Part of our Fixed Assets and Depreciation guide

What is the Written Down Value Method?

The written Down Value method is a depreciation technique that applies a constant rate of depreciation to the net book value of assets each year, thereby recognizing more depreciation expenses in the early years of the asset’s life and less depreciation in the later years of the life of the asset. In short, this method systematically accelerates the recognition of depreciation expenses and helps businesses recognize more depreciation in the early years. It is also known as the Diminishing Balance Method or Declining Balance Method.

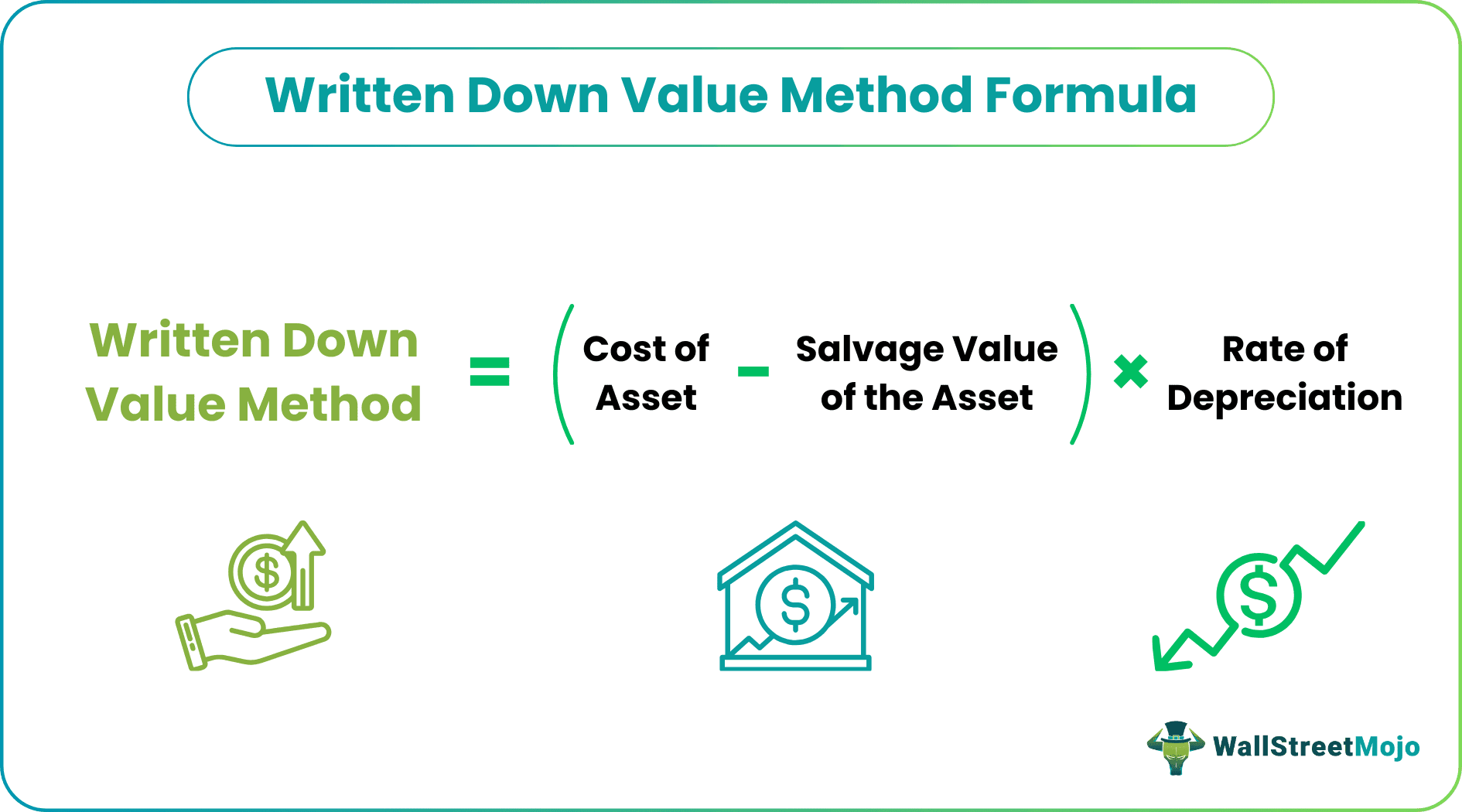

The formula is as follows:

Written Down Value Method = (Cost of Asset – Salvage Value of the Asset) * Rate of Depreciation in %

How to Calculate WDV Depreciation?

Let’s understand the same with the help of an example.

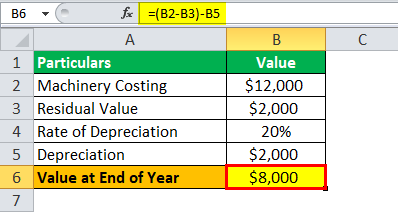

Whitefield Company purchased a Machinery costing $12000 with a useful life of 7 years and a residual value of $2000. The rate of Depreciation is 20%.

Solution:

Calculation of written down value (WDV) of depreciation can be done as follows –

Depreciation = ($12,000 – $2,000) * 20%

Depreciation = $2000

Calculation of the end of the year can be done as follows –

Value at End of Year = ($12,000 – $2,000) – $2,000

Value at the End of Year = $8,000

Depreciation as per the Written down Value Method is calculated as follows:

Similarly, we can do the calculation, as shown above, for years 2 to 5.

Whitefield depreciated the Machinery using WDV Method, and as we can observe, the depreciation expense amount was higher during the initial years and kept reducing as the asset got older.

