What Is The Equipment Lease?

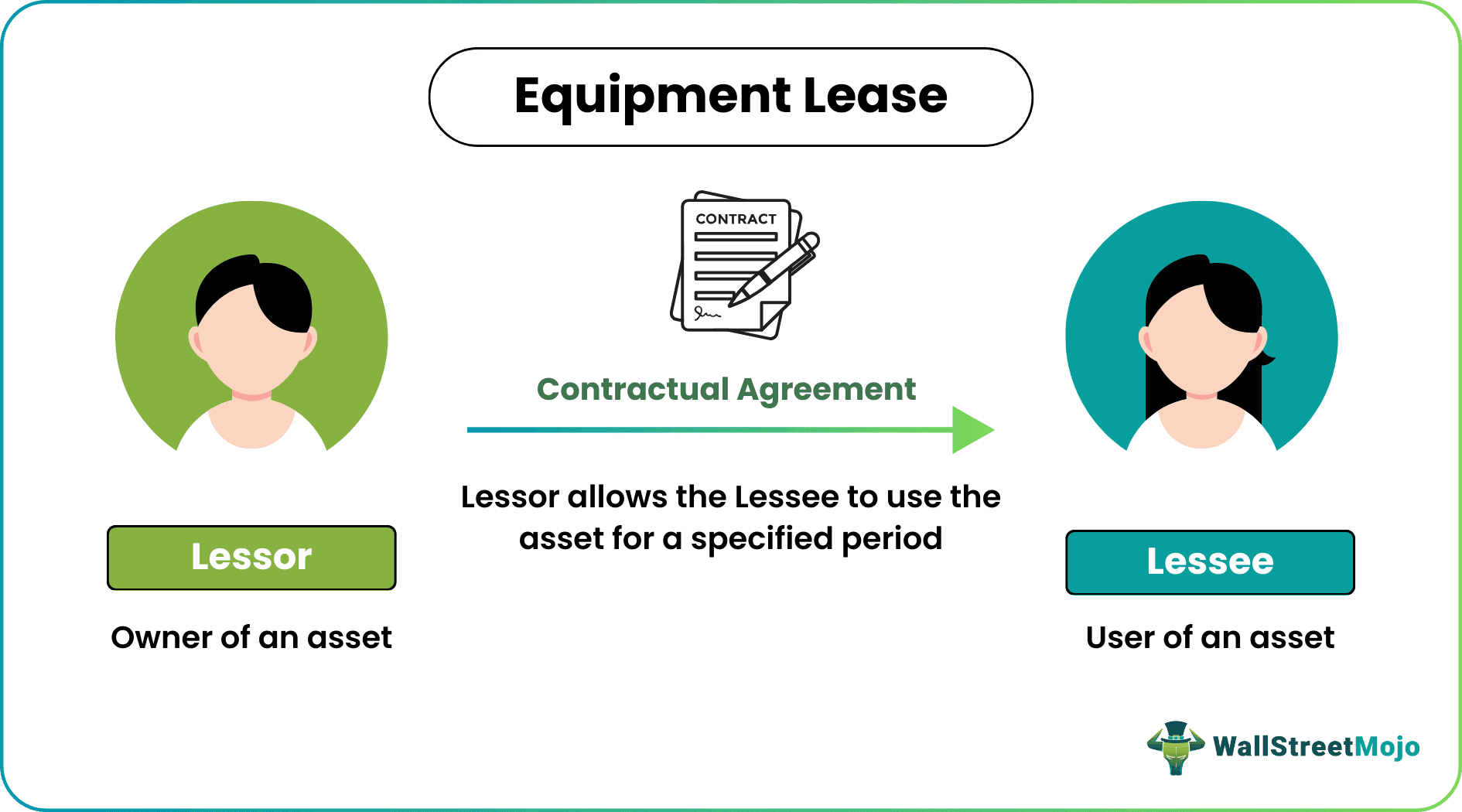

Equipment Lease refers to the lease where one party who is the owner of the equipment allows another party to use the equipment in exchange for the periodic rentals where the ownership during the tenure of the agreement remains with the lessor only and has the right to cancel the lease right away when he finds that the lessee has contravened any terms of the lease agreement.

In simple words, it is a contractual agreement between two parties, namely the Lessor ( owner of the asset) and Lessee (user of the asset), wherein the Lessor allows the Lessee to use the asset for a specified period in return for periodic payments popularly known as Lease payments.

The equipment lease agreement is a popular model that is frequently used by The The equipment lease agreement is a popular model that companies across the globe frequently use. However, this Lease has its benefits and disadvantages, which we will try to understand through this article. Instead of buying the assets, companies prefer to lease them, thereby saving millions of dollars in the purchase. However, this Lease has its benefits and disadvantages which we will try to understand through this article.

