Part of our Balance Sheet guide

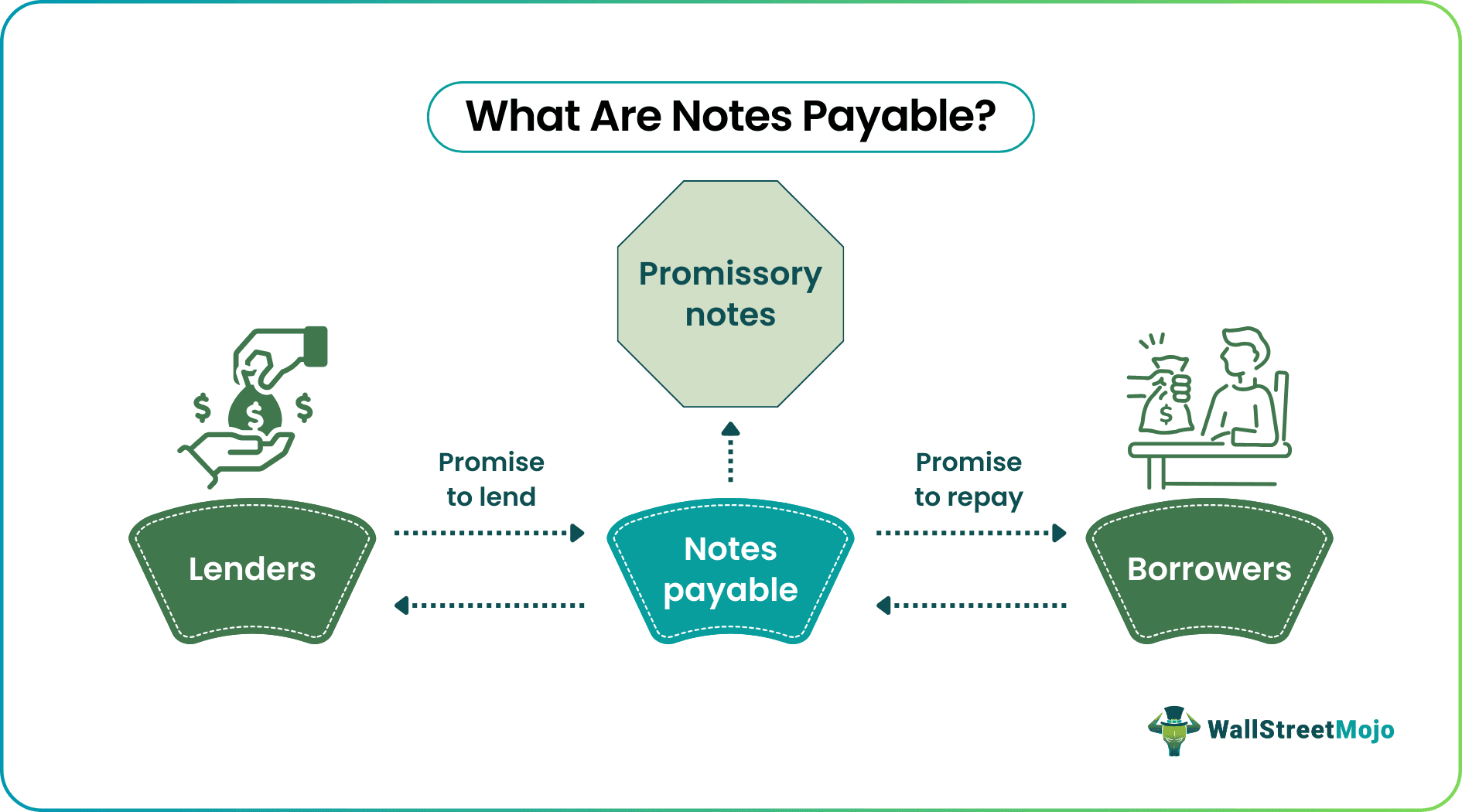

What Are Notes Payable?

Notes Payable are a promise in writing whereby a borrower assures repaying the lenders within a specific period. These promissory notes indicate the loan that one party lends to the other, expecting the timely repayment, which may be the principal alone or the principal along with the interest amount.

The notes payable is legally binding and signed by both parties, which need to stick to the points mentioned. It differs from Accounts Payable, which is used when firms purchase goods and services from the other party on credit and expect to pay for them later.

- Notes payable is a promissory note offered by the lender to the borrower wherein the latter is bound to pay a certain amount to the lender within a stipulated period along with interest.

- These can be short-term agreements with due dates within a year or long-term with validity beyond a year.

