What Is Leveraged Lease?

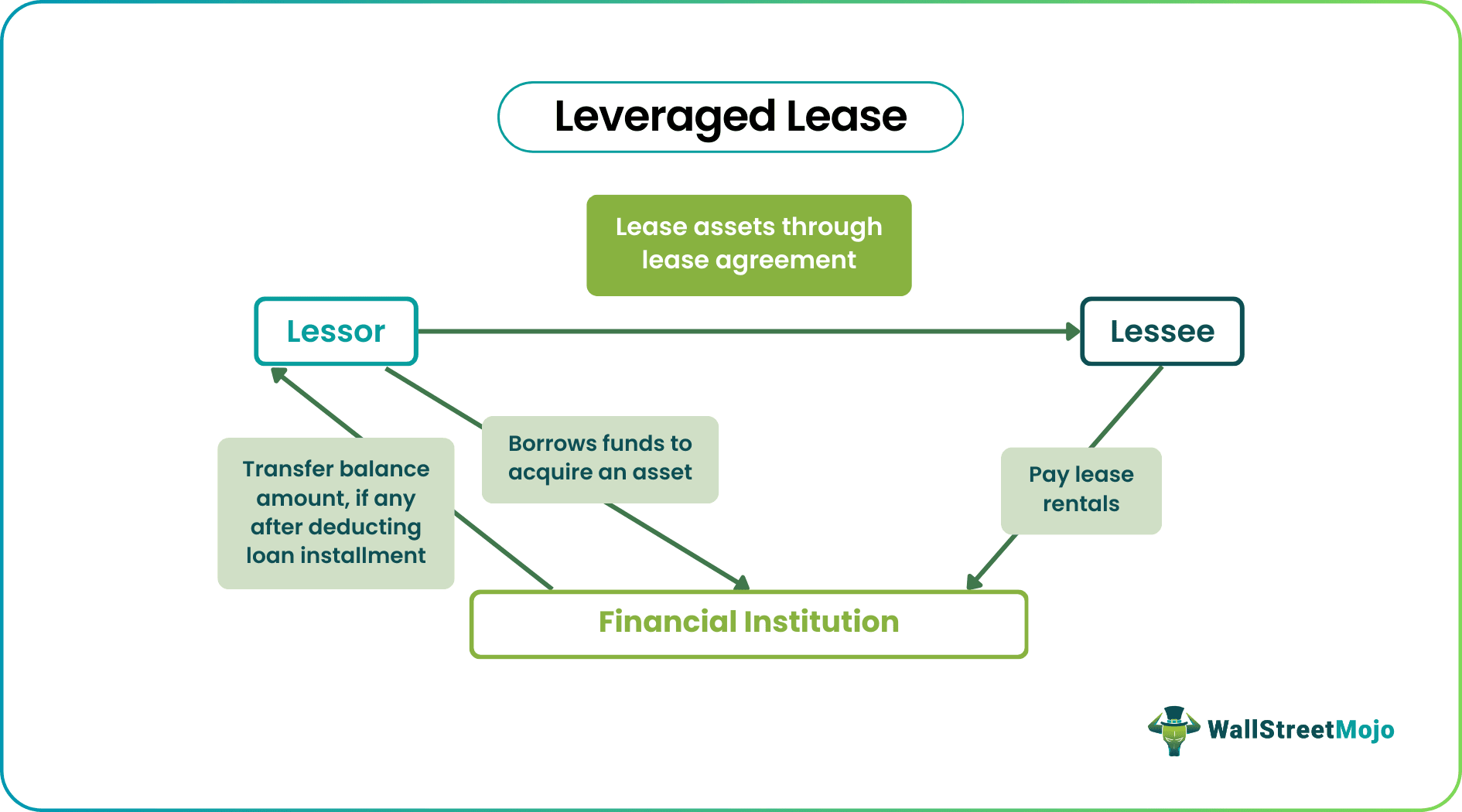

Leveraged lease refers to a lease agreement wherein the lessor acquires an asset partially financed by the financial institutions and leases out the same to the lessee for the agreed lease payments. The lessee transfers the lease rentals directly to an escrow account maintained with the financial institution by the lessor. The financial institution charges the loan installments (principal and interest) from the proceeds available in the escrow account, and the balance amount, if any, gets transferred to the lessor’s account.

