Part of our Fixed Assets and Depreciation guide

Difference Between Depreciation and Amortization

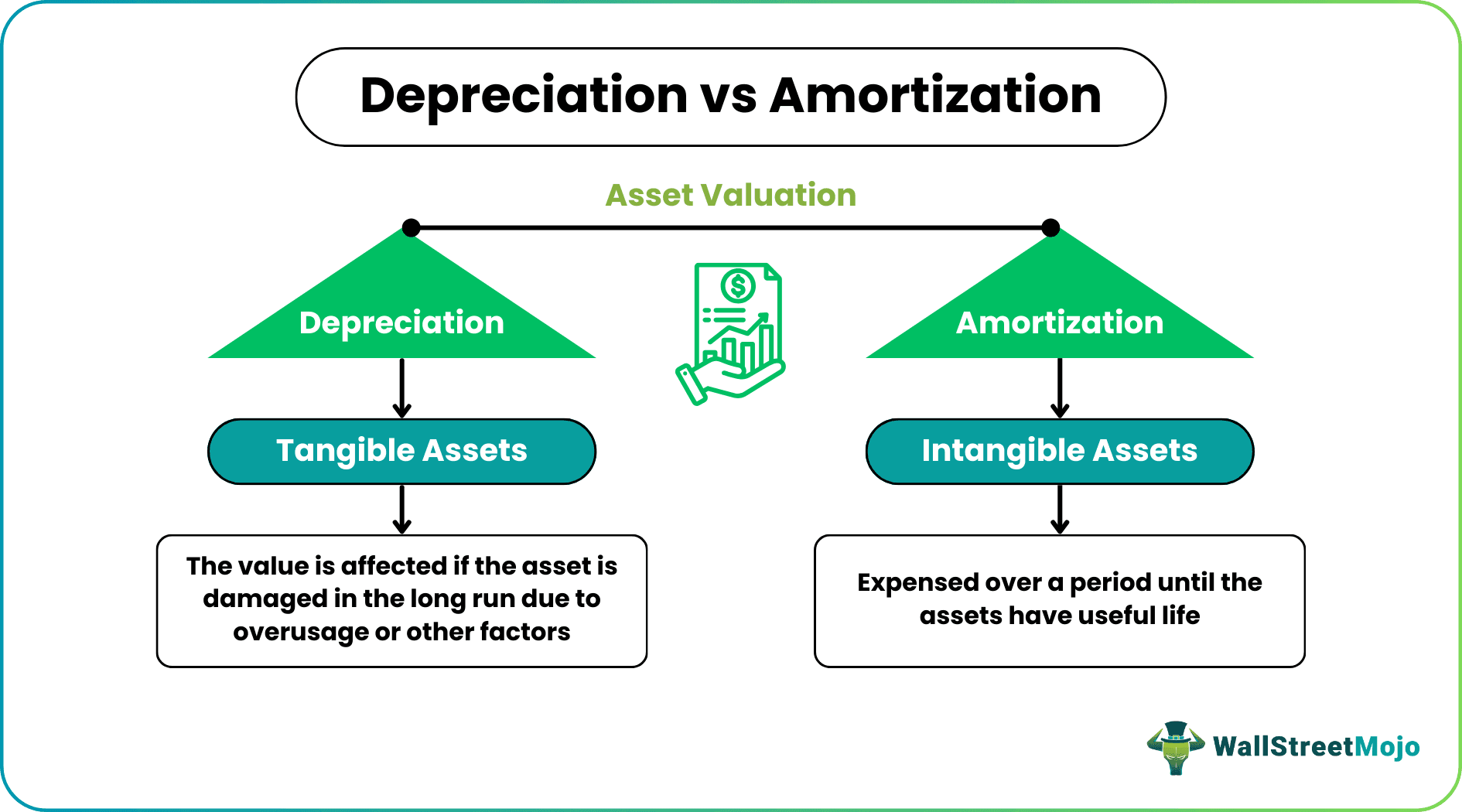

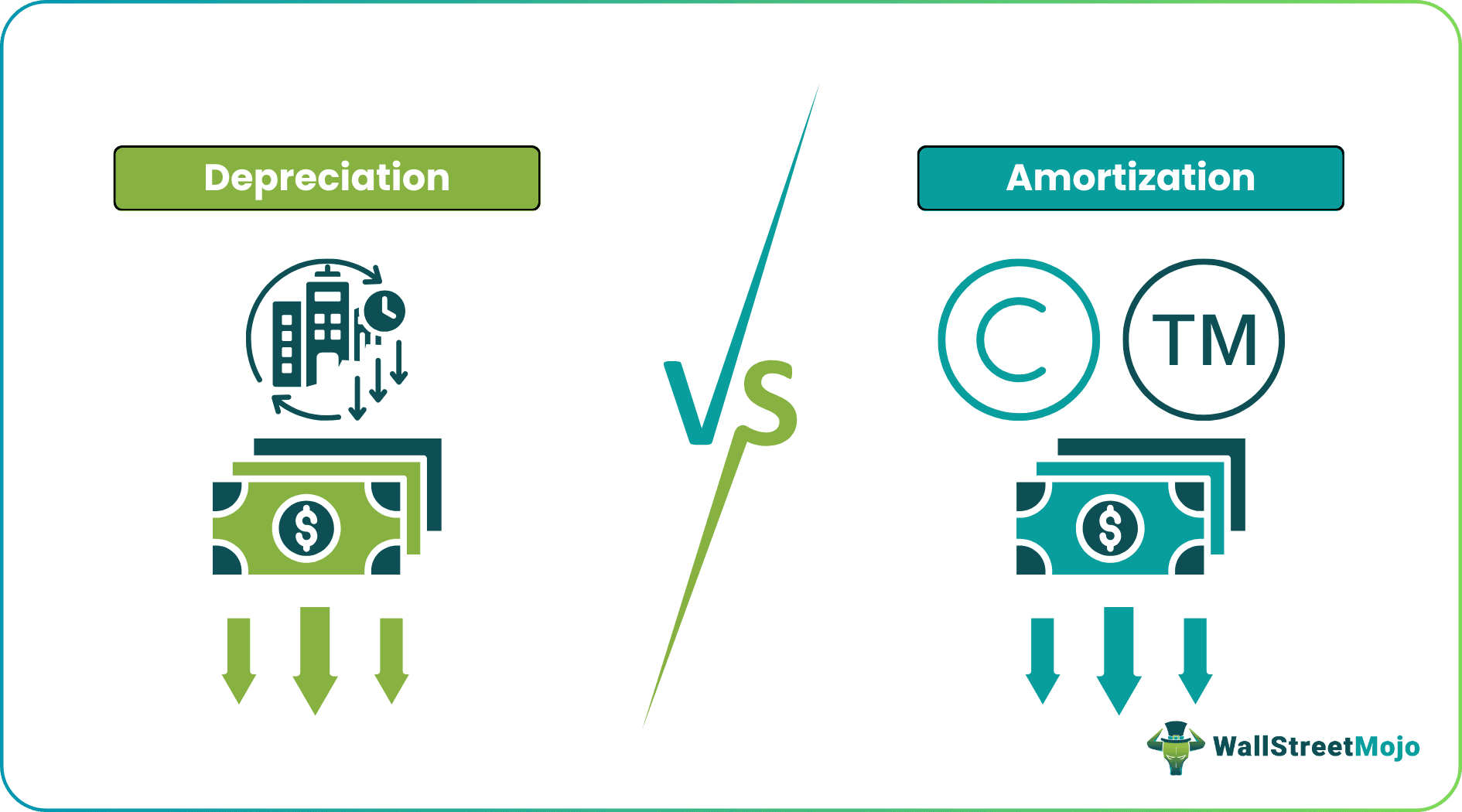

Depreciation is the reduction in the value of the fixed assets due to normal wear and tear, usage or technological changes, etc. It applies to tangible assets. In contrast, amortization refers to the process under which the cost of different non-physical assets of the company are expensed over a specific period and thus applies only to the company’s intangible assets.

Assets are the backbone of any business. No business can run without owning an asset, as it generates economic returns and revenue over its life. Therefore, it must be depreciated or amortized in the books of accounts to recognize its true value. Companies use methods like depreciation or amortization to depreciate the asset over its useful life.

- Depreciation refers to an asset’s gradual wear and tear that reduces its initial value. Amortization, on the other hand, is the general reduction in the value of an intangible asset over its useful life.

- The most basic and essential difference is that depreciation is accounted for tangible assets, whereas intangible assets are recorded using amortization. Depreciation also includes salvage value/scrap value.

- Methods to calculate depreciation are Straight-Line Method, Declining Balance, and Double Declining Balance Method. For amortization, the Bullet and Balloon methods are used.

- Both theories are non-cash expenditures, and businesses must remember the importance of asset management not to lose labor efficiency.

Depreciation vs. Amortization Comparative Table

| Depreciation | Amortization |

| A technique to calculate the reduced value of the tangible asset is known as depreciation. | A technique to measure the reduced worth of intangible assets is known as amortization. |

| Allocation of the cost principle | Capitalization of the cost principle |

| The different methods of depreciation are a straight line, reducing balance, annuity, sum of years, etc. | The different methods to calculate the amortization are straight line, reducing balance, annuity, increasing balance, bullet, etc. |

| Applies over tangible assets | Applies over intangible assets |

| The governing accounting standard of depreciation is AS-6. | The governing accounting standard of amortization is AS-26 |

| Examples of Depreciation asset are Plant Machinery Land Vehicles Office Furniture | Examples of Amortization assets are Patents Trademark Franchise Agreements Cost of issuing bonds to raise capital Organizational costs Goodwill |

| The cost of depreciation is shown in the Income statement | The cost of amortization is also shown in the income statement. |

| Non-cash item | Non-cash item |

What Is Depreciation?