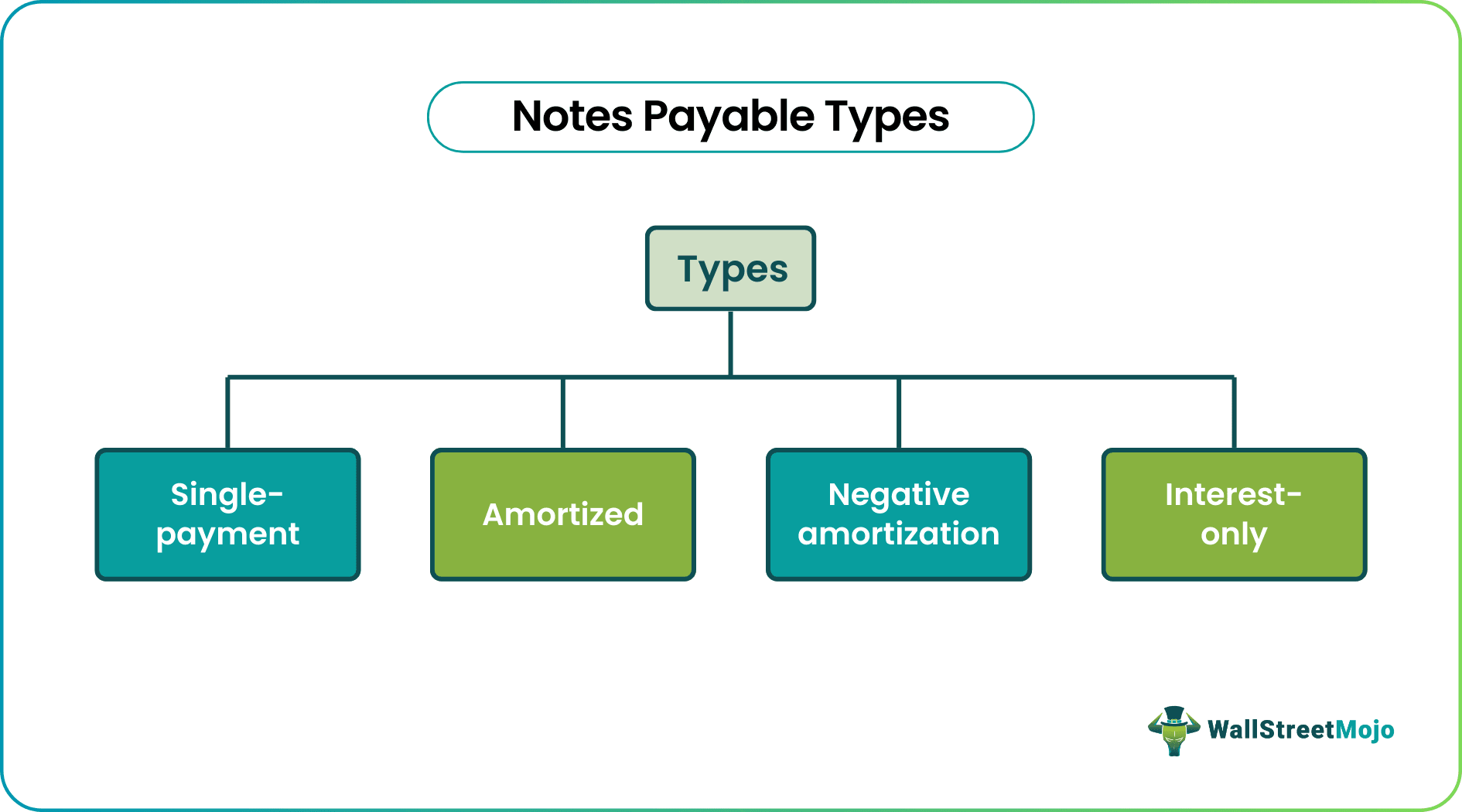

- Single-payment, amortized, negative amortization, and interest-only are the types of such contracts.

- The same agreement becomes notes receivable if recorded on the balance sheet at the end of the lender.

Notes Payable Explained

Notes Payable resembles any loan, which binds borrowers and lenders against payment and repayment liabilities. As soon as the agreement is signed, the borrowers receive the amount in cash from lenders with a promise to pay back the amount, which could either be the principal amount alone or the principal along with the applicable interest amount.

When borrowers make the contract’s journal entry as liability, it is termed as notes payable. On the other hand, when the same is recorded as an asset by lenders, it is known as notes receivable.

These agreements detail all important points surrounding the transaction. It comprises information related to the amount paid, applicable interest rate, name of the payer and payee, the maturity date, limitations if any, and the issuer’s signature with the date. In addition, the timeframe can differ hugely and range from a few months to five years or maybe more. In short, these promissory notes can be short-term with a validity of up to a year or long-term, involving a timeframe of more than a year, given the period of payment and repayment involved.

