Part of our Banking Services and Operations guide

What Is A Bounced Check?

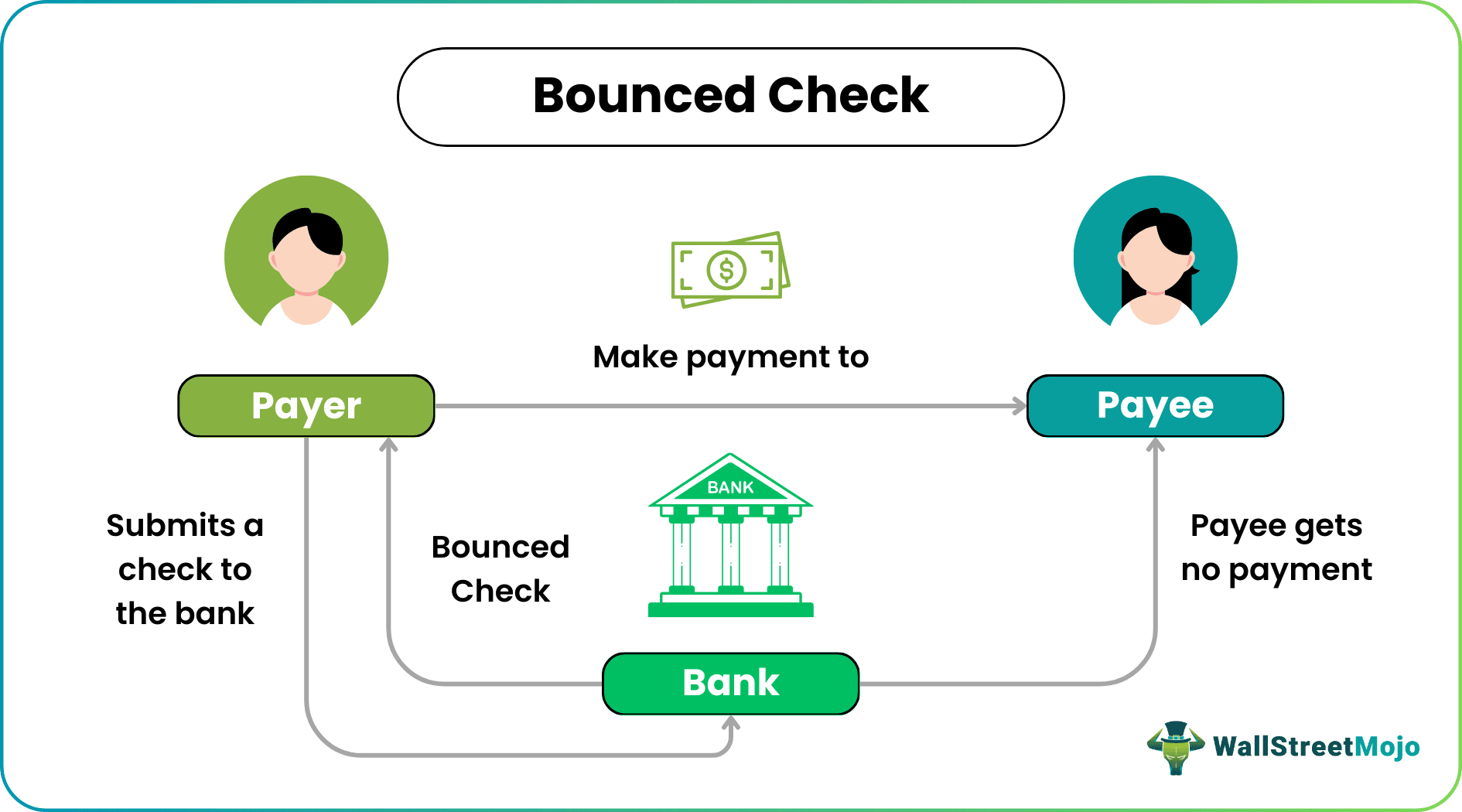

A bounced check is a situation when the processing of a dispensed check becomes unsuccessful by the bank and gets returned without any processing due to insufficient funds in the payer’s account or data or signature mismatch. It has serious monetary and financial consequence.

The check stands void between the parties and the bank. This may result in a penalty fee that the account holder has to pay to the bank. The payee of the check also does not get the fund resulting in legal problems, reduced credit score, loss of faith on the payer, etc.

- A bounced check is returned by the bank due to insufficient funds, incorrect data, signature mismatch, or other reasons and becomes void between the parties.