Depreciation refers to the expenses of an asset that are fixed and tangible. These are physical assets that are reduced each year due to wear and tear. This amount is chargeable to the income statement.

The properties, including buildings, equipment, tools, machinery, etc. let businesses manufacture and produce goods that they sell to generate revenue. Any damage to these ultimately affects the value of those properties, causing depreciation. For example, in a damaged plant resale, buyers would hardly take interest in buying it unless the sale value is low. This shows how deprecation affects a business premise.

What Is Amortization?

On the other hand, amortization is the expense of an asset over its useful life. However, amortization applies to intangible assets over the life of the asset. Therefore, this amount is also chargeable to the company’s income statement.

Some examples of these intangible assets are copyrights, trademarks, patents, etc. These are to pay for the time until which the assets are useful. The expense related to the maintenance of these assets remains the same throughout the useful life of that property.

Depreciation vs Amortization: Features

The difference between the two asset valuation types in terms of their features are listed below:

- The critical difference is that the assets expensed in depreciation are tangible assets, and those expensed in amortization are intangible assets.

- There is usually no salvage value involved in amortization, whereas, in depreciation, there is a salvage value in most cases.

- There are various methods used by the business to calculate depreciation. However, there is only one method of amortization that companies generally use.

- The objective of depreciation is to prorate the cost of the asset over its useful life. On the other hand, amortization aims to capitalize on the cost of the asset over its useful life.

The only similarity in depreciation and amortization is that they are both non-cash charges.

Depreciation vs. Amortization Infographics

Let’s see the principal differences between depreciation vs. amortization.

Depreciation vs. Amortization: Methods

Both processes are non-cash expenses but need to be created like a provision as assets have a particular life and need to be replaced if the business does not want to lose its labor productivity. That is why using these two accounting concepts is crucial and paramount. These two are often identical terms and are commonly used interchangeably, but different accounting standards govern them.

A business should realize the importance of these two accounting concepts and how much money should be set aside to purchase an asset in the future. The business assets should always be tested for impairment at least annually, which helps the company know the real market value of the asset.

The impairment of assets also helps the business to forecast the cash requirement and at which year the probable cash outflow should occur.

#1 – Depreciation

- Straight-line method – The same depreciation expense is charged in the income statement over the asset’s useful life. Under this method, the profit over the year will be the same if considered for depreciation.

- Declining Balance Method – Under this depreciation method, the depreciation amount is charged in the income statement in the closing balance of the previous year of the asset, i.e., Asset value- Depreciation for an earlier year = Closing Balance. Under this depreciation method, the profit for the year will be lesser in the initial years and more in the later years when considered in light of depreciation.

- Double Declining Balance method (DDB) – This is the most accelerated method of depreciation that counts twice as much of the asset’s book value each year as an expense compared to the straight-line depreciation. Thus, the formula used here is – 2 * straight-line depreciation percent * book value at the beginning of the period.

#2 – Amortization

- Bullet Method– Under this amortization method, the intangible amortization amount is charged to the company’s income statement all at once. This method recognizes the expense all at once. Generally, firms do not adopt this method as it largely affects the numbers of profit and EBIT in that year.

- Balloon Payments– Under this method, the amount deducted at the beginning of the process is less. Still, significant expense is charged to the income statement at the end of the period.

The methods for depreciation are also meant for amortization if the latter is evaluated for loans and advances. In that case, the above methods of amortization schedule of loans are used.

Frequently Asked Questions (FAQs)

How do depreciation and amortization affect the financial statements of a company?

Depreciation and Amortization affect the equity and balance sheet of the company, respectively. Due to depreciation, the value of a company’s equity gets affected, mostly reducing. On the other hand, due to the yearly amortization of assets, the balance sheet is affected as it reduces the asset side of the statement.

Is software depreciated or amortized?

Software is considered a fixed physical asset for several companies; it is depreciated instead of amortized.

Can goodwill be depreciated or amortized?

Goodwill is the market credibility of a company and, thus, is intangible. Therefore, goodwill will be amortized. Moreover, goodwill can be amortized for over 10 years or less.

Recommended Articles

This article is a guide to Depreciation vs. Amortization. We explain the differences between them in terms of features and valuation methods with infographics. You may also have a look at the following articles –