Written Down Value Method Video

Written Down Value Method vs. Straight Line Method of Depreciation

One of the most common and popular types of WDV Method is the Double Declining Balance Method. This method applies depreciation two times the Straight-Line Rate. The method is suitable for assets that quickly lose their value and, as such, require higher depreciation. The word “Double” signifies this aspect.

Let’s understand the differences between WDV and Straight-line depreciation with the help of an example.

Mason Limited purchased a Machinery costing $25000 for a specific project and expected useful life of 5 years. The Machine is expected to have a residual value of $5000 at the end of its useful life.

Solution:

Calculation of written down value of depreciation can be done as follows –

Based on the above facts, the Straight-Line Rate is as follows:

- Straight Line Rate = (Cost of Machine-Residual Value) / Useful life (in years)

- Straight Line Rate = ($25000-$5000) / 5 = $4000

The Straight Line Depreciation Rate can be done as follows –

- Straight Line Depreciation Rate= $4000 / ($25000-$5000) = 20%

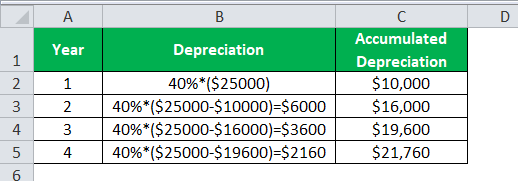

- Double Declining Balance Rate= 2 * 20% = 40%

So, the calculation of depreciation can be done as follows –

- Depreciation = 40% * ($25,000 – $10,000) = $6,000

- Accumulated Depreciation = $10,000 + $6,000

- Accumulated Depreciation = $16,000

Depreciation Schedule as per Double Declining Balance is shown below:

Similarly, we can do the calculation, as shown above, for years 3 and 4.

Advantages

- The written down Value Method helps determine the asset’s depreciated value, which helps determine the price at which the asset should be sold.

- It applies a higher amount of depreciation in the initial years of the asset’s useful life. It is an ideal method to record the depreciation of assets, which lose their value quickly. An example of such assets could be any Technological development software by an IT company. By recognizing accelerated depreciation in the early years, the business can determine its fair market value on the Balance Sheet before the technology becomes outdated.

- Higher Depreciation during initial years results in reduced taxes or deferred taxes to later years for the business on account of lower Net Income but increased Cash profits as Depreciation is a Non-cash expense.

Disadvantages

- Written Down Value Method recognizes higher depreciation during the early years and may not be an ideal method of depreciation for those assets with uniform utility throughout their useful life and don’t suffer from the risk of obsolescence and technology change.

- Higher Depreciation expenses due to this method result in reduced Net Income for the business.

How does WDV Depreciation Offsets Repair Requirements?

The method is based on the premise that certain assets not just have limited use and need to be depreciated with higher values during their useful life to show the true fair value of the asset on the balance sheet. Still, this depreciation method is also apt for those assets requiring higher repairs in the later stages of the asset life. A balancing act is also achieved by applying higher depreciation during the initial years when the repair requirement is less and lesser depreciation during later years when the repair requirement is more.

Let us take an example to illustrate this concept.

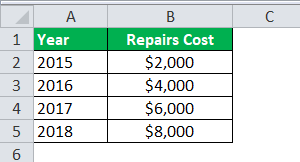

Mayor Inc purchased machinery costing $80000 in 2014 with a useful life of 4 years with no residual value at the end of the useful life. The company has incurred the following expenditure in the form of Repairs of the machinery during the last five years:

Solution:

Let’s understand the point discussed above using the two different Depreciation methods, i.e., WDV and Straight Line Depreciation Method. We will understand how using WDV and applying higher depreciation during the initial years when repairs require less and lesser depreciation during later years when a repair requirement is more of a balancing act.

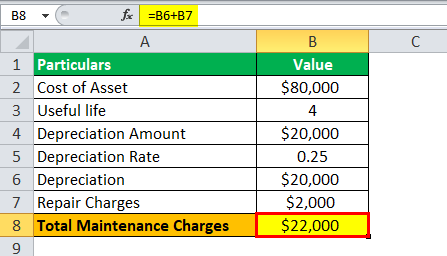

Calculation of written down value of depreciation can be done as follows –

The Depreciation Amount calculation–

The Depreciation Amount = Cost of Asset-Residual Value/Useful life ( in years)

- Depreciation Amount = $80000 / 4 = $20000

- Depreciation Rate = $20000 / $80000 = 25%

So, the calculation of depreciation is as follows –

- Depreciation = $80000 * 25% = $20,000

The Total Maintenance Charges will be –

- Total Maintenance Charges = $20,000 + $2,000

- Total Maintenance Charges = $22,000

Similarly, as shown above, we can do the calculation for the year 2016 to 2018.

Thus we can observe how the Written Down Value method ensures that higher depreciation expenses in initial years and lower depreciation expenses in later years help offset higher Repairs and Maintenance charges as the asset becomes older and needs more such expenses.

Conclusion

The written-down Value method is appropriate for matching expenses to revenues. Most long-lived assets generate more benefits in the early years of their economic life and fewer benefits in the later years. It ensures the same by more Depreciation expenses in the early years and fewer depreciation expenses in the later years of the asset’s useful life.

Recommended Articles

This article has been a guide to the Written Down Value Method. Here we discuss how to calculate WDV Depreciation, practical examples, and explanations. Here we also discuss its advantages & disadvantages. You may learn more about accounting from the following articles –