Origination Meaning

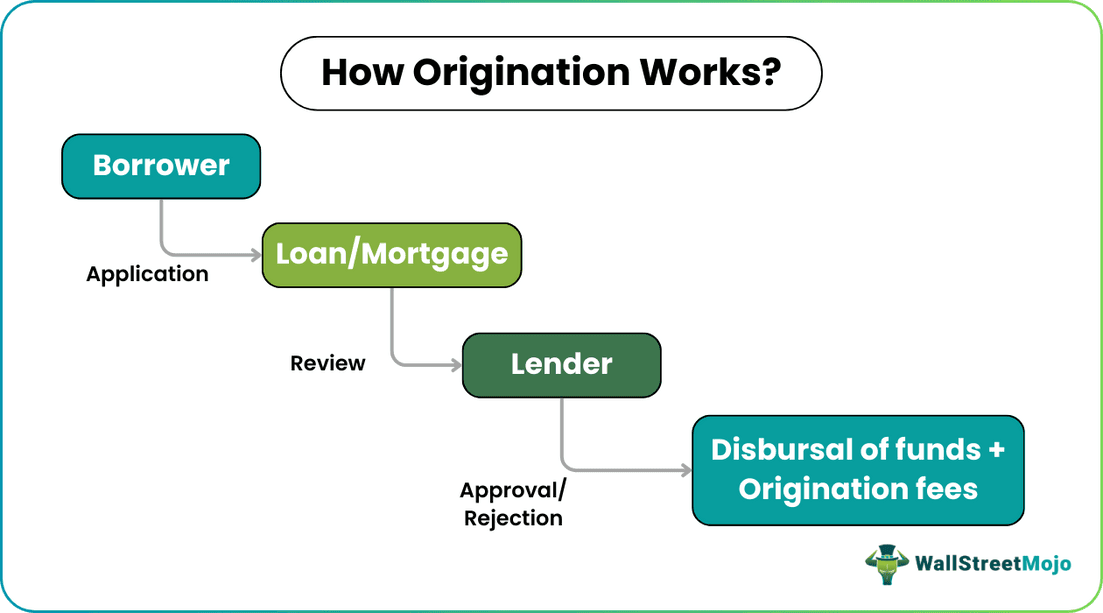

Origination in finance refers to the borrower applying for a loan or mortgage and getting it approved by the lender. It includes a loan application and submission of required financial information by the borrower and a review of the relevant documents by the lender before approving or rejecting the application.

The process differs depending on the loan type and risks, the regulator, the lender’s policy, and other factors. An originator handles the entire process, from pre-qualification to disbursal of funds. The borrower usually pays a fee to secure the loan. A government agency, such as the Federal Deposit Insurance Corporation (FDIC), oversees multiple stages in obtaining a loan or mortgage.

Key Takeaways

- Origination definition refers to the process of a borrower applying for a loan or mortgage and a lender processing that application. The borrower applies, along with the relevant financial documents, which the lender analyzes before approving or rejecting it.

