Part of our Accounting for Leases guide

Operating Lease Accounting Definition

Operating Lease Accounting refers to the accounting methodology used for leasing agreements where the lessor retains the ownership of the leased asset. When the lease payments become payable, the lessee recognizes each payment as an expense in its income statement. At the same time, the lessee utilizes the asset for an agreed period, known as the lease term.

Operating lease accounting plays an important role when it comes to managing the transactional affairs relating to the lessee and lessor relationship in this type of lease arrangement. The best part that makes accounting for such leases preferable is the provision it offers to use an asset or property without paying high prices involved in purchasing them.

Operating Lease Accounting Explained

Operating Lease Accounting refers to the recordkeeping concerning an operating lease scenario whereby the lessor owns the property and the lessee only uses it for a fixed time. The lessee records rental payments as expenses in the books of accounts. In contrast, the lessor records the property as an asset and depreciates it over its useful life.

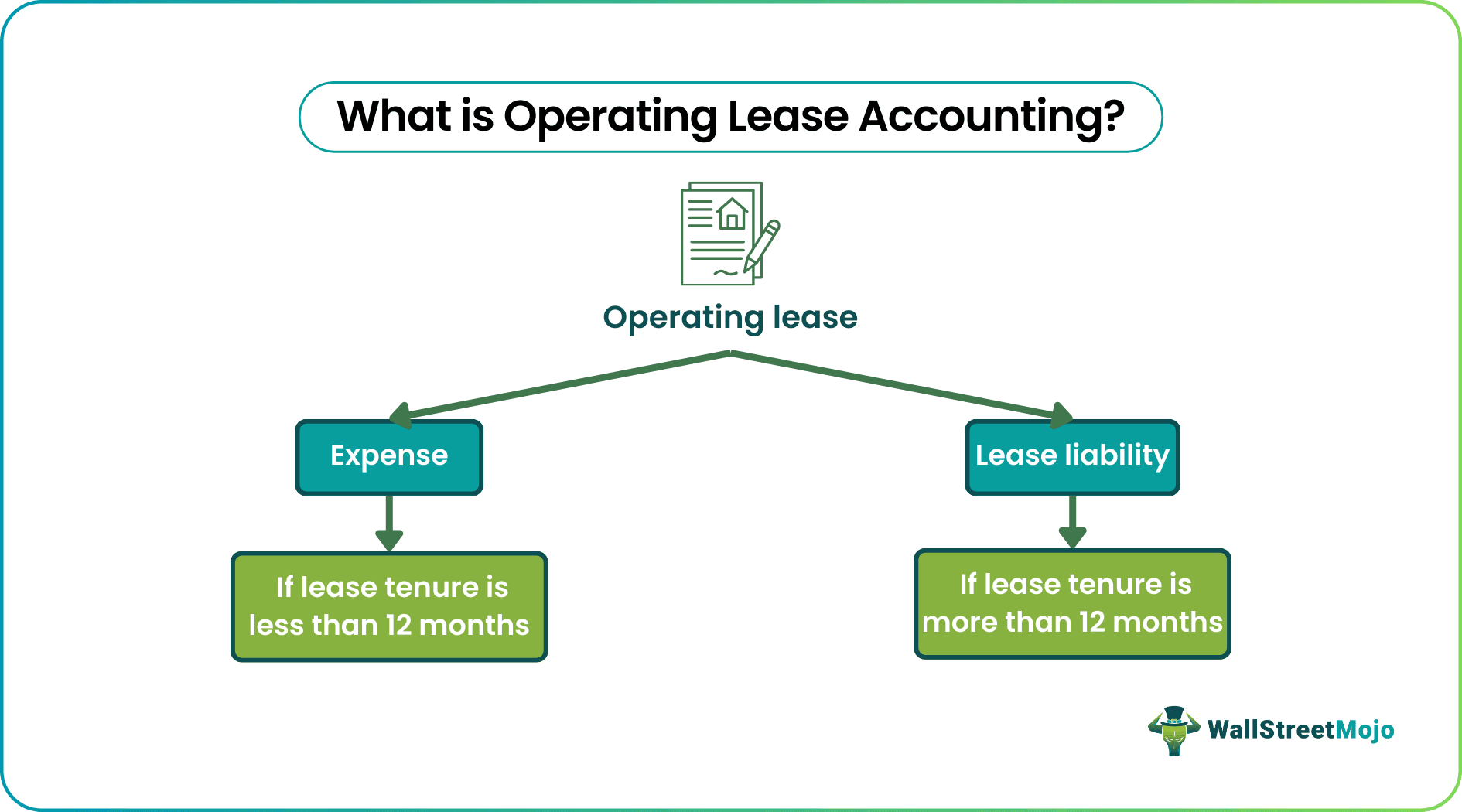

One of the recent developments with respect to this operating lease accounting treatment was observed in 2016 with the evolution of the ASC Topic 842, Leases introduced by the Federal Accounting Standards Board. There were a few guidelines that were expected to follow while making operating lease entries into the balance sheet. Let us have a look at some of them:

- When the leases are for less than 12 months or a year, they should be considered an expense,

- When the lease period is over 12 months or an year, the lessee must consider the expenditure as the lease liability on the balance sheet.

