Part of our Accounting for Leases guide

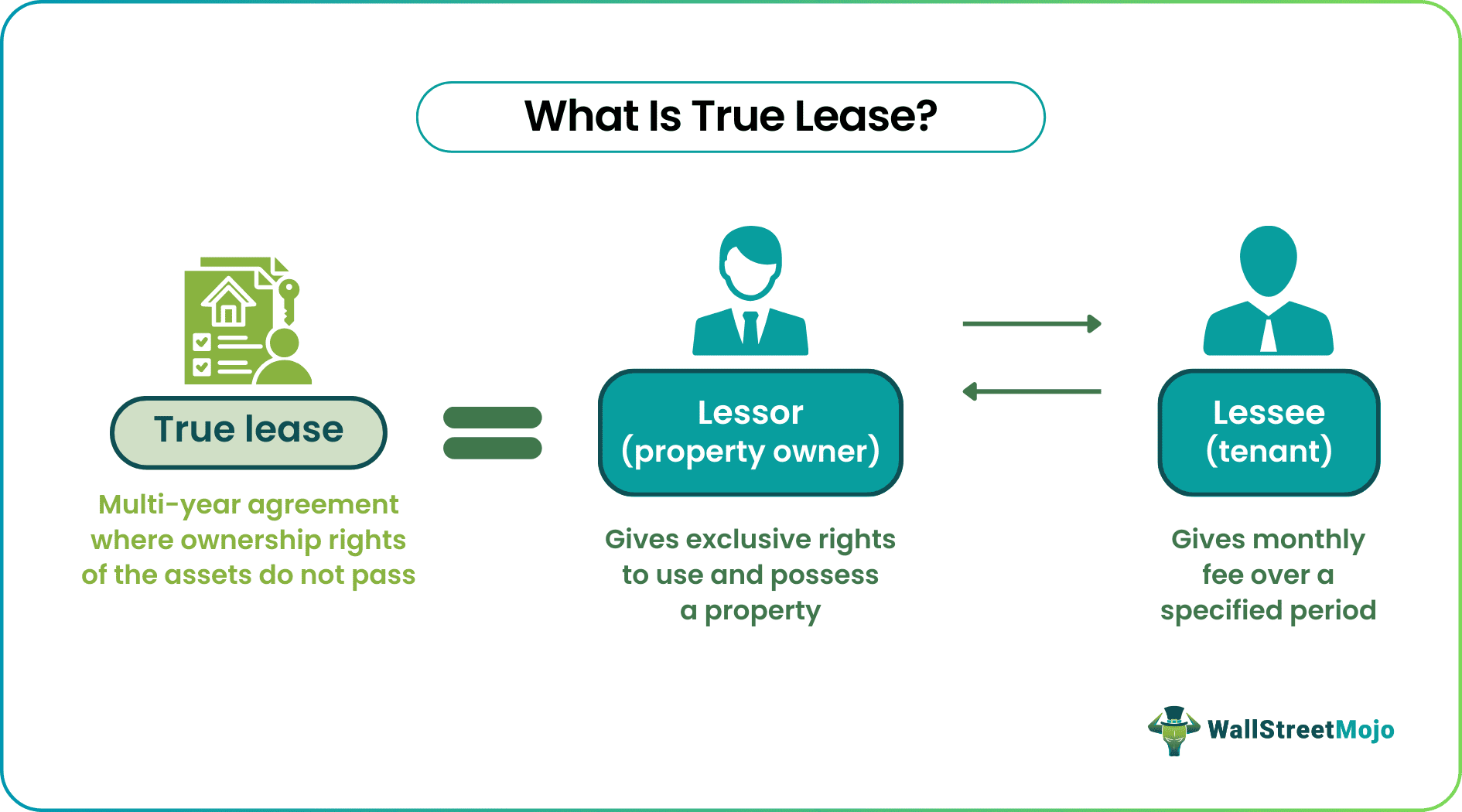

What Is True Lease?

A true lease in real estate refers to a legal agreement between the lessor (property owner) and the lessee (tenant) in which the former allows the latter to use and access the property for a specific period in exchange for a payment at a regular interval, mostly on a monthly basis.

A true lease does not require the ownership rights to be passed from the lessor to the lessee. The advantage of such a lease is that it allows the parties to enjoy tax benefits. This is why it is also known as a tax lease.

- A true lease definition refers to a real estate agreement where the property owner or lessor will rent their property to the lessee for a pre-determined period (usually a year) at an agreed-upon monthly rental payment.

- Also known as a tax lease, it is opted for due to the tax advantage it can offer the parties.

- The lessor can claim depreciation over the leased asset, while the lessee can deduct the monthly rental payments as capital expenses from the taxable income.