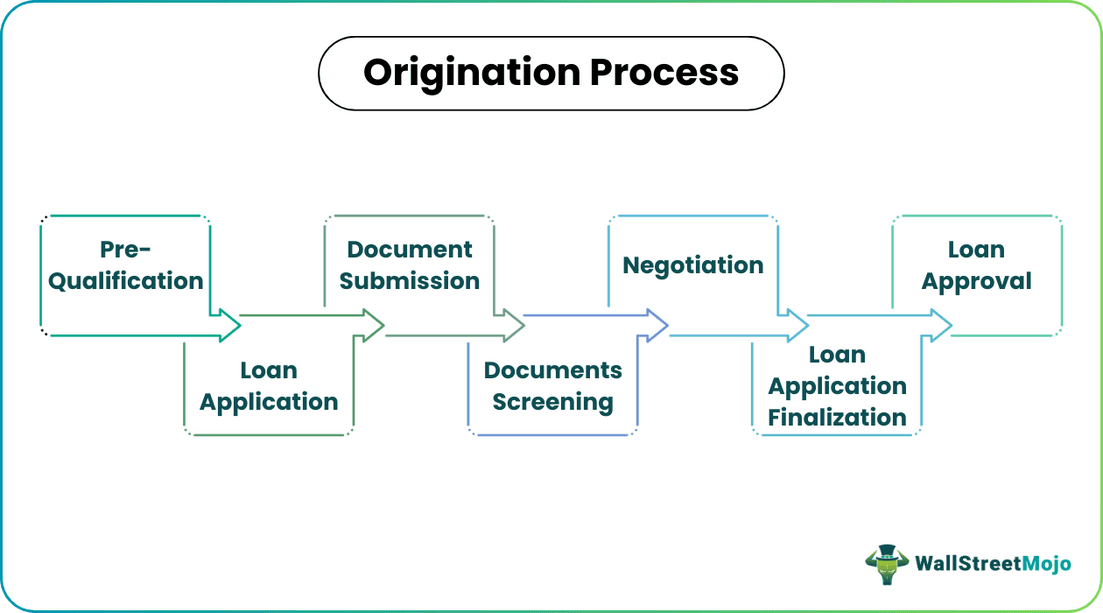

- It occurs in several stages, including pre-qualification, loan application, documents submission and screening, negotiation, underwriting, and loan approval.

- The lender charges a fixed percentage of the loan or mortgage amount, known as the origination fee, from the borrower to process the loan.

- An underwriter verifies the borrower’s income, financial statements, debts, and credit history to establish their eligibility and ability to repay the loan.

How Does Origination Work?

Origination of a loan or mortgage signifies services offered by the lender to the borrower till its processing. It covers everything from the application to the disbursal of the requested fund. A loan officer, also known as a loan originator or mortgage broker or a dedicated department at a bank, manages from pre-approval of loan to granting the amount. Once approved, the lender charges a fee to process the application and cover related costs.

Let us discuss in detail various stages to understand what does origination mean:

#1 – Pre-Qualification

It is the initial stage of the process, during which the borrower submits relevant financial information and papers to the lender. The lender requires this information to determine whether the borrower qualifies for the loan or mortgage and estimate the interest rate. This process can take place online or offline (in person or over the phone). The financial details requested for the processing of the loan application include:

- Source of income

- Credit score/report

- Financial statements (profit-and-loss)

- Bank balances

- Bank statements

- Tax returns

- Debts

- Purchase and sale contract

- W-2 forms

- Additional documents outlining the borrower-lender arrangement

When the borrower submits this data and information, the lender processes it for a loan pre-approval.

#2 – Loan Application

The next step in this process is filling out an application form on paper or electronically. It mainly contains information about the type of the mortgage or loan and the income and property that it intends to cover. The loan originator reviews the application for the accuracy of the information and performs the required legal paperwork.

#3 – Documents Submission

The borrower provides documentation to get the income-related information, including financial statements and tax returns verified by the loan officer. Sometimes, it is a part of the previous two steps, depending on the lender’s policy.

#4 – Documents Screening

This step involves screening the application and requisite documents by the lender before approving or rejecting the loan or mortgage. Besides income and financial history, the officer verifies the credit score of the borrower.

#5 – Negotiation

Before signing the loan or mortgage agreement, the borrower gets the chance to negotiate on favorable terms and conditions. However, the lending institution and the borrower’s financial status play a crucial role in it.

#6 – Loan Application Finalization

Following agreement on terms, the processor submits the loan or mortgage application and documentation for underwriting before approval. In this step, the underwriter evaluates all the information to determine if it follows the lender’s guidelines. It also ensures if the borrower can pay back the loan amount and interest rates. The lender finalizes the application after the underwriter gives a green signal.

#7 – Loan Approval

It is the last step in the process. Soon after finalizing the loan or mortgage application, the loan originator sends it to the lender for approval. The officer sets closing date and orders the appraisal of the loan purpose.

