Commodity Derivatives Meaning

Commodity derivatives are investment vehicles allowing investors to reap profits by investing in commodities without owning them. A commodity is any item that can be exchanged or traded. On the other hand, its derivative comprises the value of the underlying assets.

Derivatives are available as forwards, options, futures, and swaps, with the commodities like gold, copper, cotton, and crude oil, as underlying assets. These commodity derivatives help manage price risks that are likely to affect the producers, manufacturers, etc.

- Commodity derivatives are the financial tools that help investors spend on commodities and profit from them without exercising any ownership rights.

- These derivatives can be traded over the market or used as exchange-traded derivatives.

- The commodity derivative contracts used in the market are forwards, options, futures, and swaps.

- These investment tools help assess market sentiments, investors’ interest, and market confidence via the rise and fall of commodity prices.

Commodity Derivatives Explained

The commodity derivatives market offers investors a chance to invest directly in the commodities, not through the firms that trade them. These are invested in as forwards, options, futures, or swaps. However, whichever form they are traded in, the transaction occurs at a predetermined price and decided date.

Risk givers and risk takers participate in the transaction of these derivatives. The former is the one who has physical exposure to the commodities, realizes the associated risk, and tries to pass it on to someone else by selling or purchasing the position on the stock exchange. On the other hand, risk takers are not exposed physically to the commodity but are ready to take risks by selling or buying the positions. While the risk givers are hedgers here, the risk takers are the investors.

The derivatives transaction can either be undertaken via the spot market, where the assets could be transacted on the spot or within two business days, or in the futures market or forwards market, where the transactions are booked for a future date.

Features

The features that make commodity derivatives trading one of its kind include its presence in multiple forms, its trading mechanism, and the settlement process.

- Types: These derivatives are available as contracts of different forms:

- Forwards contract – A private agreement whereby the buyer promises to purchase those derivatives.

- Futures – These are similar and standard forward contract formats for commodities that trade on exchanges.

- Options – This agreement offers the holders the right to buy or sell the underlying asset on a predetermined future date.

- Swaps – It is a contract using which two parties agree to exchange cash flows.

- Mechanism: The market is for those who do not require the items for their use but invest in them per the price movements only to reap profits.

- Settlement: The market involves the exchange of funds and goods, and a Clearing House handles the settlements related to commodity derivatives.

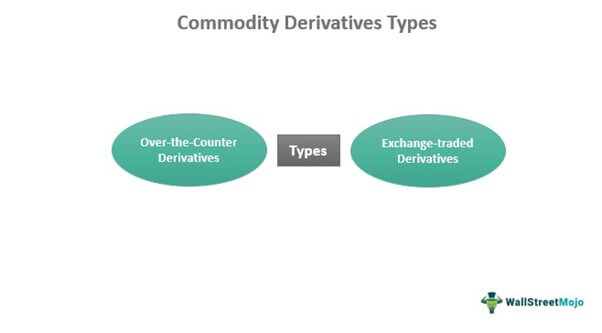

Types

Based on how these are traded, the derivatives are classified into two types – Over-the-Counter (OTC) and Exchange Traded commodity derivatives.

The OTC derivatives are structured contracts whereby two parties transact outside the exchange. On the other hand, exchange-traded derivatives are standardized contracts for the transaction to occur on a stock exchange.

Examples

Let us consider the following examples to understand properly what exactly is commodity derivatives:

Example #1

Though tomatoes are cheap in July and expensive in January, people can’t buy them in July for delivery in January since the item would spoil by then. Therefore, the July price reflects the tomato supply and demand in July. On the other hand, the forward price for January indicates the market’s supply and demand expectations in January. This shows how July tomatoes are a commodity different from January tomatoes.

Example #2

The Russian-Ukraine tension has significantly impacted the financial sector, making energy-driven entities utilize their derivatives per their exposure to risk in the market. The energy market has been volatile since March 2022, causing large margin calls, which have boosted the liquidity risks for the derivatives participants. One of the major reasons behind the triggered margin calls is the commodity derivatives instruments that seems to have taken the initial and variation margin calls to a significant high by late 2022.

Importance

These derivatives come with many benefits, making them an important financial instrument. Some of their advantages include the following:

- As a frequently used input in the production processes, they help accurately measure market volatility.

- As a result, they help in identifying the effects of the rise and fall of the prices in various industries.

- They help in proper risk assessment.

- These indicate the market sentiments, investors’ interest, and market confidence as reflected via the rise and fall of commodity prices.

Commodity Derivatives vs Financial Derivatives

Commodity derivatives and financial derivatives are not the same. The differences between the two are as follows:

| Category | Commodity Derivatives | Financial Derivatives |

|---|---|---|

| Involves | Physical exposure to underlying assets | No physical exposure |

| Settlement | Physical settlement | Mostly cash settlement |

| Nature | Bulky; need a proper storage facility | Not bulky; no issues with storage |

| Quality concerns | Quality plays a vital role | The quality of assets is not a major concern. |

Frequently Asked Questions (FAQs)

Who regulates the commodity derivatives market?

The Commodity Futures Trading Commission (CFTC) regulates such derivatives markets in the United States. The agency was formed in 1974 to take care of the derivatives market and its mechanism while dealing with futures, swaps, and specific options contracts. In India, the Securities and Exchange Board of India (SEBI) looks after this market.

Are commodity derivatives securities?

Yes, these are securities that investors invest in without having to own the same. Instead, the buyers buy them as futures, options, forwards, or swaps and gain the right to trade and profit from them at a predetermined price and future date.

What is the pricing application of commodity derivatives?

These derivatives help in price risk management. While it protects farmers when commodity prices decrease, it ensures food processors are not affected by the increasing costs. This is due to the provision allowing investors to book deals for a future date at a fixed price. In short, these commodity derivatives help manage price risks likely to affect the producers, manufacturers, etc.

Recommended Articles

This article has been a guide to Commodity Derivatives & its meaning. We explain their features, types, and examples and compare them with financial derivatives. You may also find some useful articles here: