Part of our Balance Sheet guide

Off-Balance Sheet Meaning

Off-balance sheet items are those assets that are not directly owned by the business and therefore do not appear in the basic format of the balance sheet. However, they tend to impact the financials of the company indirectly. An operating lease is a glaring example where the asset value is not recorded in the balance sheet, but in case of any misuse, the entire amount of the asset would be borne by the company.

Earlier, the companies with hidden assets and liabilities tend to show a different picture to the investors, potential investors, and third parties. Thus the actual picture was not visible. After the introduction of the disclosure of hidden assets and liabilities within the Balance sheet, the related party, along with the investors, would tend to notice the real picture of the company. The rule emphasizes the theory that the operating assets which earn revenue for the company should be disclosed properly and effectively so that the leverage position can be evaluated properly.

Off-Balance Sheet Explained

The term off-balance sheet explains all the assets and the liabilities that are not displayed in the balance sheet of a company. But that does not mean that they are not relevant to the business operations. They still remain important components of the business but are just not directly fall under company obligations of ownership.

Therefore, off balance sheet items indirectly impact the financial satements and reporting procedures, even though they are not openly visible on the statements. They have an effect on the risk-taking capacity, the current payment obligations, the cash flow, financial health, future planning and expansion and overall development of the company.

Among common items that fall under this catagory, there are operating lease, that many companies very often do not report in the balance sheet, certain contingent liabilities or joint ventures are often not mentioned because they may often affect the company image and its profits. Sometimes a business may also not mention the accounts receivable balances in the balance sheet because they are may or may not be received at all and there is often a probability of default. This helps in maintaining the company image and credibility but are recorded in the balance sheet when they are received.

But it is to be noted that these off balance sheet items provide options for financing or flexibility, it also creates an image about the company which may not be true. In other words, the true asset and liability position is concealed. This proves to be tricky for investors and analysts who frequently refer to the balance sheet to assess the financial health of a business.