- The bank sends a “check return memo” to the issuer stating the reasons for the payment failure. The check can be resubmitted within three months of the return date.

- If the issuer fails to pay, the payee may sue legally.

- Bouncing a check is a criminal offense and can lead to imprisonment, monetary penalty, and negative effects on credit scores.

Bounced Check Explained

A bounced check is a situation in which the bank is not able to transfer funds from the payer’s account to the payee due to a lack of money, incorrect data, or a signature, etc on the check. Since the check cannot be honored, is returned to the payer, and receiving a bounced check, there is a bounced check charge, which the payer has to pay.

Sometimes banks may offer overdraft facilities to account holders to prevent such situations. However, repeated check bounces may lead to legal problems or a hefty monetary penalty since the payee does not get their due on time. The payer may eventually have to change the mode of payment due to a loss of faith from customers.

When the check gets bounced, the bank sends the “check return memo” to the issuer specifying the reasons for non-payment. On receiving a bounced check, the issuer or the holder of the check can resubmit the check within three months of the date of the check’s return by the bank. If the issuer fails to make the payment, the payee can take bounced check legal action and sue the payer legally.

This rule applies if the payer makes some payment and the bank bounces due to insufficient funds.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

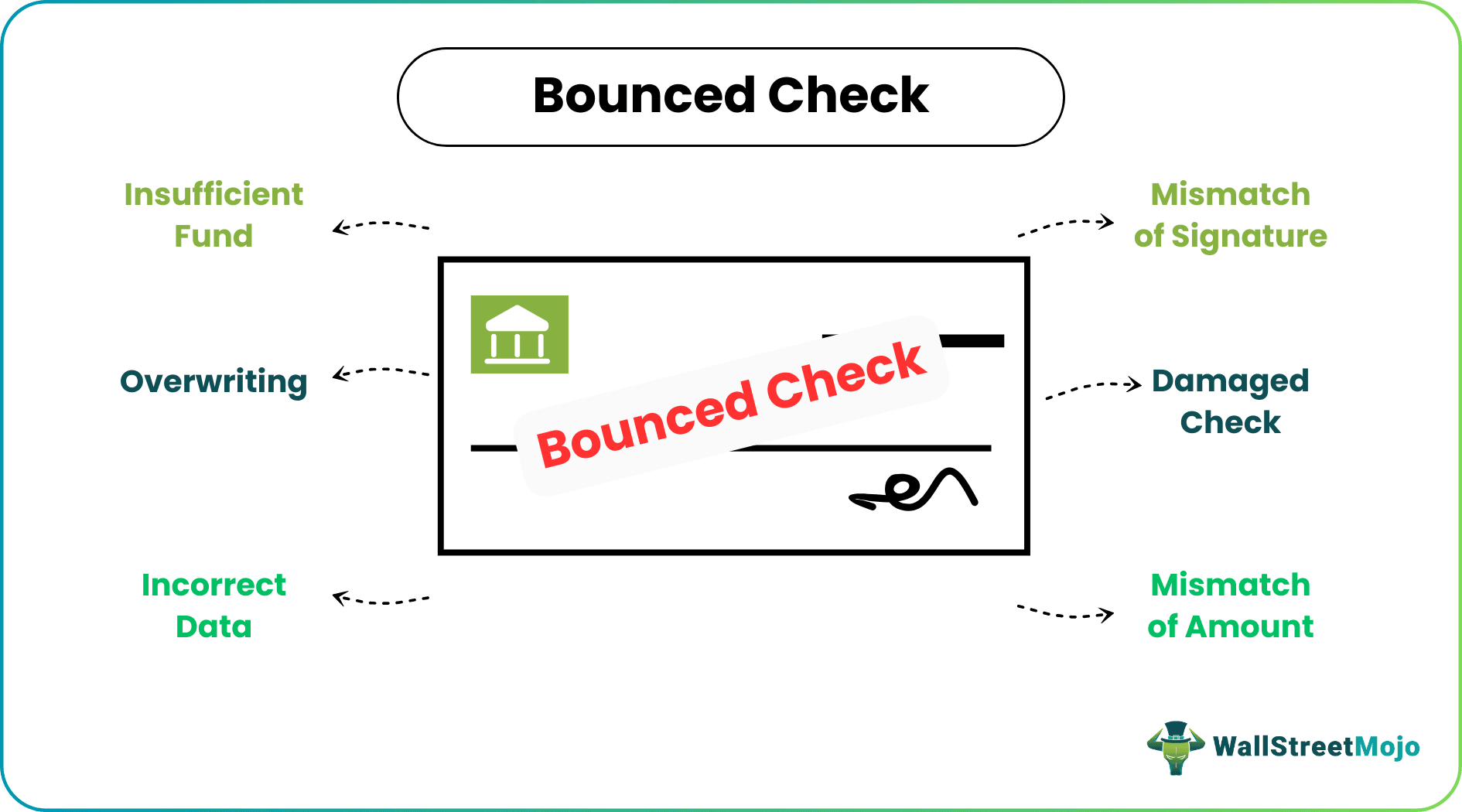

Reasons

The following are the reasons: –

- Insufficient fund is the major reason when the amount in your bank account is lower than the check issued.

- It can bounce when the data on the check is incorrect such as the account holder’s name, etc.

- Overwriting is also one reason. If the check is overwritten, it leads to the bouncing of the check.

- Mismatch of signature, i.e., when the signature on the issued check is different from the account holder’s signature as per bank records.

- Damaged check becomes disfigured, and banks do not accept them the same.

- Mismatch of the amount written in words differs from the amount reported in numbers.

Example

Let us understand the concept with an example.

Let us take the example of Peter. He has $50 in total in his savings account maintained with Bank of America and needs to pay Mr. Alex $75. So now issues a check to Alex for $75 for the Bank of America.

Alex presented the check issued by Peter in the Bank of America. However, as the amount in Peter’s savings account is $50 only, and the check amount is $75, the bank did not process it, and the check was returned. This non-processing of the check is due to insufficient funds in Peter’s account and is referred to as a check bouncing. Peter received a notice of bounced check and had to pay the applicable charges to the bank.

Impact

There is a negative impact:

- A bounced check hampers the payee’s credit score, and one can face difficulty getting a loan in the future.

- When the bouncing of checks continues for any customer repeatedly, the bank can restrict the issuance of the checkbook to that customer.

