Part of our Balance Sheet guide

What Is A Revolving Credit Facilities?

A Revolving Credit Facility is one of the forms of business finance in which flexibility is provided to the companies to borrow and use the financial institution’s funds according to their cash flow needs by paying a commitment fee as agreed in the agreement with the financial institution.

Revolving Credit Facilities are pre-approved corporate loan facilities (just like credit cards) wherein corporations can avail of a loan without further documentation, and there are no fixed repayment schedules for the same.

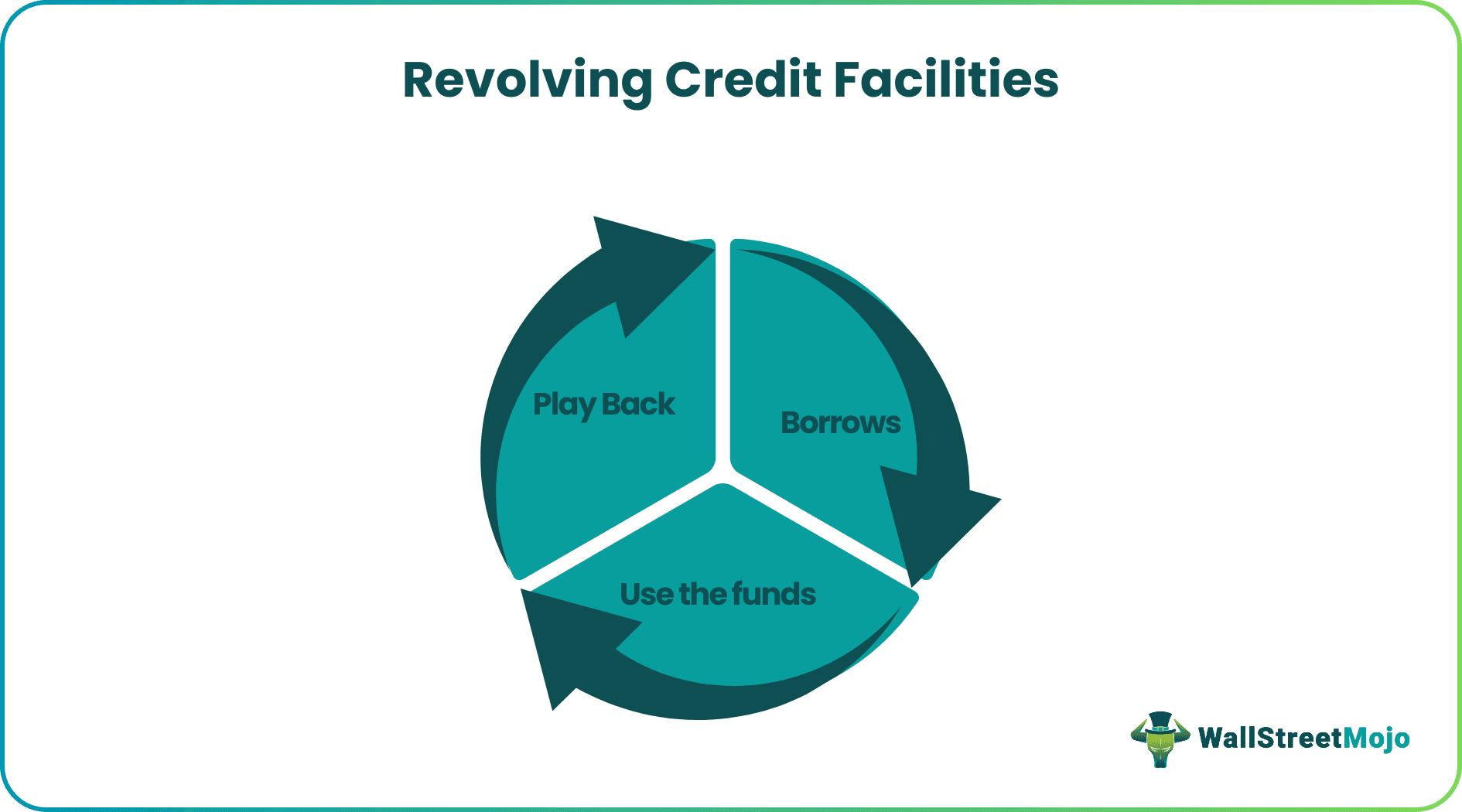

How Do Revolving Credit Facilities Work?

