What Is Retail Banking?

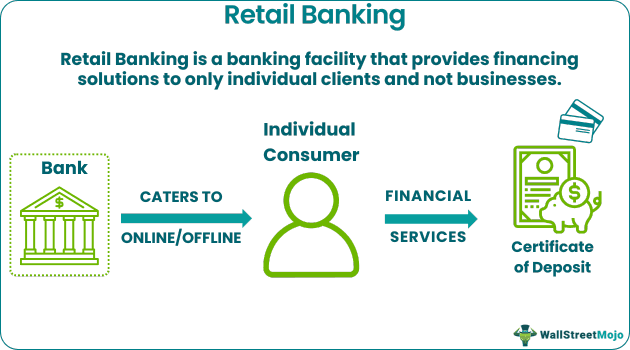

Retail banking is a banking facility that offers financial services to the general population rather than companies. It certainly helps retail customers conduct their daily financial dealings more effectively and safely. Also labeled as “consumer banking,” it occurs between consumers and their banks.

Retail banking services are provided both on online portals and offline branches. Moreover, it incorporates savings and checking account, credit cards, consumer loans, debit cards, internet banking services, and mortgages. Simply put, it is a consumer-oriented banking approach.

- Retail banking is a banking service that directly handles individual consumers, not enterprises. Moreover, retail banking jobs entail the provision of customer-centered solutions.

- There are 3 types of retail banks – small, large, and online. Moreover, they collect funds through service charges, overdraft charges, monthly maintenance fees, and modest fees.

- Its products comprise checking and savings accounts, credit and debit cards, personal and home loans, and also, certificates of deposit.

- Consumer banking (catering to individual consumers) differs from commercial banking (catering businesses) regarding the target audience, products, and transactional volume and value.

Investors seeking a comprehensive platform may consider Saxo Bank International for a variety of account types and investment options.

Retail Banking Explained

Retail banking assists consumers in directly connecting with the bank to manage their everyday requirements, for example, personal loans and mortgages. Moreover, they must approach the bank portal or branch to examine its menu of retail banking services. It helps customers certainly get the desired services at the concerned portal or branch. In recent years, the growth of retail banking jobs has certainly attained a high level owing to the demand for digital banking services.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Also termed “personal banking,” it facilitates management of the money for individual consumers. Thus, the profile for retail banking jobs includes offering personal banking services and accounts, for example, product manager or customer advisor.

Retail banks also impose monthly maintenance costs and service charges to improve their bottom line. Additionally, they charge overdraft fees when consumers spend beyond available funds and levy modest fees to send wire transfers or print cashier’s checks.

For efficient cross-border payments, many individuals and businesses use the Wise Money Transfer UK or Wise Money Transfer US services for transparent and low-cost transfers.

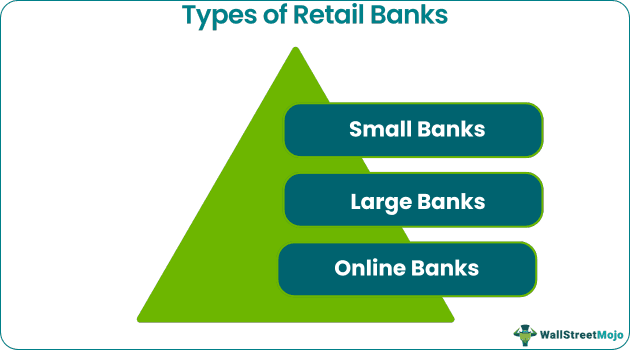

Types Of Retail Banks

So, there are 3 kinds of retail banks:

#1 – Small Banks

They function in a small range via branch banking with nearly all facilities offered by the large banks and hence are quite known among the populace. Nevertheless, they possess lower market shares and lesser deposits compared to them.

#2 – Large Banks

These prominent banks operate in big cities with numerous branches and certainly have more personnel than small banks. Also, several retail clients choose them because of their huge popularity.

#3 – Online Banks

As the name suggests, online banks work electronically with no tangible offices. Moreover, they operate through an official website accessible from even the remotest parts of the world. Now that a majority of people prefer to avail banking services from the comfort of their homes, it is a lucrative option for people with hectic schedules.

Retail Banking Products

Moreover, let’s go through the list of personal banking products:

#1 – Savings Accounts

Also known as “interest-bearing accounts“, it is a relevant retail banking example referring to basic deposit accounts to safeguard cash with a decent interest rate. They stash away the amount for short-term requirements and generally apply cash transferal and withdrawal limits.