OFF Balance Sheet Explained in Video

Types

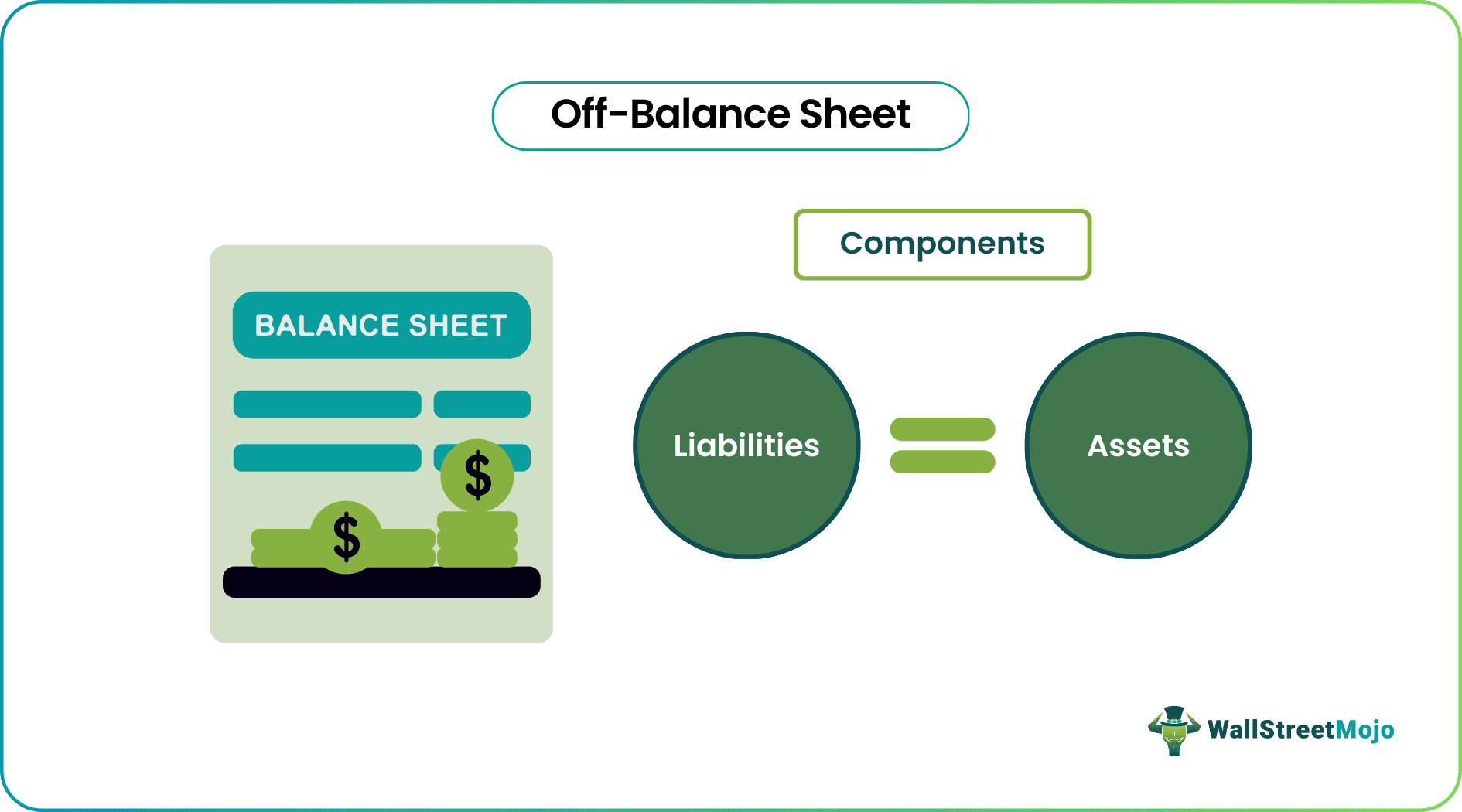

We know that the basic balance sheet consists of three segments: assets, liabilities, and Owner equity or Equity capital plus reserves. Off-balance consists of two components as Assets and liabilities. Some items are associated with the business and do not appear directly on the balance sheet; they are invisible. E.g., leverage in the form of debt (liability items), operating lease (assets), etc. In some cases, any banks/ financial institutions offer an array of financial activities such as brokerage services and asset management to their esteemed clients, which might not be their original business.

Examples

Let us understand the concept of off balance sheet exposure with the help of some suitable examples.

Example #1

XYZ Ltd. has a D/E rate of 3.5. Because of high leverage, the company cannot do a capital expenditure worth $5 million, which would increase D/E to 4.5. Thus, it might hinder shareholders’ confidence. So the management of the company might opt for an operating lease option, where the company would only pay Machinery rent per the machine owner’s quotation. Thus the leverage position is not compromised. However, the shareholders should also be informed about the company’s current scenario, such as the additional revenue not coming from the company’s fixed assets. In case of any damage caused to the machinery, the entire liability would be borne by the Company. Thus, the additional risk should be ascertained as the company’s liability in case of any damages.

Example #2

ABC Bank Ltd offers its clients a savings account and other banking transactions. A high Net worth individual may ask for a service not offered by the bank itself. However, they can’t refuse as the above client has a long relationship with the bank. Suppose the client requires brokerage services. The bank has contacts with brokerage firms and would provide the service via that particular brokerage firm. Thus the assets would directly come under the brokerage firm, but the bank itself would control them. The AUM would not be recorded within the bank.

Advantages

Some noteworthy advantages of the concept of off balance sheet exposure are given below.

- Off-balance sheet financing does not affect the liquidity position of a company adversely.

- Capital expenditures related to the assets used are recorded in the lender’s books.

- Lower fixed assets would result in lower depreciation and hence lower operating expenses.

- Whenever the assets are required, the expense is shown as a rental expense and within the Income statement.

- Purchase and installation of any fixed asset would aid an increase in liability like long-term borrowings or a decrease in reserves. Thus, it retains the liquidity positions of the company.

- The companies with a higher debt-to-equity ratio would tend to benefit from off-balance-sheet financing, as no further capital expenditure is required for new fixed assets.

Disadvantages

Here are some common disadvantages of the concept of off balance sheet transactions. Let us study them in details.

- Using rented machinery retains the company’s liquidity position, whereas any damages or accidental incidents might lead to an increase in maintenance costs.

- The management should clear machinery usage before particularly fixed assets are used. Some other companies bear the ownership of the fixed asset, and they decide the extent of its usage.

- The actual liability of the company is much more compared to what it has shown to the shareholders, creditors, and other third parties associated with it.

- Off balance sheet transactions and OBS financing are allowed under the GAAP, whereas the company has to maintain certain rules prescribed by GAAP.

- Due to the present uncertainty surrounding the credit markets, the rentals could be sky high, and off-balance-sheet financing can lead to higher costs.

- The current picture of the company is not visible unless the off-balance sheet items are taken into account in a detailed manner. It might lead to certain ambiguity among the shareholders and third parties.

Changes In The Off-Balance Sheet

As per the new corporate accounting rule, the companies have to show operating leases on their balance sheet, starting from 1st January 2019 onwards. As per the rule, the companies which used to show the operating leases under footnote have to show the expenses such as office leases, rent for equipment, and cars to the Liability side. It will affect the company’s leverage position. Thus companies having higher operating leases like renting airplanes, ships, etc., would get affected badly as the Liability associated with them would tend to increase. Thus, the investors, financial analysts, quantitative funds, and banks will likely change their mode of evaluating the financial position of a company that has high operating lease assets.

Off-Balance Sheet Vs On-Balance Sheet Items

Both the above are important components of financial reporting and it is necessary to understand the differences between them as given below:

- The main difference lies in the fact of visibility of both in the financial statement. The former does not appear in the financial statement or the balance sheet, whereas the latter does as directly implied, by the terms.

- There are also differences in the type of items for both. In case of the off balance sheet arrangements, the common items are operating lease, contingent liability, etc, but in case of the latter, all other assets and liabilities that are required to be displayed for financial reporting purpose are included.

- Even though both have an impact on the risk assessment and financial health of the business, in case of the off balance sheet arrangements, since the investors and analysts are not able to directly observe them in the balance sheet, there is a possibility of risk and obligations not getting noticed by them, which leads to a false impression and its financial condition. On the other hand, the latter are clearly visible and correct opinion can be formed about them, which gives a true picture to the analysts.

Thus, the above are some basic differences between the two types of items relate to the financial reports that have opposite procedures for reporting.

Recommended Articles

This article has been a guide to Off-Balance Sheet and its meaning. We explain it with examples, differences with on balance sheet, advantages and types. You can learn more about accounting from the following articles –