What Is Dividend Declared?

A dividend declared is that portion of profits earned by the company’s board of directors that decides to pay off as dividends to the shareholders of such a company in return for the investment done by the shareholders through the purchase of the company’s securities.

Such declaration of dividend creates a liability in the books of the concerned company. The company must not declare dividends more than the profits available from current and previous financial years of the company’s performance as it will create liquidity issues.

- A dividend declared is the fraction of earnings that the board of directors of a company decides to distribute as dividends to its shareholders in exchange for their investment in the form of stock purchases. Such a dividend declaration results in a liability on the records of the involved corporation.

- A “dividend declared” is when the Board of Directors announces dividend distribution. It reduces earnings and creates a “dividends payable” liability.

- The company may distribute dividends after emergency funds are met, boosting market confidence without losing money.

Dividend Declared Explained

Dividend declared is when the company makes the declaration regarding the payment of part of its earnings as a dividend to its shareholders. The amount of dividend to be declared is decided in a general meeting where the board of directors agree to the proportion and shareholders give their consent.

Such declaration leads to creating a liability account in the company’s balance sheet for the associated payments until the dividend payment is made. The value of such a liability account depends on the amount declared by the board of directors authorized by shareholders.

In the case of a company, dividend distribution tax is paid by the company when the dividend is paid to the shareholders and not when it is declared. The announced dividend and the dividend distribution tax are deducted from retained earnings at the time of declaration. And a similar amount is credited to the dividend payable liability account. But actual tax payment is made when the dividends hit the shareholder’s account.

Suppose a company declares a dividend on October 10, 2018, for dividends with future payment dates as March 25, 2019. However, there was a new policy rolled out by the government in the company’s sector of operation, which led to a reduction in liquidity in the company for the medium term. Thus, the company requires cash for regular business operations. Hence, if a company wants such dividends to be reversed, the same can be done. The company will need to call for another meeting of the board of directors, and basis their vote, the dividends can be reversed.

How To Calculate?

Though there is no such standard formula for calculating the dividend declared, the calculation below shows how the dividend is computed.

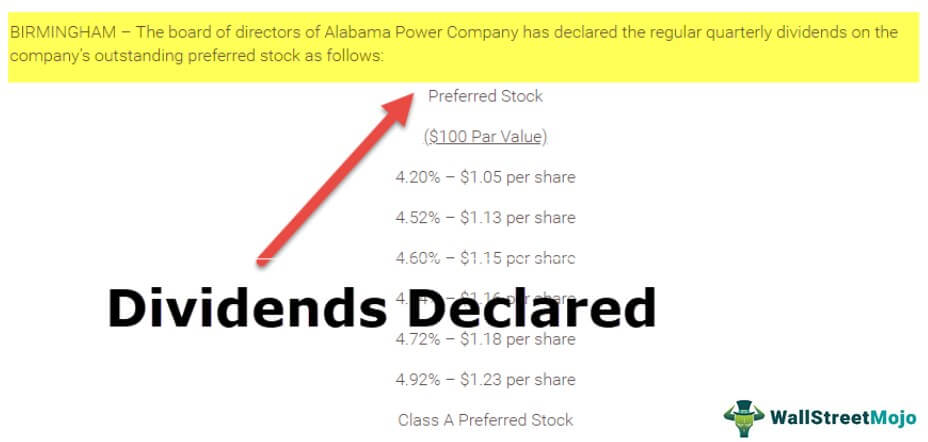

On December 20, 2018, a company, XYZ Limited’s board of directors, announced that a cash dividend amounting to $ 4.5 per share would be paid to the shareholders of the company. The actual payment of cash dividends to the investors will be made on April 04, 2019. The total number of shares of the company is 2,50,000 shares.

Thus, a journal entry for Dividend Declared on December 20, 2018,looks like:

- Retained Earnings to be Debited by Dividend * Number of shares = $ 4.5 * 2500 = $ 11,25,000/-

- Dividend Payable accounts on the current liability side to be credited by $ 4.5 * 2500 = $ 11,25,000/-

Now, as was declared earlier, dividends will hit the investor’s account on April 04, 2019; the following journal entries will be passed into the company’s account:

- Dividend Payable accounts on the current liability side to be debited by $ 4.5 * 2500 = $ 11,25,000/-

- Cash account on current asset side to be credited by $ 4.5 * 2500 = $ 11,25,000/-

Benefits

Dividend Declared helps to develop a positive sentiment in the market for the company. For example, if a company wants to create a positive sentiment in the market, thereby increasing the price of its shares. But it does not want to part with the cash in the company in the short term to create hedging for some contingency. The company may declare a dividend to be paid once the company’s short-term contingency fund requirement is over. This way, the money will not flow out of the company’s books, and positive sentiment will also be created in the market.

Dividend Declared Vs Dividend Paid

To understand the dividend declared meaning properly, investors and entities must be aware of the differences it shares with the dividend paid. Here is a list of few differences between the two:

- When the board of directors issues a declaration regarding dividend distribution, it is a dividend declared. The accounting effect of the dividend is retained, the earnings balance of the company is reduced, and a temporary liability account of the same amount is created called “dividends payable.”

- The dividend paid is the event when the dividends hit the investor’s account. When the dividends are paid, the “dividends payable” liability account is removed from the company’s balance sheet, and the company’s cash account is debited for a similar amount.

Frequently Asked Questions (FAQs)

How to record dividends declared?

You must make a journal entry that debits retained profits and credits dividends payable to record a dividend declaration. This entry is created when the company’s Board of Directors declares the dividend.

Can the dividend declared be revoked?

A dividend that a firm has already announced can only be changed with the shareholders’ approval. As a dividend is issued, it becomes a “Debt” in the shareholders’ favor. It implies that a declared dividend becomes a debt owed by Company shareholders.

Is dividend declared an expense?

Dividends are not classified as an expense since they represent a company’s earnings distribution. Hence, dividends do not appear as an expense on the income statement of the issuing entity. Instead, they are regarded as a distribution of the business’ equity.

What is the “dividend declaration date?

The dividend declaration date is when a company’s board of directors officially approves and announces the dividend payment. It is the starting point for determining which shareholders are entitled to receive the dividend.

Recommended Articles

This article has been a guide to what is Dividend Declared. Here we explain how to calculate, vs dividend paid along with the benefits and examples. You can learn more about financing from the following articles –