- BankThe bank will ask for a mortgage. Usually, for business owners, inventories or accounts receivables act as mortgages. The small business owner will talk to the bank about a credit facility.

- Bank hands the business owners a revolving account with the pre-approved limit. If the business owners want to use little, she can do so. On the rest of the amount, revolving credit facility interest rate is being charged by the bank. For example, if the pre-approved limit is $30,000 and the small business owner only needs around $3000, the bank will charge interest on the outstanding amount.

- There is no fixed monthly payment. The business owner can pay back the amount in 6 installments (the principal plus the interest) or in one go.

And if the business owner doesn’t take more credit facilities, she can pay back the amount whichever way she wants.

You may wonder what the bank does if the small business owner fails to pay off the amount.

The bank values the inventories or the accounts receivables at 80%. It then sells off the inventories or accounts receivables if the business owner fails to pay off the loan amount she has taken.

Video Explanation of Revolving Credit Facilities

How To Interpret?

Many US companies use such credit flexibility, and you will usually find that they report back on their balance sheet.

Let’s say a company has taken a revolving credit facility from a bank. Where would the company report its revolving credit in the financial statements?

To understand the revolving credit facility accounting treatment we should know that they would first set up their balance sheet. They will go to the debt section, and then usually, they will mention a note below the balance sheet where they will report what exactly happens in regards to a revolving line of credit.

Now, what if they don’t mention it?

Then it would be difficult for an investor to determine where the debt (the figure) came from. If the company has done the calculation but doesn’t show the calculation and the exact narration of how it happened under the balance sheet, it wouldn’t be possible for the investor to understand it.

The filing system under Sec filings ensures that the investors’ interest is secured. Not showing or mentioning a revolving line of credit will be treated as non-disclosure and will not help the investor.

In the example below, we will show you how you would be able to do revolving credit facility accounting treatment.

Example

Let us understand the concept of corporate revolving credit facility with the help of some suitable examples.

Example#1

| Particulars | 2016 (In US $) | 2015 (In US $) |

|---|---|---|

| Current Assets | 300,000 | 400,000 |

| Investments | 45,00,000 | 41,00,000 |

| Plant & Machinery | 13,00,000 | 16,00,000 |

| Intangible Assets | 15,000 | 10,000 |

| Total Assets | 61,15,000 | 61,10,000 |

| Liabilities | ||

| Current Liabilities | ||

| Short term debt including current maturities | 50,000 | 80,000 |

| Accounts Payable | 60,000 | 70,000 |

| Deferred Revenue | 30,000 | 45,000 |

| Accrued Expenses | 60,000 | 75,000 |

| Long term Liabilities | ||

| Long term debt* | 95,000 | 125,000 |

| Deferred Revenue | 20,000 | 15,000 |

| Total Liabilities | 3,15,000 | 4,10,000 |

| Stockholders’ Equity | Amount | Amount |

|---|---|---|

| Preferred Stock | 550,000 | 550,000 |

| Common Stock | 50,00,000 | 50,00,000 |

| Retained Earnings | 250,000 | 150,000 |

| Total Stockholders’ Equity | 58,00,000 | 57,00,000 |

| Total liabilities & Stockholders’ Equity | 61,15,000 | 61,10,000 |

This is the balance sheet we have. You can see an asterisk on Long term debt. Now we will see how to represent the revolving credit facility.

Let’s look at the note.

| Particulars | 2016 (in US $) | 2015 (In US $) |

|---|---|---|

| Notes due in 2020 | 120,000 | 140,000 |

| Revolving Credit Facility | 25,000 | 20,000 |

| 145,000 | 160,000 | |

| (-) Short-term debt including credit facility | (50,000) | (80,000) |

| Long-term debt | 95,000 | 80,000 |

In 2015, ABC Company took a revolving credit facility of US $50,000 from RVS Commercial Bank. They wanted to expand upon their operations by buying a new machine for their production house. So, in 2015, they took the US $20,000 payable within three months of borrowing. That’s the reason it was treated under short-term debt. In 2016, they also took a revolving credit of US $25,000 from the same bank, and the payment was due within 90 days of borrowing. So, in this case, the corporate revolving credit facility was also included in the short-term debt.

In reality, it is much more complex (as seen in the practical examples).

