabet SEC Filings

As noted above, Google’s assets example includes intangible assets worth $3847 million and $3307 million in 2015 and 2016, respectively.

#4 – Goodwill

When one company buys another company, it buys more than just assets on a balance sheet. It’s also buying some intangibles, like the quality of the employees and client base, reputation, or brand name. Therefore, it implies that the firm purchasing another business pays more than the fair market value of the business assets. If the excess purchase price cannot be attributed to patents, brands, copyrights, or other intangible assets, it is recorded as Goodwill.

source: Amazon SEC Filings

We note above that Amazon’s assets example includes Goodwill of $3759 million and $3784 million in 2015 and 2016.

#5 – Long Term Investments

When an investor buys securities in the financial markets, they purchase with the hope that they will appreciate and pay a return.

Alphabet’s non current asset example of long-term investments includes non-marketable investments of $5,183 million and $ 5,878 million in 2015 and 2016.

Purchase of Debt Securities like loans or bonds

- The company records the purchase as an investment on its balance sheet

Purchase of Stock / Shares

- If shares of another company are purchased and have a controlling interest (usually owning more than 50%), then the company needs to consolidate (combine) its accounts with the other company.

- If the company does not own a controlling interest, it must include the shares as investments on its balance sheet.

#6 – Other Long-Term Assets

These items are given in many financial statements, whose explanation needs to be included. For example, there is a need to know the “Other Assets” proportion to “Total Assets.” If it is significant, an analyst may want to clarify the same with the management after studying the total non current assets and their explanations.

Accounting

| Non Current Asset | IFRS | US GAAP |

|---|---|---|

| Property, Plant, and Equipment | Cost Model or Revaluation Model | Cost Model |

| Intangible Assets | Cost Model or Revaluation Model. Research cost is expensed, and the development cost is capitalized | Both Research and Development Costs are Expensed |

Cost Model Approach

Under this model, a non current asset is reported at amortized cost. Amortized Cost is computed by subtracting Accumulated Depreciation, and amortization from the Asset’s Historical Cost. Historical cost is the total cost of the asset, including purchase price and any other cost incurred to get the asset ready for use, such as installation.

Let’s understand the same with an example:

- ABC purchased Plant and Machinery on 01.4.2017 for $100000 and spent Rs 5000 on installing the same. Depreciation for the year is $9500. Under Cost Model, Plant and Machinery will be reported for $95500 (100000+5000-9500) on 31.03.2018.

Revaluation Model Approach

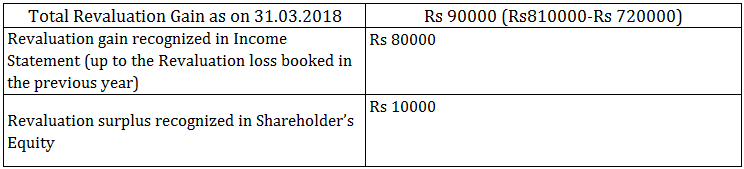

Under this approach, an asset is reported at the Fair value less any accumulated depreciation. If initial Revaluation results in a loss, the initial loss is recognized in the Income Statement. Any subsequent non current assets revaluation gain would be recognized in the Income Statement to the extent of the previously reported loss. Surplus revaluation gain beyond the initial loss is recognized in the Shareholder’s Equity as Revaluation Surplus.

Let’s understand the same with an example:

ABC purchased Plant and Machinery on 01.4.2016 for Rs 800000. As of 31.03.2017, the machinery had a fair value of Rs 720000. As of 31.03.2018, machinery had a fair value of Rs 810000. In such a case, as per the Revaluation Model, non current assets revaluation gain will be reported as follows:

Disposal of non current assets is through sale, in which the profit or loss is the difference between the cost and the sale price.

Non Current Assets Vs Current Assets

Non current assets are the ones that are bought for the business’ long-term benefit and current assets benefit the business for the short term. The basic differences between them are as follows:

| Non Current Assets | Current Assets |

|---|---|

| Provide long-term benefits. | Provide short-term benefits. |

| Cannot be converted to cash easily. | Can be converted to cash easily. |

| They meet long-term needs. | They help in running the day-to-day business operations. |

| They are valued at cost less depreciation. | They are valued at market price. |

| They include property, machinery, plant, building, etc. | They include cash, account receivable, and Inventory. |

Frequently Asked Questions (FAQs)

What are non-current assets and assets?

Current assets, or those that can be swiftly sold and used for a company’s immediate needs, are referred to as short-term assets. Noncurrent Assets are long-term investments with a lifespan of more than a year. Current assets include cash, marketable securities, inventory, and accounts receivable.

What does “non-current asset” mean?

Non-current assets are things a company owns that can’t be quickly turned into cash in a year. Another name for them is long-term assets. Non-current assets are for the business’s long-term usage and are anticipated to contribute to revenue generation.

What are fixed and non-current assets?

Fixed assets, or non-current assets, are assets that are difficult to turn into cash. For example, non-current assets might include tangible items like real estate and machinery and intangible ones like investments and intellectual property.

Recommended Articles

This article is a guide to what are Non Current Assets. We explain it with examples, accounting entries, types, and vs current assets. It is also necessary to have a look at the following articles to learn more about basic accounting –