Part of our Banking Services and Operations guide

What Is An Agent Bank?

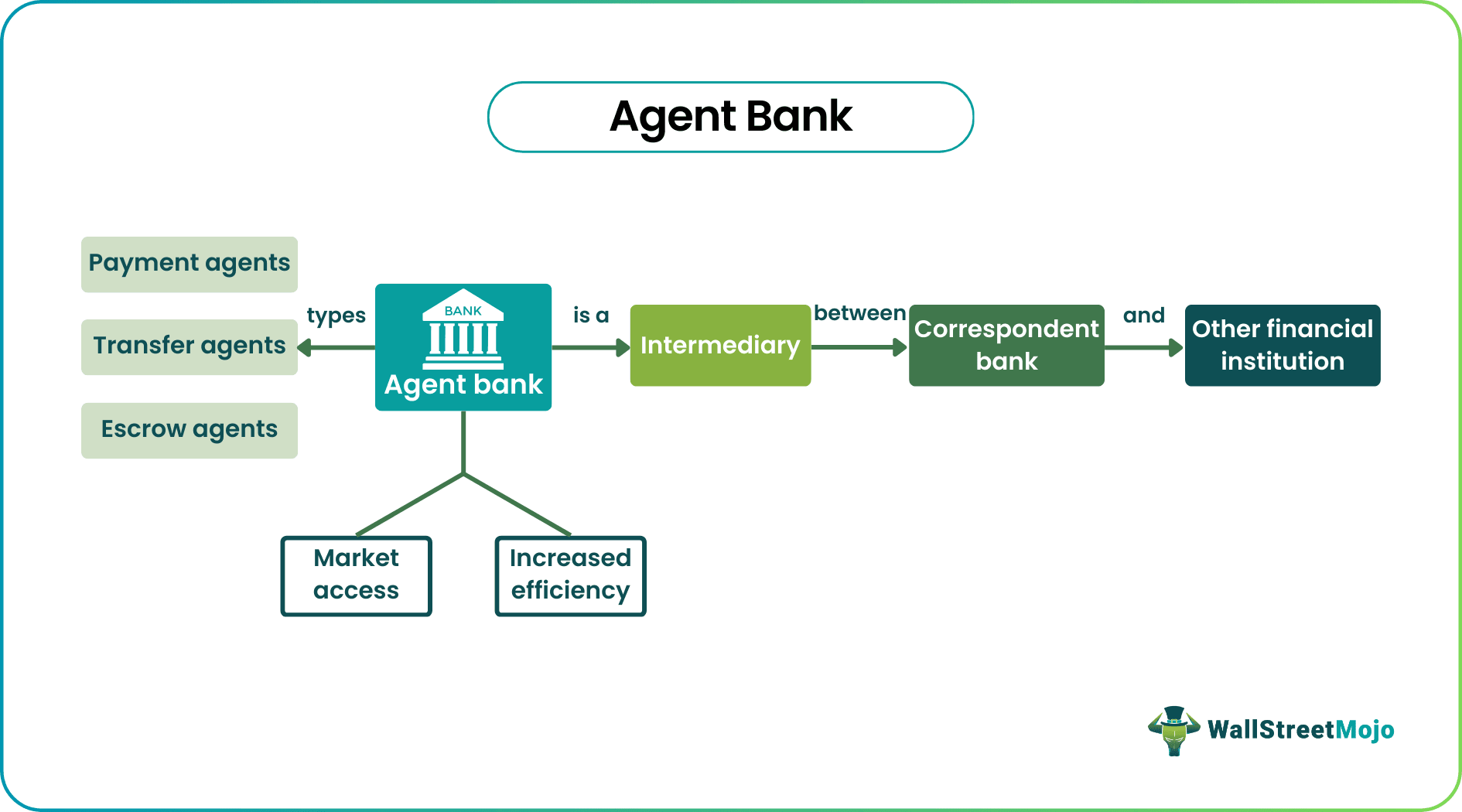

An agent bank is a financial institution that acts on behalf of other banks, typically in a correspondent banking relationship. In this role, the agent bank purpose is to provide various services to the correspondent bank, such as facilitating wire transfers, processing payments, and providing account management services.

The importance of agent banks lies in their ability to provide vital financial services to other banks, particularly when the correspondent bank does not have a physical presence or expertise in a particular country or region. In addition, by leveraging the agent bank’s network and knowledge, the correspondent bank can expand its reach and provide its clients with access to new markets and financial products.

- Agent banks are financial institutions that provide services to other banks or their clients, such as payment processing, custodial services, and fund administration.

- There are different types of agent banks, including correspondent banks, paying agents, transfer agents, escrow agents, securities services agents, syndication agents, and trustee agents.

- Benefits of using an agent bank include access to expertise, increased efficiency, risk management, market access, and customization. However, there are potential disadvantages, such as loss of control, additional costs, reputation risk, communication challenges, and lack of flexibility.

- Before entering into a relationship with an agent bank, it is important for banks to carefully evaluate their specific needs and the risks and benefits associated with using an agent bank to determine if it is the right choice for their business.

How Does An Agent Bank Work?

An agent bank intermediates between a correspondent bank and other financial institutions or clients. The correspondent bank relies on the agent bank to perform various financial services on its behalf, including processing payments and managing accounts. In addition, the agent bank is responsible for ensuring that all transactions comply with the correspondent bank’s policies and procedures and applicable laws and regulations.

To work effectively, the agent and correspondent banks typically enter a formal agreement outlining the scope of services, each party’s responsibilities, and the compensation terms. The bank may also be required to maintain certain capitalization levels and meet other regulatory requirements to operate in its jurisdiction.

