Table of Contents

What Is An Electronic Check (E-Check)?

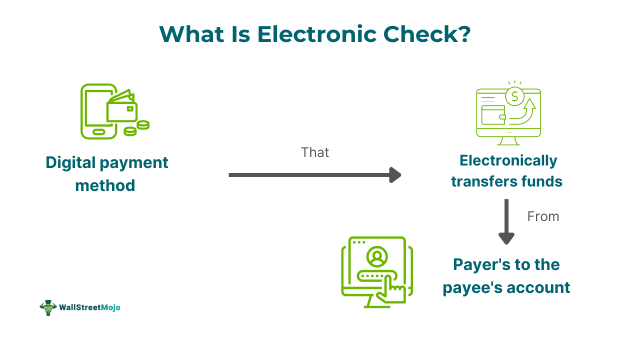

An electronic check is a check sent digitally. It is an electronic payment method that can be accessed online or by phone. Similar to a normal check, the funds are withdrawn from the payer's account and transferred to the payee's bank account.

E-checks are convenient due to their ease and efficiency. They help streamline transactions and detect fraud and better suit a fast-paced, growing environment than a traditional way of banking. Additionally, they can be accessed from anywhere in the world without having to visit a bank. They also reduce paper waste.

Key Takeaways

- Electronic checks or e-checks are a digital version and a better version of traditional checks. They allow electronic fund transfers between the payer and the payee's bank account through the ACH network.

- They are convenient, easy, and reduce paperwork. They are easier to process and secure. Businesses can attract consumers through a variety of options they provide through such modes of payment.

- The method, however, has drawbacks, such as technological issues, the threat of online security, and hacking. Additionally, some people do not accept payments through this mode, which reduces the desirability of the payment system.

Electronic Check Explained

An electronic check (e-check) is a digital version of a traditional paper check. While traditional checks use paper, e-checks use digital networks to make payments. In this digital process, money is withdrawn electronically from the payer's account and deposited electronically into the payee's account.

The payer initiates the e-check payment by providing their bank account information (account number and bank routing number) to the recipient (payee). This information is stored securely. The payee's bank or payment processor verifies the details for accuracy and validity. After verification, the payment is processed through the Automated Clearing House (ACH) network, transferring the specified amount from the payer's account to the payee's account.

Institutions that accept electronic check payments provide forms for customers to fill out the required details. Once the information is entered, the processing, including the transfer of money, is handled automatically. This eliminates the need for manual processing and physical documentation, and e-checks do not require physical storage.

E-checks cannot be misplaced like physical checks and have encryption and security measures in place. They use authentication methods such as digital signatures, multi-factor authentication, and other verification techniques to authorize account holders and prevent forgery. However, e-checks cannot guarantee 100% security as digital forms of payment are subject to attacks. The strength of security depends on the protection systems in place, which can vary between institutions involved in the transactions.

Examples

Let us look at a few examples to understand the concept better.

Example #1

Let's say Dan is a business owner of a small furniture company that needs to pay $50,000 to a supplier for raw materials. Dan logs into his online banking portal and selects the option to pay through an electronic check. He inputs the supplier's name, email address, and bank account details (including the account number and routing number) for electronic check verification. These details are required to ensure the electronic check is processed correctly. Once the information is verified, the payment is initiated. On the supplier's end, the funds are typically received within 3-5 business days after the electronic check clears.

Example #2

Clementine Jones, a customer of PNC Bank, faced a four-month ordeal after PNC issued electronic checks to Wells Fargo and Citi Cards. Despite receiving confirmation of the payments, Wells Fargo mistakenly cashed both checks, leaving Citi Cards unpaid and Jones out $1,778. Frustrated by the lack of resolution and the blame-shifting between the banks, Jones sought help from 2 Wants To Know. After multiple calls, visits, and intervention from the news team, Wells Fargo attempted to resolve the issue, but PNC initially remained unresponsive. Eventually, public and social media pressure prompted action, highlighting the challenges and frustrations customers can face with electronic check errors.

Benefits

Some of the benefits of e-checks are given below.

#1 - Time associated

E-checks do not need any paperwork, and working at the click of a button eliminates the need for too many people and processes involved in execution. Hence, they reduce the paperwork and processing time, making them efficient.

#2 - Saves money

When paperwork is eliminated, the associated costs, including the cost of papers and stationery, are eliminated. Additionally, the cost of storing these is also saved. The transaction fees associated with online transfers are also less than the costs of card transactions.

#3 - Convenience

E-checks are convenient and easily accessible from one's home or anywhere in the world through the internet. The need to visit banks personally is reduced. Sometimes, specific processes can be automated, such as monthly payments to loans. These factors make it a convenient option.

#4 - Benefits for businesses

Businesses benefit from an expanded customer base. Businesses can attract more customers through the variety of payment methods they offer. This can reduce the rate of cart abandonment, resulting in more sales and profit.

Drawbacks

Given below are some of the drawbacks of e-checks.

#1 - Security risks and frauds

Online transactions are vulnerable to attacks from hackers. They try to steal the information and finances of people using them, so caution must be maintained at all times while accessing them.

#2 - Technological issues

Since everything has to happen over the internet, there is dependence on technology. Hence, the speed of electrical availability and the infrastructure to avail the services are all important, and disruption in any of the factors is undesirable.

#3 - Grass root penetration

Electronic checks are no doubt a widely accepted payment method. However, some people still prefer payment through cash or cards. There can be outlets that do not accept e-checks due to skepticism or unfamiliarity; this is an issue of acceptance. Additionally, there is a segment of people, the underprivileged, who need the opportunity to access these methods. This is also a disadvantage.

Electronic Check Vs. Wire Transfer Vs. Ach

The differences between both the concepts are given as follows.

| Basis | E-Checks | Wire Transfers | ACH (Automated Clearing House) |

|---|---|---|---|

| Concept | E-checks are a payment method where a check is presented electronically instead of in paper form. | Wire transfers are a method of electronically transferring funds from one bank account to another. | ACH is an electronic funds transfer system used to process payments and transfers between banks. |

| Process Initiation | Initiated by account holders for bill payments and transactions. | Initiated by individuals or businesses for one-time or urgent transfers. | Initiated by businesses or individuals for regular or scheduled payments. |

| International Transactions | E-checks can be used for international transactions, but speed and fees may vary. | Wire transfers are commonly used for both domestic and international transactions with generally faster processing. | ACH has limited international capabilities and is primarily used for domestic transactions. |

| Speed | Processing can take several days, depending on the banks involved. | Typically processed within hours to the same day, depending on the service and location. | Usually takes 1-3 business days for processing. |

| Fees | Generally lower fees compared to wire transfers; fees vary by bank. | Often have higher fees, especially for international transfers. | Typically lower fees compared to wire transfers, especially for batch transactions. |

| Usage | Commonly used for bill payments, business transactions, and recurring payments. | Often used for high-value or time-sensitive transactions. | Commonly used for payroll, direct deposits, and recurring payments. |

| Security | Secure, but still subject to fraud and errors. | Highly secure, but large amounts make it a target for fraud. | Secure, with strong fraud prevention measures, but still subject to risks. |

| Reversibility | Difficult to reverse once processed, requiring bank intervention. | Can be difficult to reverse, particularly once the funds are received. | Reversible within a specific timeframe, especially for erroneous transactions. |