Part of our Risk Management guide

What Is Basis Risk?

Basis risk is the financial risk traders take when they hedge a position by entering a contrary position in a derivative, for example, a futures contract. This risk arises in the case of an imperfect hedge, i.e., when the hedge cannot offset losses in an investment.

To quantify the risk, traders must consider the market price of the hedged financial asset and deduct the contract’s futures price. There are different types of basis risk, like location, price, and calendar. Introducing this risk in a scenario may mean that an alternative hedging technique would lead to a better result. Traders accept this risk to hedge price risk.

- Basis risk meaning implies a risk that materializes when perfect hedging is impossible. In the case of investments involving large quantities, this risk can significantly impact the eventual losses or gains.

- There are four types of basis risk — location, price, calendar, and product quality.

- This risk in insurance is the possibility that a person buys an insurance policy, but the amount that the insurer pays them in the case of a claim does not equal the total cost of the claim event.

- The spread or difference between futures and spot prices may narrow or widen.

Basis Risk Explained

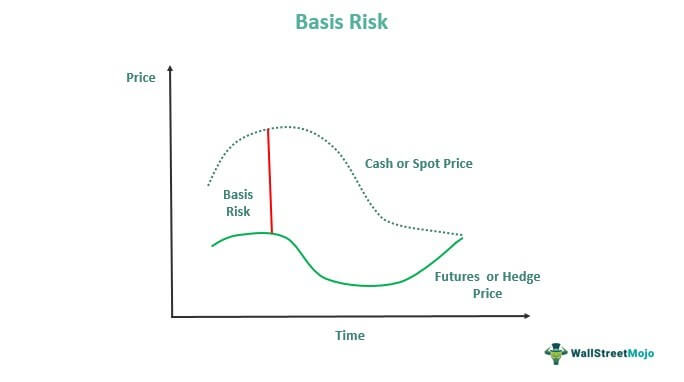

Basis risk meaning implies the potential risk that comes to light because of mismatches in a hedged position. In other words, when a variation exists between the futures or hedge price and the spot or cash price of the hedged underlying asset at any given time, the variation is the basis, and the associated risk is the basis risk.

Thus, the basis is the relationship between an underlying asset’s futures and cash prices. The variation occurs when the security in the hedged asset is not identical to the futures contract’s underlying financial assets. A variation might also occur if the hedging horizon does not perfectly match the futures contract’s maturity period. As noted above, in the case of large investments, the basis risk can have a significant impact on the final gains or losses.

The price spread or difference between the futures and cash prices may either narrow or widen between when the initiation of a hedging position occurs and when the trader liquidates it. When the hedged asset and the underlying assets of the hedging instrument are identical, the basis will be 0 at the time of maturity.

When traders enter a futures contract to hedge against the price fluctuations in the market, they change the price risk into basis risk, which is a systematic risk. Systematic risk arises from the uncertain nature of financial markets. Usually, as a futures contract nears the expiry date, the futures contract’s price moves toward the cash or spot price. Nevertheless, individuals must remember that there is no guarantee that the basis spread will narrow.

Besides securities trading, this risk exists in insurance. In the case of insurance, this risk is the possibility that an individual purchases an insurance policy, but the amount they get in a claim is not the same as the overall cost of the specific claim event. In simple terms, it refers to the possibility that the amount received by the insured from an insurance policy does not match what they thought they would receive as a payout.

Types

Basis risk in derivatives is of four types. Let us look at them in detail.

- Calendar: This risk arises when the futures contract’s expiry date is different from the selling date of the cash market trade.

- Location: Typically, this risk arises in the commodity market where the actual delivery location of the spot market and that of the futures market differs.

- Product Quality: When the qualities or properties of a financial asset are not the same as the asset represented by the derivatives contract, this risk materializes.

- Price: This risk materializes when the price movements of the financial asset and the futures contract are not in sync at the start and end of a trade.

Examples

Let us look at some basis risk examples to understand the concept better.

Example #1

The switch from USD London Interbank Offered Rate or LIBOR to replacement rates is going smoothly, and per Fitch Ratings, there is a lot of time until the deadline (June 30, 2023) to fix the transition problems. That said, the Federal Family Education Loan Program or FFELP student loan asset-backed securities remain susceptible to the basis risk of the draft rules under the LIBOR Act.

The Federal Reserve Board wanted feedback concerning the draft rules this year. However, it did not signal the requirement of conforming changes for applying a replacement rate. The preliminary rules propose multiple Secured Overnight Financing Rates or SOFR settings with suitable tenure-spread adjustments for multiple instruments. For instance, the SOFR is compounded in arrears for derivatives. That said, for cash products and consumer loans, it is the term SOFR. The different settings between bonds and derivatives might lead to a basis risk for bonds that rely on cash flows under derivatives contracts.

Example #2

Suppose a portfolio manager named Ryan wants to eliminate a diversified stock portfolio’s risk exposure. Hence, he decides to short Dow Jones futures.

If the portfolio’s composition does not match Dow Jones’s, the hedge will be imperfect. As a result, Ryan will have to take on basis risk.

Frequently Asked Questions (FAQs)

What causes basis risk?

Basis risk in derivatives arises when a predictable relationship does not exist between the price of a futures contract and the price of the hedged financial asset.

Is basis risk a credit risk?

No, it is not a credit risk. Credit risk is a possibility of a loss that arises from the borrower’s inability to fulfill contractual obligations or repay a loan. Unlike basis risk, it is an example of unsystematic risk.

How to manage basis risk?

Portfolio managers and traders must properly analyze market trends to manage this risk. For instance, the discount on the local market is generally larger than the futures market during harvest time. Afterward, the basis narrows.

What is basis risk in energy?

It is the possibility that the hub price exceeds the nodal price where the sale of power takes place. In other words, the risk arises when the cost of purchasing electricity to resell to the hedge provider is more than what was paid to the project for the electricity sold into the grid.

Recommended Articles

This has been a guide to What Is Basis Risk and its meaning. Here, we explain the types of basis risk and their examples. You may also find some useful articles here –