The agent bank’s role may vary depending on the specific services required by the correspondent bank. For example, in a wire transfer transaction, the agent bank may facilitate funds transfer between the correspondent bank and the receiving bank. In other cases, the agent bank may provide account management services, such as monitoring account activity and reporting on balances and transactions.

Types

There are different agent banks, each serving a specific purpose or providing a particular set of services. However, here are some common types of agent banks:

- Correspondent Bank: This bank is often used in international banking. A correspondent bank in one country engages an agent bank in another country to provide financial services to its clients.

- Paying Bank: This bank is responsible for distributing interest and principal payments to bondholders on behalf of the issuer.

- Transfer Agent Bank: A transfer agent bank maintains records of a company’s stock ownership and facilitates the transfer of shares between shareholders.

- Escrow Bank: This bank holds funds or assets in a secure account on behalf of two or more parties as part of a contractual agreement.

- Securities Services Agent Bank: It provides various securities-related services, including custody, clearing and settlement, and corporate actions.

- Syndication Bank: This bank leads a group of lenders in a syndicated loan, coordinating the loan process and managing the administrative aspects of the loan.

- Trustee Bank: It acts as a fiduciary for the beneficiaries of a trust, managing the trust’s assets and ensuring that the trust’s terms are carried out according to its legal requirements.

Examples

Let us have a look at the examples to understand the concept better.

Example #1

As per the article by Finextra, agent banks can play a crucial role in modernizing the payments infrastructure. With their established networks and expertise, banks can provide innovative solutions and services to meet the market’s evolving needs. However, to fully realize the potential of banking, it is necessary to address certain challenges, such as regulatory barriers, technology limitations, and increased collaboration between banks and agents.

By working together and embracing new technologies, banks can help future-proof the payments infrastructure and drive innovation in the financial industry.

Example #2

Consider that Bank A, based in the United States, has a correspondent banking relationship with Bank B in Japan. Bank A wants to expand its business in Japan but does not have a physical presence or expertise in the country. In this case, Bank A may engage an agent bank, Bank C, as its intermediary in Japan.

Bank C has an established network and expertise in Japan and can provide Bank A with various services, such as processing payments, managing accounts, and providing local market intelligence. Bank A and Bank C enter into a formal agreement that outlines the scope of services to be provided, the responsibilities of each party, and the terms of compensation.

As part of its services, Bank C may process payments on behalf of Bank A’s Japanese clients, using Bank B as its correspondent bank. In addition, Bank C would ensure that all transactions comply with Bank A’s policies and procedures and applicable laws and regulations in Japan. Bank C may also provide account management services, such as monitoring account activity and reporting on balances and transactions.

In this scenario, Bank C acts as an agent bank for Bank A, providing valuable financial services and expertise that enable Bank A to expand its business in Japan without establishing a physical presence there. In addition, Bank C plays a critical role in managing risk and ensuring all transactions are conducted safely and securely.

Benefits

Let us look at the benefits associated with using this bank:

- Access to Expertise: These banks typically have specialized knowledge and expertise in particular markets or financial services. Thus, by leveraging this expertise, banks can expand their reach and offer their clients new products and services.

- Increased Efficiency: Using them, banks can outsource certain functions, such as payment processing and account management, which can increase efficiency and reduce costs.

- Risk Management: It can play a critical role in risk management for their clients. For example, in a correspondent banking relationship, such banks are responsible for ensuring that all transactions comply with applicable laws and regulations, reducing the correspondent bank’s exposure to risk.

- Market Access: Such banks can provide banks with access to new markets and geographies, which can help them grow their business and diversify their revenue streams.

- Customization: It can often provide customized solutions to meet the unique needs of its clients. Thus, it can help banks differentiate themselves from their competitors and provide a better experience for their clients.

Disadvantages

Let us look at some potential disadvantages:

- Loss of Control: When a bank uses an agent bank, it relinquishes some level of control over its operations. This bank will be responsible for carrying out certain functions on the bank’s behalf, which can make it more difficult for the bank to oversee these functions directly.

- Additional Costs: Using an agent bank typically involves additional costs, such as service fees. These costs can increase over time and may affect the bank’s profitability.

- Reputation Risk: Banks that use agent banks may be exposed to reputational risk if the agent bank does not meet the bank’s standards for rules, ethics, or customer service. If a bank engages in illegal or unethical behavior, it can reflect poorly on the bank that uses its services.

- Communication Challenges: When working with a bank in a different country or time zone, communication challenges may slow the process or create misunderstandings.

- Lack of Flexibility: These banks may have processes and procedures that may not be flexible enough to accommodate the unique needs of a particular bank or client.

Frequently Asked Questions (FAQs)

1.Where to cash in a landbank agent bank card?

Landbank cardholders can cash in or deposit money at any authorized landbank partner or branch. These partners can include rural banks, cooperatives, or other authorized financial institutions.

2.What are the challenges of agent banks?

Some of the challenges of such banking include lack of access to technology and infrastructure, low levels of financial literacy among customers, inadequate regulation and supervision, and high operational costs.

3.How much agent bank charge?

Bank charges can vary depending on the specific services being provided, the location of the bank, and the terms of the agreement between the bank and its clients. Therefore, it is important to carefully review any fees or charges before selecting a bank.

Recommended Articles

This has been a guide to what is Agent Bank. Here, we explain the topic in detail, including its types, examples, benefits, and disadvantages.You can learn more about it from the following articles –