The standards were introduced with an aim to ensure the balance sheet is maintained with utmost efficiency without any confusion. In short, this new guideline aimed to establish a sense of trust amongst users. However, users still had critical views on these guidelines given the partial benefits it offered across corporate sectors. These guidelines seemed to not have a uniform impact on the companies that used it. The effects differed and hence the accuracy and reliability was questioned.

Capital Lease vs Operating Lease – Explained in Video

Examples

Let us consider the following examples to understand how to record operating lease accounting entries for an accurate representation of data:

Example #1

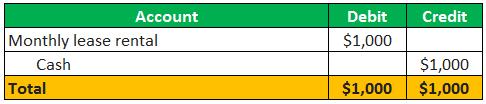

Let us take the example of a company that has entered into an operating lease agreement for an asset and has agreed to a rental payment of $12,000 for twelve months. Show the journal entry for the operating lease transaction.

Since it is an operating lease accounting, the company will book the lease rentals uniformly over the next twelve months, which is the lease term. The monthly rental expense will be calculated as follows,

Rental expense per month = Total lease rental / No. of months

= $12,000 / 12

= $1,000

Now, let us have a look at the journal entry for recording the operating lease rental transaction for each month,

Example #2

Let us take the example of a company named ABC Ltd that has recently entered into a lease agreement with a company named XYZ Ltd for some specialized IT equipment for a 2-year lease that involves payment of $20,000 at the end of 1st year and $24,000 at the end of 2nd year. The present value of the minimum lease payments is $35,000, while the equipment’s fair value is $50,000. At the end of the lease term, ABC Ltd has to return the equipment to XYZ Ltd, and there is no scope for extension of the lease term. Further, as per the lease agreement, the lessee also can’t purchase the asset at a lower price after the expiry of the lease term. The equipment has a useful life of 4 years. Show the journal entry for both ABC Ltd (lessee) and XYZ Ltd (lessor) at the end of 1st year and 2nd year.

The above-mentioned lease agreement can be treated as an operating lease because of the following:

- The agreement does not allow the transfer of ownership of the equipment from the lessor to the lessee after the expiry of the lease term

- The term of the lease is equal to 2 years, which is less than 75% of the total useful life of the equipment

- The present value of the minimum lease payments is $35,000 is 70% of the fair value of the equipment, which is well below the generally accepted threshold of 90%.

- Since there is no option to purchase the equipment at a lower price after the expiry of the lease term indicates, there is no bargain purchase option.

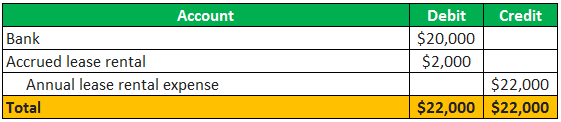

Since it is an operating lease, ABC Ltd will book the lease rentals uniformly over the next two years. The yearly rental expense will be calculated as follows,

Annual lease rental expense = Average of lease rental for Year 1 and Year 2

= ($20,000 + $24,000) / 2

= $22,000

Now, let us have a look at the journal entry of ABC Ltd,

At the end of the 1st year

At the end of the 2nd year

Now, let us have a look at the journal entry of XYZ Ltd, which is exactly the opposite of ABC Ltd,

At the end of the 1st year

At the end of the 2nd year

Example #3

Let us take the example of a company that has entered into an operating lease agreement for three years with an initial lease payment of $2,000, followed by lease payments of $1,500, $1,000, and $1,000 at the end of the first second and third year respectively. Calculate the interest expense component of the lease payment for the current year.

Let us calculate the debt value of the lease payments as follows,

Debt value of lease payments = PV of lease payments in year 1, year 2 and year 3

= $1,500 / (1 + 5%)1 + $1,000 / (1 + 5%)2 + $1,000 / (1 + 5%)3

= $3,199.4

Depreciation on the leased asset = Debt value of lease payments / No. of years

= $3,199.4 / 3

= $1,066.5

Therefore, the interest paid on the lease obligation for the current year can be calculated as,

Interest paid on leased asset = Lease payment in the current year – Depreciation on the leased asset

= $2,000 – $1,066.5

= $933.5

Therefore, the interest component of the lease payment in the current year is $933.5.

Impact

The impact of the accounting can be seen on the balance sheet, income statement as well as cash flow statement. Let us check the effects of operating lease accounting on different financial statements that a company generates:

Balance Sheet Impact

There is no impact on the Balance Sheet of Lessee

Effect on Income Statement

Lease payments will be treated as Expense in the Income Statement.

Effect on Cash Flows

Total lease payment reduces cash flow from operations

Operating leases do not affect the lessee’s liabilities and hence, are referred to as off-balance-sheet financing.

Footnote disclosure of lease payment for each of the next five years is required.

Recommended Articles

This has been a guide to Operating Lease Accounting & its definition. Here, we explain the concept along with its examples, and its impact. You can learn more about accounting from the following articles –