True Lease Explained

A true lease is an arrangement used to claim tax benefits, commonly seen in real estate and business contexts. In a tax lease, the lessor rents their property or equipment to the lessee for a specified period, usually a year, with agreed-upon monthly payments. The lessee can use the property without intentionally damaging it, ensuring its condition for the lessor at the end of the lease term. Ownership rights remain with the lessor in a tax lease, and tax advantages are available for both parties.

Regarding taxation and true lease guidelines from Internal Revenue Service (IRS), the lessor can depreciate the asset over its economic life and claim investment tax credits, as the IRS stipulates. However, the rental payments received by the lessor are subject to taxation, while the lessee can deduct them as capital expenses.

To determine if a transaction qualifies as a tax lease, the IRS has established a tax lease test with four criteria:

- The lessee cannot purchase the asset for less than its fair market value (FMV), which is the price for which the product can be sold in an open and competitive market.

- The expected residual value of the asset should be at least 20%, and the lessor must bear all residual risks. Residual value refers to the worth of an asset after it is fully depreciated or at the end of the lease term.

- The asset must be a general-use property; its expected remaining useful life should be at least 20% of its original estimated useful life.

- The asset must meet additional IRS requirements for profit, excluding tax benefits, minimum equity investment, and cash flow.

By meeting these criteria, a transaction can be considered a tax lease, allowing the parties to benefit from tax advantages outlined by the IRS.

Examples

Let’s study a few examples of tax leases.

Example #1

Consider this hypothetical example. Amy leases equipment to Jake for a year. The monthly rent, as agreed by them, is $500. They entered into a tax lease agreement. Thus, Amy could claim depreciation and tax credit, while Jake could seek his monthly payments as capital expense deductions.

Example #2

New rules by the IRS have made leasing electric vehicles (EVs) more profitable than selling one. All clean vehicles (electric, hybrid, fuel cell cars, and trucks) are eligible for federal tax credits regardless of weight, cost, and assembled location. The only limitations, for now, include the minimum battery capacity requirements.

The required capacity for light-duty vehicles under 14,000 pounds is 7kWh, and for heavier commercial vehicles, it is 15kWh. However, these tax credits only apply to EV producers and leasing companies, not the end consumers. The leasing companies can pass the credits to consumers by charging lower leasing rates. Nevertheless, it is up to them.

True Lease vs Financial Lease

Let us understand the differences that highlight the contrasting characteristics of true and financial leases.

- Tax leases offer tax benefits for both the lessor and lessee. The lessor can claim depreciation on the asset over its economic life and may be eligible for investment tax credits. Meanwhile, the lessee can deduct the rental payments as capital expenses. In contrast, financial leases are primarily a financing method for the lessee and generally do not come with specific tax benefits.

- A true lease involves an asset usually bought for the lessor’s personal or business use but leased to the lessee. But in a financial lease, the asset is bought purely for the lessee’s use.

- In a true lease, the ownership is not transferred to the lessee. At the end of the leasing agreement, the lessor retains the rights over the asset. However, in a financial lease, the ownership is transferred to the lessee once they make total payments (principal + interest) to the lessor.

True Lease vs Capital Lease

True and capital leases are distinct leasing arrangements. Let’s understand the differences between them.

- In a true lease, the lessor retains ownership of the leased asset throughout the lease term and beyond. However, in a capital lease, the lessee treats the asset as if they own it for accounting and tax purposes. Ownership is effectively transferred to the lessee.

- In a true lease, the lessor takes on the risks related to asset ownership, including value fluctuations and obsolescence. In contrast, a capital lease places the responsibility of risks and rewards on the lessee, who treats the asset as their own.

- True leases are primarily focused on providing the lessee with the use of the asset, while capital leases often have a financing component. Capital leases are often used when the lessee intends to own the asset.

Frequently Asked Questions (FAQs)

1. Can a true lease be used for various types of assets?

True leases are versatile and applicable to real estate properties, machinery, vehicles, etc. The lease terms and conditions are customized to suit the asset being leased, ensuring a tailored agreement for each situation.

2. Is a TRAC lease a true lease?

Yes. A terminal rental adjustment clause (TRAC) is a leasing agreement on vehicles in commercial use for more than half of the time. It allows the lessee to avail assets at low rates. Further, it also gives the parties tax benefits akin to a true lease.

3. What is the difference between a true lease and a conditional sale?

In a conditional sale agreement, the ownership passes to the buyer only after the payment is made in full. But they can still use the asset. In a tax lease, the ownership may or may not pass to the lessee after the contract period.

Recommended Articles

This article has been a guide to What Is True Lease. Here, we compare it with financial & capital leases, and explain it with its examples. You may also find some useful articles here –