Part of our Banking Services and Operations guide

Cosigner Meaning

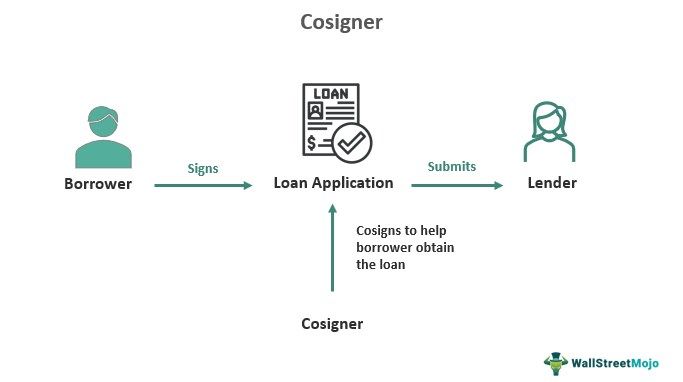

A cosigner is a person who signs the loan application and assumes full responsibility for loan repayment along with the original borrower. Often family members with good credit scores cosign a loan. They are only responsible for loan payments if the principal borrower defaults. They help borrowers get loans easily for big items, like a car or a house.

Cosigning increases the chance of the acceptability of the loan application. In other words, the chance of loan approval and getting better loan terms increases with the presence of a cosigner. Cosigning entity is responsible for repayment, and defaulting can affect the borrower’s and cosigning entity’s credit scores. The cosigner’s credit can be affected even when the borrower is late with payments.

- A cosigner is a person who signs the loan application together with the principal borrower and assumes full responsibility for loan repayment. Often an individual with a good credit score cosigns a loan.

- They are only responsible for loan payments if the principal borrower defaults.

- It helps the borrower to get easy access to loans and better loan terms and gives the loan lender additional assurance that the loan will be repaid promptly.

- Any loan can be availed through cosigning, be it student loans, credit card agreements, vehicle loans, personal loans, and home improvement loans.

How Does A Cosigner Work?

Cosigner pledges to repay the loan if the borrower cannot do so. They assist the applicant, typically someone with bad credit or no credit, to become eligible for a loan. The borrower might not be eligible for various reasons, such as having a high debt-to-income (DTI) ratio, not having a stable income, or being too young to develop a credit history. For example, students with no job or salary do not have a credit history, and student loans without a consigning entity may be difficult to attain.

Lenders often place more weight on the consigning person’s score during application. In cosigning a loan, individuals consent to guarantee another person’s debt. However, the property for which the loan is being used does not become theirs, and they do not acquire any ownership rights, title, or other rights. Cosigners are only liable for monthly payments if the principal borrower defaults and does not hold any ownership stake in the assets purchased with the loan. Any loan can be availed through cosigning, be it student loans, credit card agreements, vehicle loans, personal loans, home improvement loans, and other loans.

If the principal borrower is late on payments or defaults, the cosigner solely needs to repay the loan. Therefore, lenders prefer to work with consigners with excellent credit scores, a clear credit history, and a track record of timely payments. In addition, if an individual signs a loan as a cosigning entity, they formally acknowledge that if the principal borrower defaults, they will take on the financial responsibility of making payments.

Requirements

A loan with a cosigner requires different documents and may vary, especially with the lender chosen. For example, a personal loan with a cosigner requires checking the credit score of the individual who agreed to cosign the loan. The process is made easier if the right lender is found. At the same time, many documents need to be submitted during the whole process.

A personal loan with a cosigner requires the following to be submitted:

- Driver’s licenses or other identification documents of both parties (consigner and the actual borrower);

- Personal identifying information to employment, income, and debt information;

- Social Security numbers of both parties;

- Bank statements of both parties;

- Paystubs of both parties;

- Form W-2.

Pros And Cons

In the following section, let us look into the pros and cons of a cosigner to understand the concept better.

Pros

- Loans with a cosigner can help people with low or zero credit scores.

- Signing might be advantageous for both the lender and the borrower; it can improve relationship ties.

- Having a different person to sign and support the loan assures the lender that the loan will be paid back.

- It may also enable the borrower to obtain a lower interest rate.

Cons

- If the borrower defaults, the cosigner will be held liable for the full amount of the loan, and their contact information will be given to a debt collector.

- A debt collector may take legal action against a cosigner to recover the debt.

- There will be negative effects of poor payment history on credit scores. The co-credit signer’s score will suffer even in the absence of default because of the principal borrower’s late payments.

- The debt-to-income (DTI) ratio rises. There is a corresponding rise in outstanding debt when a cosigner is added to a loan. As a result, the ability to qualify for loans may be hampered by a high DTI.

- Removing oneself as a cosigner might be challenging.

- To ensure that the borrower is paying timely and full payments, the cosigner may have to keep an eye on their credit report.

Cosigner vs Guarantor vs Co-Borrower vs Co-Applicant

Let us look at the difference between a cosigner, guarantor, co-borrower and co-applicant in the following section –

| Basis | Cosigner | Guarantor | Co-applicant | Co-Borrower |

|---|---|---|---|---|

| Interest rates : | The entity that signs together with a borrower to aid in the loan approval or to obtain better loan terms. | A person who guarantees the repayment of a borrower’s debt if the borrower cannot make loan repayments is known as a guarantor. Guarantors put up their property as security for the loans. | A co-applicant works alongside a borrower during the loan underwriting and approval process. In some circumstances, a co-applicant may be considered second to a major applicant. | The co-borrower has access to the loan funds and shares and is responsible for repayment. Furthermore, they also share the title to the property. |

| Payment responsibility: | Yes, liable to payment on failure from the borrower. | Liable to payment on failure from the borrower. | Yes, liable to payment on failure from the borrower. | Liable to payment on failure from the borrower. |

| Ownership: | They do not necessarily own the property. | They do not have ownership of the property. | They cannot own the assets. | Co-borrowers on a mortgage have the same legal right to the property as the principal borrower. |

Frequently Asked Questions (FAQs)

Frequently Asked Questions

What happens if you are a cosigner?

<p>When a borrower defaults, an individual is legally required to pay back a debt in full if he has cosigned it. Serving as a good reference for another person is not required to cosign a loan. The cosigning entity verifies the ability to repay the debt when he cosigns. It implies that the cosigning entity runs the danger of being instantly liable for any missing payments.</p>

Is a cosigner a legal owner?

<p>Along with the borrower, a cosigner signs for the loan to purchase the property. They are not, however, included on the property’s title. Although the cosigner is legally obligated to repay the loan in case of default, they do not own the property; instead, they provide an additional security element.</p>

What’s the difference between a signer and a cosigner?

<p>The applicant, or borrower, for the loan, who will be the property owner brought using the loan, is the signer. An additional party that agrees to assume financial liability for loan repayment if the signer defaults are known as a co-signer.</p>

Recommended Articles

This has been a guide to Cosigner and its meaning. We explain its comparison with the guarantor, co-applicant & co-borrower, requirements, and pros & cons. You can learn more about finance from the following articles –