Based on the status of the application, the lender concludes to either approve or reject it. A low credit score leads to rejection of the loan, while a high credit score drives to eligibility checks based on the documents submitted.

The application is then subsequently reviewed by a quality assurance team for regulatory compliance. It is the final review of the loan application before processing funds. Finally, the lender disburses the loan or mortgage after confirming that everything meets the lending criteria.

Origination Fee

An origination fee refers to the fees usually set in advance and charged by the lender to execute a loan. It could be a percentage of the loan or mortgage amount, but it varies depending on the lender, the type of loan, and the amount being lent. A home loan, for example, may have less fee (between 0.5% and 1%) than a personal loan (between 0% and 6%).

This fee compensates the lender for processing applications, preparing documents, and underwriting. Generally, the lender gains profit based on the fee and any money collected by servicing the loan.

The borrower has the option of negotiating the fee in exchange for a higher interest rate. Also, the lender can reduce the cost when the loan or mortgage is for a substantial sum and a long-term. Additionally, a solid credit score and a steady source of income may entitle the borrower to a reduced fee.

At times, the lender splits this fee into processing fee and underwriting fee. The borrower can pay it in full as part of loan closing expenses, or the lender can deduct it from the loan amount.

For example, someone obtains a personal loan worth $9,000 at a 1% processing fee. The lender may require the borrower to pay $90 upfront or deduct it from the loan amount, i.e., $9,000 minus $90 = $8,910.

Origination Examples

Let us understand how origination works with a few examples:

Example #1

Lisa, a software engineer, plans to buy a lake-view house valuing at $250,000. She has $100,000 in savings and will need an additional $150,000 to purchase the property. Therefore, Lisa decides to initiate the mortgage loan origination and applies at a local bank. She fills out the application and submits the required financial information to the bank.

The loan originator, processor, and underwriter review her application and documentation before disbursing funds. They take an in-depth look at her source of income, debts, tax returns, credit score, and bank statements. The bank also arranges for a closing date and an evaluation of the property in question.

Upon finding the application compliant with lending regulations, validating the documents submitted, and inspecting the property, the bank offers Lisa a $150,000 mortgage loan on favorable terms due to good credit ratings. However, she pays a 1 % processing fee, i.e., $1,500 upfront for securing the loan.

Example #2

Usually, it takes 46 days on average for traditional mortgage lenders in the United States to complete the process. Also, it costs between $2,000 and $2,500 for each loan application. However, incorporating digital collaboration technologies into lending processes may lead to more secure, faster (up to 15 to 40%), and cost-efficient (up to 10%) mortgage origination.

Borrowers can connect with originators through an integrated portal for application and documentation processing and underwriting. Also, loan officers, processors, underwriters, and quality assurance teams can coordinate the progress of loan applications.

Example #3

The onset of the COVID-19 pandemic, coupled with record-low mortgage interest rates, led to a significant increase in mortgage loan applications. It made it difficult for lenders to keep up with increased volume while combating online mortgage fraud risks. However, lenders can deal with unprecedented challenges by embracing big data and automation to detect fake borrowers and safeguard themselves.