#2 – Checking Accounts

These deposit accounts permit easily accessible (and usually unlimited) cash withdrawals and deposits for regular payments. Also known as “Transactional accounts,” they offer debit cards for purchases and online bill payments. Nonetheless, they render less interest than savings accounts.

#3 – Debit Cards

Also called ATM Cards, they are bank-issued payment cards for cashless transactions through money deduction directly from the checking account. Furthermore, they link straight to the bank account, and consumers can utilize them at Automated Teller Machines (ATMs).

#4 – Certificates Of Deposit (CDs)

This savings account holds a set capital amount for a predetermined duration and the issuing bank grants interest in exchange. When cashed in, consumers collect the actual amount and the interest amount.

#5 – Credit Cards

Credit cards are financial tools released by banks to borrow money for digital transactions with a fixed line of credit. Cardholders must repay the entire amount with any levied interest either until the payment date or with time to avoid credit risk.

#6 – Home Loans

They denote a capital amount consumers lent from banks or financial institutions to buy a home. Moreover, second mortgages infer the usage of home equity as collateral to borrow funds.

#7 – Personal Loans

These loans certainly entail money borrowed from banks, online lenders, or credit unions to meet financial obligations. Moreover, the multi-purpose unsecured loan is compensated in monthly payments within a few months or years.

Examples

Now that we know the concept, let’s discuss some relevant retail banking examples:

Example #1

Suppose Elena visits the nearby retail bank to deposit $5000 in her checking account. Moreover, one of the salespersons in the bank also briefs her about the latest investment scheme for retirement. Now, Elena is certainly impressed and decides to invest in the retirement plan next month.

She also enquires about the home loan services to buy a new house in another locality. Hence, personal banking helped her facilitate the cash deposit process, comprehend the new scheme, and acquire personal counseling.

Example #2

Due to consistent innovations, consumer banking has been expedited since the onset of the COVID-19 pandemic. In other words, it is experiencing a top-to-bottom evolution to benefit clients with an ever-lasting revolution. Coronavirus has undoubtedly been a blessing in disguise for consumer banking as it has forced financial markets toward adopting smooth banking experiences.

However, there is still a lot of friction to overcome from. For instance, 40% of banks offering online checking account services require applicants to finish a process more than 10-minutes long. Needlessly, real innovation is required for personal banking to originate from a digital bank establishment.

Retail Banking vs Commercial Banking

| Particulars | Retail Banking | Commercial Banking |

|---|---|---|

| Definition | Provides financial offerings to the general population. | Provides financial offerings to firms. |

Target clientele | Individual consumers | Businesses |

Focal point | Personal banking services and accounts | Serving enterprises |

| Products and services | Savings and checking accounts Personal and home loans Debit and credit cards Certificates of Deposit (CDs) | Merchant services Global trade services Treasury management services Lending services |

Transaction volume & value | High volume Modest value | Low volume Bigger value |

Product customization | Standardized products and services | Customized products and services |

Advantages | Increased earnings of small individuals and units Decreased operational charges Strong customer-bank relations Secured method to retain savings | Safeguarding public riches Simplification of business transactions and deposits Conversion of digital money Global trade expedition |

Want a smarter way to bank on the go? Revolut offers a user-friendly app with global access, crypto and stock trading, and innovative budgeting tools—all in one powerful platform.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What Does Retail Banking Mean?

Retail banking meaning certainly implies providing banking solutions to only individual clients and not enterprises. Therefore, it revolves around the customer to offer them secure financial services. Furthermore, this includes CDs, credit cards, and personal and home loans. Moreover, the most common retail banking example is debit cards.

Is Retail Banking a Good Career?

Yes, retail banking is deemed a good career in the 21st century. The onset of the Coronavirus pandemic has certainly accelerated the demand for digital-yet-personal banking services. It has also revolutionized the banking landscape. Therefore, several professionals choose retail banking jobs to provide customized monetary solutions.

What Are Retail Banking Products?

The retail banking products include checking accounts, credit cards, savings accounts, mortgages, debit cards, home equity loans, CDs, and personal loans. Moreover, consumer banking products are basic and standardized financial offerings to the general population. They also have high volume, fair value, and decreased market risk.

Recommended Articles

This has been a guide to retail banking and its meaning. Here we explain retail banking products, examples, & how it differs from commercial banking. You may also have a look at the following articles to learn more –