The contracts must be registered with the Securities and Exchange Commission (SEC), being identified as a security sometimes. Notes payable on the balance sheet take a spot under the liabilities column. They are considered current liabilities when the amount is due within one year, and else they are recorded under the long-term liabilities category.

Types

These contracts are obligations for the parties involved and are classified as – single-payment, amortized, negative amortization, and interest-only types. Therefore, exploring them is important to better understand the meaning of notes payable.

Single-Payment, as the name suggests, is a contract in which the borrowers require repaying the principal and interest amount as one lump-sum payment by the end of the maturity period as specified in the agreement.

Amortized, on the other hand, is whereby a borrower pays a fixed monthly amount, including both principal and interest portions. Here, the major portion is paid towards the principal and the rest towards applicable interest. Amortized agreements are widely used for property dealings, be it a home or a car.

Negative agreements require borrowers to pay interest less than the applicable interest charges, thereby adding the remaining amount to the principal balance. Though choosing this option helps people refrain from paying more as interest when inconvenient, the same adds up to the total amount to be repaid in the long run, increasing the burden.

The interest-only type requires borrowers to pay only the applicable interest every month with an assurance of the repayment of the entire principal amount at the end of the loan tenure.

Notes Payable Explained in Video

Examples

Let us consider the following notes payable examples to check how it works:

Example #1

Kelly shortlists a residential property and decides to go ahead with it. She contacts a lending institution, and they agree to pay the required amount. The latter prepares the notes payable with all the details to sign and get it signed by themselves and Kelly, respectively. Kelly reads the documents and finds that she must pay a fixed monthly amount to the lender. The amount mentioned seemed convenient for her to pay. She signed the agreement and received the amount instantly to book the property.

Example #2

Suppose Company Bev has a long-term note payable obligation of $1000. Let us check the journal entry for notes payable at the end of the payee, preparing the sheet. Here, it is created at the end of customers as they are the ones who borrowed the amount:

Scenario 1

The cash is a debit entry as it is an asset in the above scenario. As the customers receive the cash, there is an increase in their assets, and hence they debit the account. At the same time, notes payment is a credit entry as they promise repayment, which is a liability.

| Account Titles | Debit (Dr) | Credit (Cr) |

|---|---|---|

| Cash Account | 1000 | – |

| To Notes Payable Account | – | 1000 |

Scenario 2

The next entry in the balance sheet is of interest, an expense for the customers yet to pay. Then, finally, the entry is made with respect to the applicable interest:

| Account Titles | Debit (Dr) | Credit (Cr) |

|---|---|---|

| Interest Expense Account | 150 | – |

| To Interest Payable Account | – | 50 |

| To Cash Account | – | 100 |

In this journal entry, interest expenses is a debit entry, and interest payable is a credit entry, as a portion of it is yet to be paid. Thus, it is also a liability to take the credit side. The cash account is a credit entry as the amount will decrease, given the pending interest payment.

Scenario 3

The customers make the final journal entry when they repay in full. Here, notes payable is a debit entry as it leaves no further liability. The same applies to the interest payable. The cash account, however, has a credit entry, given the cash outflow in making repayments, which records a decreased asset.

| Account Titles | Debit (Dr) | Credit (Cr) |

|---|---|---|

| Notes Payable Account | 1000 | – |

| Interest Payable Account | 50 | – |

| To Cash Account | – | 1050 |

Notes Payable vs Bonds Payable

→ Explore all 63 Bonds articles

Notes and bonds payable are terms that sound confusing and synonymous, but they differ in many aspects. Let us look at some of the differences and similarities between them:

| Category | Notes Payable | Bonds Payable |

|---|---|---|

| Treatment | Not necessarily treated as a security | Treated as a security |

| Lenders involved | Signifies the amount owed to one lender | Involves multiple lenders issuing the number of bonds simultaneously |

| Form | Form of debt | Form of debt |

| Recorded as | Liabilities | Liabilities |

Frequently Asked Questions (FAQs)

Are notes payable a debit or credit?

These are debit entries with the cash accounts being credited, considering the amount received as debt from lenders, which indicate the borrowers’ liabilities.

Are notes payables current liabilities?

These agreements can be short-term contracts with a due date falling within a year or long-term with a maturity period beyond one year. If the liability is for more than a year, it becomes a long-term liability. On the other hand, short-term agreements are treated as current liabilities.

How to record notes payable?

When one takes up the loan and signs the agreement, it becomes the debit entry on the part of the one who borrows the amount. The cash account of the borrower goes to the credit side. As soon as the loan is repaid, the note payable account of the borrower is still on the debit side and cash on the credit side. This is because the debit side indicates no further liability for the borrower with the cash account being credited.

Recommended Articles

This has been a guide to what are Notes Payables. We explain their types, examples, journal entry on the balance sheet, and differences with bonds payable. You may also have a look at these articles below to learn more about accounting –