- If there is any loan active in the bank and the check for the repayment of EMI bounces, the bank has the right to issue a legal notice. It can also deduct money from the active bank account of the customer.

Penalty

When the check is dishonored, it may attract many penalties and bounced check charges under many acts. The bank may charge an overdraft fee for this purpose. Repeated bounce may result in other actions like the bank may close or freezing the bank account.

According to the legal provisions, bouncing the check is a criminal offense. Thus, there might be bounced check legal action. Furthermore, it can result in imprisonment, a monetary penalty, or both. Also, credit score gets negatively impacted due to which one can face many difficulties in acquiring a loan.

How To Avoid?

Before issuing any check, the issuer must ensure that they have a sufficient amount in their bank account. Also, they should properly go through various reasons that lead to the bouncing of checks and verify that they have correctly entered the inputs and the required information. And they should also handle the check properly as a damaged check leads to the bouncing of the check and the default by the payer.

Bounced Check Vs Stop Payment

In case of a bounced check, the bank dishonors it whereas in case of a stop payment, the payer wants to stop the check payment. Let us look at the difference between them.

| Bounced Check | Stop Payment |

|---|---|

| The bank is unable to make the payment to the payee. | The payer instructs the bank to stop the check payment |

| It has a legal and financial consequences. | The bank charges a fee for the procedure. |

| The reason is a lack of funds in the payer’s account. | Reasons might be forged checks, lost or stolen checks, lack of funds, etc. |

| It happens after the bank tries to process the check. | It can be implemented only if the processing has not yet been done. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1. What is a demand letter for the bounced check?

A demand letter for a bounced check is a written notice sent to the issuer of a bounced check requesting payment of the outstanding amount along with any additional fees or penalties.

2. Is a chargeback a bounced check?

A chargeback is not the same as a bounced check. A chargeback occurs when a consumer disputes a charge on their credit card statement and requests a refund. A bounced check occurs when a check is presented for payment but is returned due to insufficient funds in the issuer’s account.

3. What is stop payment vs. bounced check?

Stop payment and bounced checks are related but different concepts. Stop payment is a service banks offer their customers to stop payment on a check that has not yet been processed. A bounced check occurs when a check is presented for payment but is returned due to insufficient funds in the issuer’s account.

Recommended Articles

This article is a guide to what is a Bounced Check. We explain its penalty, with an example, vs stop payment, along with reasons, impact, and ways to avoid it. You may learn more about financing from the following articles: –

Recommended Articles

Continue with these closely related articles from the same guide.