Part of our Risk Management guide

What Is Wrong Way Risk?

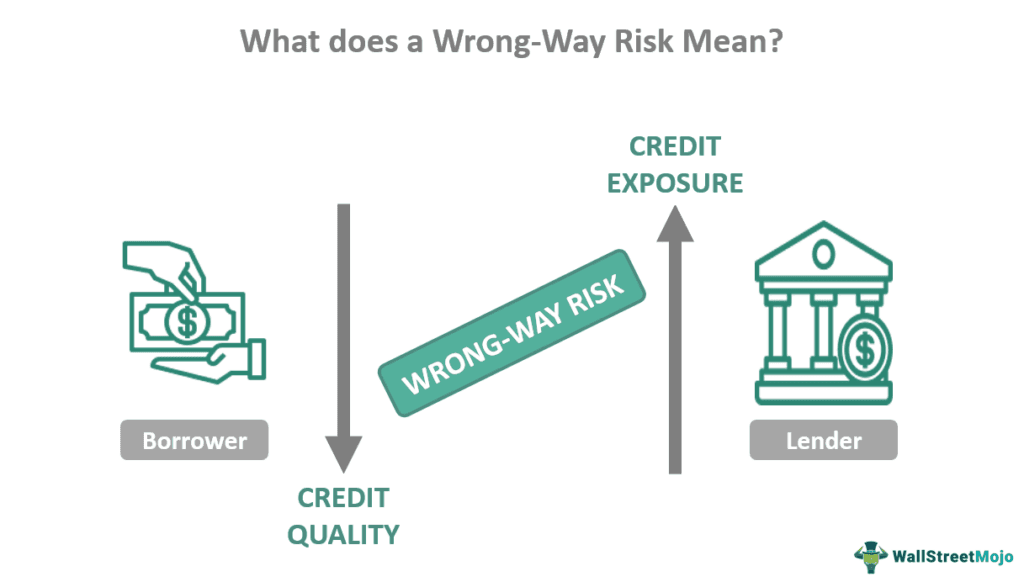

Wrong-way risk (WWR) in finance refers to the scenario where credit exposure increases with the credit risk involved. Credit exposure has a negative correlation with credit rating or quality. Therefore, the more a lender gains on lending, the more chances of the borrower defaulting.

Counterparty credit risk usually constitutes wrong-way and right-way risk (RWR). The latter is the exact opposite of the former. These concepts are important in assessing financial markets and even in banking. Analyzing the risk is a significant step toward managing it. Thus, it is a concern for regulators and banks.

- Wrong-way risk can be defined as inverse proportionality between credit exposure and credit quality. Thus, if the credit quality of a debtor falls, the creditor is more likely to face higher exposure and risk.

- There are two types of WWR – general and specific wrong-way risk. General WWR occurs due to macroeconomic factors affecting a particular market, industry, or economy. Specific WWR, on the other hand, affects a particular company alone.

- The opposite of WWR is the right-way risk (RWR) which implies that credit exposure decreases with the decline in credit quality.

Wrong Way Risk Explained

Wrong-way risk is a slightly complicated concept. Let’s try and simplify it. Counterparty credit risk means the risk of a debtor defaulting before the final settlement is made to the creditor. There are two ways this can happen – right and wrong.

Right-way risk implies credit exposure decreases as the debtor’s credit quality declines. This reduces the counterparty credit risk. In wrong-way risk, the opposite happens, i.e., credit exposure increases as credit quality decreases. Therefore, the right-way risk is generally preferred over the wrong way, as the latter is more dangerous and can result in extremely high losses for the creditor. Let’s plot these conditions on a graph of the probability of default against exposure.

These are the possible correlations between the probability of default and credit exposure. Independent means that there is no correlation at all. There is a positive correlation in wrong-way risk, i.e., exposure increases as the probability of default increases. Conversely, right-way risk has a negative correlation, implying that exposure falls as the probability of default increases.

