Table Of Contents

What Is A Capital Lease?

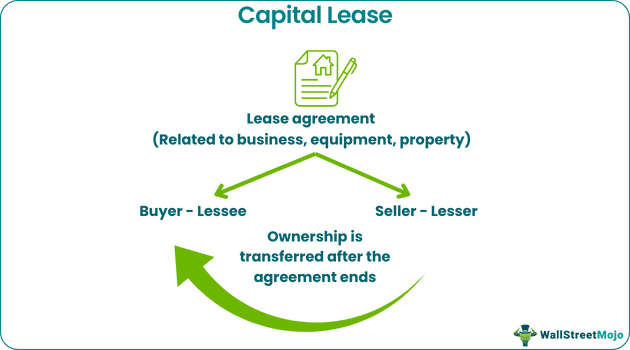

A capital lease is a legal lease agreement of any business equipment or property that is equivalent or similar to a sale of an asset by one party called the lesser to the buyer, who is called the lessee. The lesser agrees to transfer the ownership rights to the lessee once the lease period is completed.

The contract is generally non-cancellable and long-term in nature. The asset is treated in the books just like the lessee is the actual owner and is shown in the balance sheet. There are two types of leasing process- Capital lease and Operating Lease. Depending on the requirements of the business and its tax situation, a company may pick any of the lease types or even a combination of both.

Table of contents

Capital Lease Explained

In a capital lease, there is an agreement between the asset owner, who is the lesser and another party, who is the lessee. However, after the end of the contract the lessee gets ownership of the asset.

It is a long-term and non-reversible / non-cancellable type of lease. When a company or business has fewer funds to purchase an asset, it chooses to either borrow or lease the asset. The fundamental difference between these two options is the ownership is transferred at the beginning of the lending or borrowing period. In contrast, in the case of leasing, the ownership is passed only on completion of the lease period. Therefore, this type of lease can be considered debt and incur interest expense for the lessee.

The lesser books the assets and the liabilities when certain specific criterias are met in case of capital lease obligations. It is very close to an actual purchase because under the Generally Accepted Acccounting Principles (GAAP), it is viewed as an actual buy and is accounted for accordingly. Therefore, it impacts the financial statements and reports, affecting various accounts like depreciation, assets, liabilities, interest, etc.

As per the Financial Accounting Standards Board (FASB), a change was made in the method of accounting, any lease contact whcihis more than a year has to be accounted for in the financial statements and treated as a capital lease obligations.

Thus, it is a contact that allows the lessee to buy the asset at the end but at a lower price compared to the current market value. It has an effect in the financial statement and has some tax implications too. The process can be complex, depending on the nature of the asset and the terms of contract.

Capital Lease vs Operating Lease - Explained in Video

Requirements

Let us study the requirements of the capital lease criteria, per the different accounting principles, at least one of which must be fulfilled in order to become a capital lease agreement. .

- There will be a transfer of the ownership of the asset from the lesser to the lessee at the end of the contact period.

- The above will be done at a price which is lower than the market value of the asset. The agreement should contain this provision.

- The next requirement is that the term of the lease should be such that it should cover at least 75% of the total economic life of the asset.

Thus, if the arrangement meets any f the above criterias, then the condition is fulfilled. The accounting process and corresponding tax treatment will be as per the methods mentioned in the details below. This is how it becomes different from the operating lease.

Accounting Treatment

In order to study the accounting treatment of this lease agreement, it is necessary to understand that it is like an accrual accounting process for an economic transaction, where the present value of a financial obligation is recorded. The process is treated as a financial arrangement.

The company, which is the lessee, needs to break the lease payments into interest and depreciation expense while recording capital lease journal entries. Thus, whatever fund is received in the form of lease amount, the total amount is entered in the books as credit value in cash account, the interest part is debited in interest expense account and the rest amount is debited as the capital lease liability.

There is also depreciation involved in capital lease journal entries. The method is chosen as per the company policies, the depreciation expense account is debited and accumulated depreciation is credited. During the time of sale or disposal, the remaining depreciation is amount is debited form the accumulated depreciation value and fixed asset account is credited due to sale.

Examples

Examples of the assets, including Aircraft, lands, buildings, heavy machinery, ships, diesel engines, etc., are available for purchase under capital lease. Smaller assets are also available to be financed and are considered under another type of lease called the operating lease.

Tax Treatment

The tax treatment depends on the laws of the jurisdiction where the agreement is made. However, the lessee will charge depreciation in their books for the leased asset and claim deduction based on depreciation amount as per the tax laws. Not only depreciation, this method is applicable for interest amount also in order to claim deduction, subject to certain limits.

Under the arrangement, the interest portion of the payment is tax deductible but not the principal, since the liability is reduced because of it. All the above impacts the taxable income of the company. The jurisdiction may have some benefits like tax credits or incentives which the lessee may be eligible for and which can affect the tax treatment.

It is a good idea to consult tax professionals for this purpose of capital lease on the balance sheet, which may be complex and may change over time.

Advantages

- Depreciation Claim: the lessee of the asset can show the same asset in its balance sheet and claim depreciation. This setup reduces the taxable income of the lessee company

- Ownership: the lessee can use the asset for more than 75% of its life. The lessee also has an option to purchase the asset after the termination of the lease period and at a rate lower than the current market rate of the asset.

- Interest Expense: the lesser needs to pay the interest that the owner of the asset charges. Since it is an expense for the company, it shows the interest expense as an expense in the income statement, reducing the business's taxable income.

- Off-Balance sheet debt: Capital leases are counted as debt

- No risk of obsolescence: any company can act as a lesser and reduce its risks and lower productivity due to the risk of obsolescence of any fixed assets.

Disadvantages

- Debt to Equity Ratio: In the case of a capital lease, there is a creation of debt by the lessor in its balance sheet. These lease payments are paid off periodically. This increased debt directly impacts the debt to equity ratio in a severe manner, due to which maintain the interest of all the stakeholders becomes difficult.

- Maintenance Charges: once both the parties involved enter into the agreement, the lessee is expected to maintain and make any repairs, as required. It adds to the existing costs for the company.

- Risk of holding Obsolete Assets: At times, the lessor makes a good move in leasing out an obsolete part or the entire asset

Capital Lease Vs Operating Lease

There are some differences between these two types of lease agreements as given below:

- The former involves transfer of ownership at the end of the lease period but there is no such arrangement in case of the latter.

- In case of the capital lease on the balance sheet, the lessee has to record the asset and liability in the balance sheet whereas the latter is treated as a rental expense and recorded in the income statement, but not in the balance sheet.

- The lessee, in case of the former will have all the rewards, like the asset value appreciation or bear the risk like depreciation cost and maintenance cost. But in case of the latter, the above is borne by the lesser, since there is no transfer of ownership.

- The former is for longer term and the latter is for shorter term.

Thus, the above are some important differences between the two types of lease agreements.

Recommended Articles

This article has been a guide to what is a Capital Lease. We explain its differences with operating lease, accounting treatment along with examples & requirements. You can learn more about accounting from the following articles –