Example of Leveraged Lease

- ABC Inc. requires a piece of new equipment for US $ 1 million for 2 years for research purposes. Since ABC Inc. needs the equipment for a relatively short period, buying it would not be the right decision for the company. Hence, the company decided to take the equipment on lease.

- XYZ Inc. is considering buying similar equipment and ready to lease it out to the ABC Inc. post-acquisition. However, XYZ Inc. has only US $ 200,000 in hand and thus wishes to finance the balance of US $ 800,000 from the financial institution @ 7% interest rate.

- This is a transaction of leveraged lease wherein XYZ Inc. is the lessor who has part-financed the equipment from the lender (financial institution) on a non-recourse basis to lease it out to ABC Inc (the lessee).

- In turn, ABC Inc. (the lessee) will pay the lease rentals to the escrow account maintained with the financial institution. After adjusting the principle and interest due on loan, the financial institution remits the excess receivable to XYZ Inc. (the lessor).

Leverage Buyout (LBO) Explained in Video

Accounting Treatment

Accounting Standard Codification 840 (ASC 840) deals with accounting for capital leases in the United States. According to ASC 840, a lease is considered a leveraged lease, if:

The lease agreement satisfies any of the following:

- There will be transfers ownership of the asset at the end of lease term

- The lease allows the lessee an option to buy the asset at a price lower than fair value.

- The lease term is for a major part of (more than 75%) the asset’s remaining economic life.

- The present value of minimum lease payments is more than 90% of the fair value of the leased asset.

AND

The lease agreement satisfy all of the following:

- The collectibility of minimum lease payment is certain and reasonably predictable.

- The lessor is not required to incur additional costs if such costs are not reimbursable.

- The lease involves three parties: a lessor, a lessee, and a lender.

- The lender largely finances the asset on a non-recourse basis.

- The lessor’s net investment declines during initial periods and rises during later periods.

Further, as per ASC 840, in case of a Leveraged Lease, the lessor would recognize the

- Lease rentals receivables, net of principal and interest payments

- Unearned income

- The outstanding (residual) value of the leased property

- The amount of investment tax credit, if any availed.

The lessee simply recognizes the payment of lease rentals as an expense and charge against its profit.

Important Points to Consider in Case of Leveraged Lease

- Usually, in the case of a leveraged lease, the lessor puts a 20%-30% contribution from its funds, and the balance is financed through a bank, financial institution, or third-party lenders for the acquisition of an asset.

- The loan financed by the lenders is generally of non-recourse nature. That means the lessor is not liable for repayment of loan installments in case of a default, and the lender can recover the installments only from the lease rentals paid by the lessee.

- Since the lender will finance the asset on a non-recourse basis, the lender needs to evaluate the lessee’s creditworthiness before the sanction of the loan facility.

- In the United States, the Accelerated Cost Recovery System (ACRS) (as introduced through The Economic Recovery Tax Act 1981) allows the purchaser of the asset to avail Investment Tax Credit. By availing Investment Tax credit, the purchaser can deduct a percentage (as defined in the law)of the asset price from its taxes for the year in which the asset was placed in service.

- Additionally, the purchaser of the asset will also get the tax benefit of the accelerated depreciation deduction.

- The leveraged lease is beneficial for the lessee when the lessee requires the asset for short-term purposes as the lessee can get the asset through lease instead of buying it.

Conclusion

The leveraged lease is a type of capital lease that involves three parties: a lessor, a lessee, and a lender. The lessor acquires the asset through partial equity funding, and the remaining balance from the debt is financed by the lending institution on a non-recourse basis. After the asset’s purchase, the lessor leases it out to the lessee in consideration of lease rentals, which directly goes to the lending institution first, and the balance receivable, if any, gets transferred to the lessor.

Recommended Articles

This has been a guide to What is Leveraged Lease & its Definition. Here we discuss the examples of the leveraged lease along with accounting treatment. You can learn more about accounting from the following articles –