Types

There are two major types of WWR – specific and general.

- Specific wrong-way risk (SWWR) – This type of risk is caused due to factors specific to a company or its asset – like a fall in rating or litigation. It can also arise due to poorly structured transactions. One can and should avoid SWWR to a great extent. Example: Company X is involved in producing gold. It sells a put option on its stock. If the stock price falls, the company’s credit rating/ quality falls too. Simultaneously, the company’s liability towards the owner of the option increases (exposure increases).

- General wrong-way risk (GWWR) – Such a type of risk can occur due to economic, financial, and other factors that affect the overall market, economy, or nation. Example: Companies A and B enter an interest rate swap agreement where A lends at a fixed interest rate to B, hoping to benefit from a floating interest rate in the future. If the interest rates rise globally, B would be disadvantaged as its credit position worsens, and its payment liability to A will also increase.

Examples

Here are some examples of the concept of wrong-way risk.

Example #1

Bank M is in the United Kingdom, while bank Z is in South Korea. Z is a borrower and borrows GBP 1,000,000 from M for financing and other lending purposes. Z agrees to pay back M within a year at 10% interest in GBP. However, after a year, due to macroeconomic factors, if Korean Won depreciates drastically against GBP, bank Z has to pay back more in its local currency than it would have had to pay earlier. This is highly disadvantageous to Z, which has to pay more. Further, the exposure of bank M has increased now.

Example #2

Here are some wrong-way risks the international monetary fund (IMF) forecasts in its global financial stability report.

- Currency swaps in U.S. dollars – The depreciation of the second currency is likely to increase credit risk and exposure.

- Corporate credit default risk – Companies’ credit quality falls, increasing creditors’ exposure.

- China property sector downturn – Dual shock from property developer defaults and boycott of mortgage payments by homebuyers.

- Loan market credit crunch – Rating downgrades and lower returns on investments in collateralized loan obligations (CLO) could lead to a decline in its issue and a credit crunch in the loan market.

Wrong Way Risk And CVA

First, let’s understand CVA, or credit valuation adjustment. CVA is a hedging strategy that aims to limit risk from financial investments. Under CVA, a portion of the profits is set aside to cover the financial assets without collateral. One can consider it as a reserve.

So, how is CVA affected by a wrong-way risk? In a WWR, the CVA component amplifies, meaning more reserve needs to be set aside. And surprisingly, this is one of the methods to quantify WWR. So, let’s understand how to determine it through wrong-way risk modeling.

- Firstly, the life of outstanding derivatives is divided into intervals.

N is the number of intervals

qi = risk of credit default in the ith interval

vi = present value of expected exposure in the midpoint of the ith interval

R is the expected recovery rate

- Here, if qi increases with vi, the two have a positive correlation. Hence, wrong-way risk.

Further, the correlation between the probability of default and the level of interest rate has a significant impact on the CVA.

Frequently Asked Questions (FAQs)

How to mitigate wrong-way risk?

One of the popular ways to mitigate WWR is the application of additional haircuts in collateralized transactions. However, another easier way is to increase collateral which will help decrease credit exposure naturally. And since general wrong-way risks are beyond a borrower’s control, the borrower can try and avoid specific WWR.

How do you identify wrong-way risk?

Stress and scenario testing are commonly employed to identify wrong ways and risks in general. However, wrong-way risk modeling can help quantify WWR. For this, credit valuation adjustment (CVA) must be determined first. WWR usually leads to an increase in CVA, and its degree can be used to understand the effect of WWR.

What is a wrong-way risk example?

Suppose a creditor purchases a put option on the stock from a company. If the stock price falls, the company’s credit quality should fall, thus increasing its financial liability to the creditor, thereby exposing the latter to a higher degree. This is an example of a specific WWR.

Recommended Articles

This has been a guide to what is Wrong Way Risk. Here, we explain its examples, relation with credit valuation adjustment, and types. You can learn more about accounting from the following articles –