Types of Equipment Leases

This Lease is mostly divided into two types which are as follows:

Type #1 – Finance Lease

Finance Lease is known as Capital Lease in the United States and is the purchase of Equipment by the business, financed by raising Debt. Effectively in a Finance Lease, the balance sheet gets equally impacted by adding an equal amount to both Assets and Liabilities of the Balance Sheet of the Company.

Over the term of the Finance Lease, the Lessee will recognize depreciation expense on the equipment and interest expenses on the debt liability. Interest Expense is equal to the lease liability at the beginning of the period multiplied by the Lease Interest Rate.

Type #2 – Operating Lease

Operating Lease is a rental agreement between the Lessor and Lessee where no equipment purchase occurs. The lessee pays periodic lease payments, which are recognized as rental expenses in the Income Statement.

In the Cash flow Statement, the lease payment for this lease is reported as an outflow from Operating Activities. Since Operating Lease doesn’t impact the Balance Sheet of the Lessee, Operating Lease is also referred to as Off-Balance Sheet Financing Assets.

Calculation Example of Equipment Lease Payments

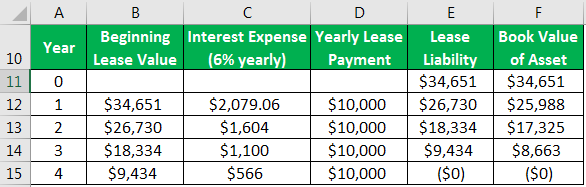

Click International leases a Machine from Harry International for its internal use purpose. The Details are furnished below:

- Monthly Lease Payment: $10,000

- Useful Life (in Years): 4

- lease Rate: 6%

At the end of the four years, the machine will be returned to Harry International, who will sell the machine for its Scrap Value.

Based on the above facts, let’s try to calculate the Lease payments and other depreciation details:

Click International will classify the Lease as a Finance Lease instead of an Operating Lease because the asset is being leased for 75% or more of its useful life. Also, it is mentioned clearly that at the end of the lease, the asset will be disposed of for its scrap value.

Thus at the beginning of the Lease, the Present Value of the Lease, i.e., $34651, will be recorded under the Asset side and liability side of the Balance Sheet of Click International.

Therefore, the Schedule of Lease Payments will be:

Refer to the Excel Template for detailed calculation.

Lease vs Rent – Explained in Video

Advantages

- It is a less costly source of financing as it requires no initial down payments, which result in conserving cash for the user of the asset, i.e., Lessee.

- Operating Lease allows the Lessee to return the asset at the end of the lease, reducing the risk arising out of Obsolescence of Equipment on account of technological changes, etc.

- Another advantage that usually arises in the case of the Operating Lease type of Equipment Lease is that it doesn’t result in a Balance Sheet Liability as it is an Off-Balance Sheet Financing. Hence Leverage ratios such as Debt/Equity ratio etc. are lower compared to the outright purchase of Assets.

- Certain Tax advantages are accorded to firms operating in the United States whereby such lease is treated as an Ownership position just like the purchase of Assets, and the business can deduct Depreciation and Interest expense for tax purposes. It can consider a lease as a rental agreement for financial reporting purpose.

Disadvantages

- Equipment lease agreement, when considered as a Finance Lease, results in Leverage Ratios such as Debt to Assets Ratio, Debt to Equity Ratio to be higher on account of reporting of Liability on the Balance Sheet.

- Operating Income is reduced when a Lease is considered as an Operating Lease as the whole lease payment is considered as a Rental Outflow and debited from the Income Statement.

- Usually, in Equipment Lease, particularly in Operating Lease, the tenure and the amount of Lease Payment are fixed at the beginning of the Lease itself, irrespective of whether the Equipment becomes obsolete due to the technological changes, etc., which can result in a committed cost for the Lessee without resulting in any benefit.

- An Operating Lease results in fixed cash flow payment in the form of Lease Rentals and can be burdensome for business when sales are impacted due to adverse business conditions.

Essential Points About Change in Equipment Lease

Under the Equipment lease agreement, the classification of Lease (Operating or Financing Lease) is determined by the economic substance of the lease transaction, which means that if the lease agreement results in the transfer of all rights and risks related to ownership to the Lessee, then such lease will be characterized as Finance Lease and will be shown on the Balance Sheet of Lessee as discussed above. These criteria apply both under US GAAP and IFRS.

Conclusion

Equipment Leasehold’s important implication on the business and its choice has widespread consequences. The business should decide on the type of lease after considering its business model, Asset life, and the changes in the sector in which such asset is put to use to make the most out of this lease.

Recommended Articles

This article has been a guide to Equipment Lease and its meaning. Here we discuss the types of Equipment Lease, its examples, and calculations along with advantages and disadvantages. You can learn more about accounting from the following articles –