Origination In Banking

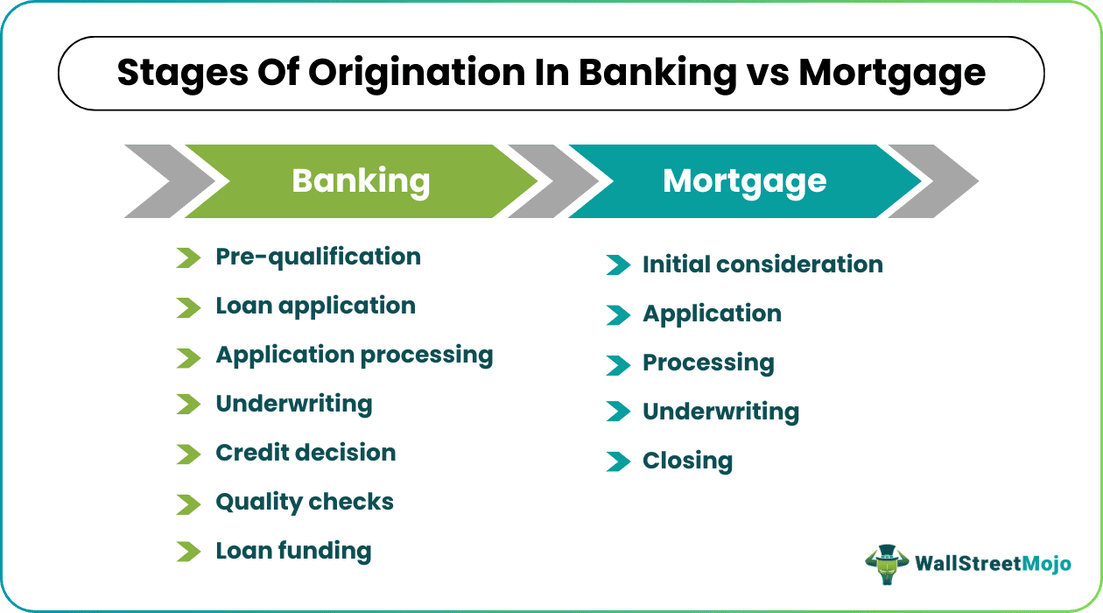

In banking, origination refers to the steps taken after a borrower applies for a loan and the bank processes it. There are seven steps to it:

- Pre-qualification

- Loan application

- Application processing

- Underwriting

- Credit decision

- Quality checks

- Loan funding

The loan origination system (LOS) has recently become a buzzword among banks and credit unions. It automates and manages the end-to-end steps in processing a loan, from filling out the application to underwriting, approval, documentation, pricing, funding, and administration. Although each bank and credit union has different procedures for approving loans and maintaining a lending relationship, they all follow a similar approach.

Professionals involved in origination – such as loan officers, underwriters, and compliance specialists- often rely on structured training to stay current with industry standards. Platforms like OnCourse Learning offer targeted programs that help them meet licensing and regulatory requirements efficiently.

Origination In Mortgage

A mortgage is a type of loan typically used to finance a property. The mortgage origination comprises five steps:

- Initial consideration

- Application

- Processing

- Underwriting

- Closing

When the borrower applies for a mortgage, the loan originator forwards their application and other supporting documents to an underwriter. The mortgage loan originator can work independently or with the lender. The underwriter reviews the loan scenario and the documents before approval to check:

- The borrower’s ability to repay the loan and down payment

- Value of the property in question

- Source as well as the amount for the down payment

Besides, the borrower’s income, savings, credit history, debt, and mortgage guidelines play a vital role in the loan approval.

Frequently Asked Questions (FAQs)

What is Origination?

In finance, origination refers to the process of a borrower applying for a loan or mortgage and the lender approving it. The procedure entails the borrower submitting a loan application and appropriate financial papers, the lender reviewing the application, and acceptance or rejection of the application. The process varies, depending on the loan type and risks, the regulator, the lender’s policy, and other variables.

What is an origination fee?

An origination fee is a cost levied by the lender to the borrower to execute the loan and cover other expenses associated with processing a loan. Typically, it varies with the lender, loan type, and amount. For example, it could be between 0.5% and 1% for a home loan and between 0% and 6% for a personal loan.

What are the various stages of loan origination?

The loan origination process includes:

1. Pre-qualification

2. Loan Application

3. Documents Submission

4. Documents Screening

5. Negotiation

6. Loan Application Finalization

7. Loan Approval

Recommended Articles

This has been a guide to what is origination and its meaning. Here we discuss how origination works in banking and mortgage along with fees & examples. You can also have a look at the following articles to learn more –