Example#2

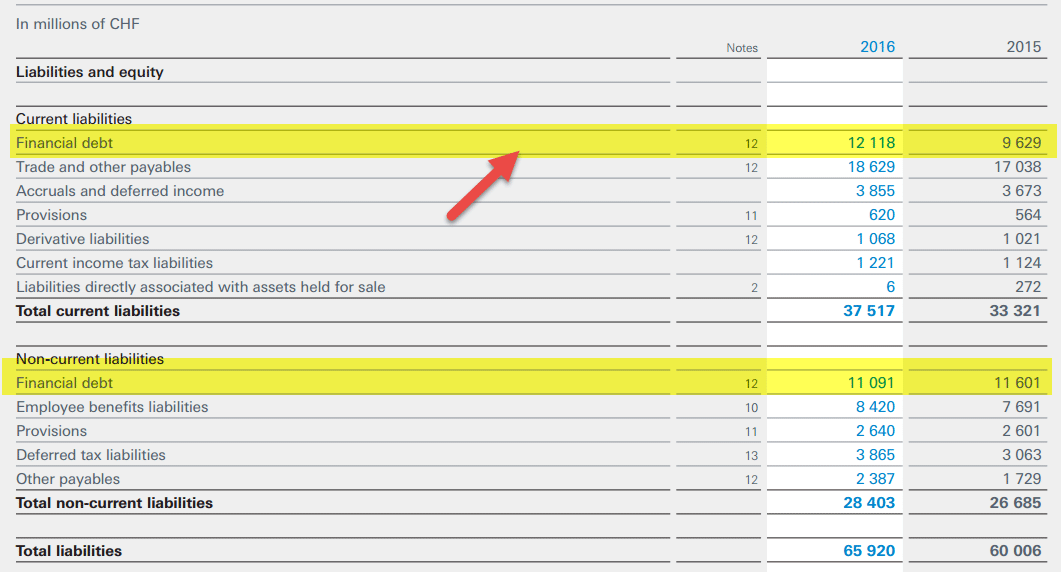

A consolidated balance sheet as of 31st December 2016 & 2015

Source – Nestle Annual Report

The above balance sheet depicts the long-term and short-term debt of Nestle in the years 2015 and 2016.

Let’s look at how they report revolving credit facilities under “notes” in their annual report. They have mentioned it under Liquidity Risk Management.

They have mentioned that they didn’t expect any refinancing issues, and they have two revolving credits. In 2016, they would have extended both of their revolving credits by one year. Along with that, the key factors of the note are –

- Firstly, they mentioned two new revolving credits (of the US $4.1 billion and EUR 2.3 billion) with an initial maturity date of October 2017. It has also been mentioned that the group has the ability to convert (if at all) into a one-year term loan.

- They also mentioned the existing facilities and their extended maturity date. The new maturity date of these revolving credit facilities (one of US $3.0 billion and another of EUR 1.8 billion) had been mentioned as October 2021.

- Thirdly, they had also remarked that these facilities should be treated as a backstop to their short-term debt.

Example#3

A consolidated balance sheet of Wal-Mart as of 31st January 2017 & 2016

source: WalMart 10K Report

Now, we will see how they have represented the revolving credit facilities. The above balance sheet of Wal-Mart has portrayed the short-term borrowings and long-term debts.

Their annual report had a note regarding short-term borrowings and long-term debts. Under that note, they have talked about their credit facilities.

First of all, they had mentioned their short-term borrowings, which are depicted in the following representation –

source: WalMart 10K Report

Wal-Mart had been committed with 23 institutions, combining them to the US $15 billion as of 31st January 2017 and 2016. Let’s have a glimpse of that in the table below –

source: WalMart 10K Report

They had also mentioned in the note that they had extended both a five-year credit facility and a 364-day revolving credit facility in June 2016.

Revolving Credit Facilities Vs Credit Cards

It may seem like a credit card for small business owners, but it’s not. There are many differences. Let’s have a look at them one by one –

- In the case of a credit card, the person needs to carry it. But in the case of revolving credit facilities, the person doesn’t need to carry any card.

- While using a credit card, the individual needs to make a purchase. But in the case of revolving credit facilities, the person doesn’t need to make any transaction. She can get the money directly into her business account for whatever reason she needs it.

- The fees charged for a credit card are often much more than those charged for the revolving credit facilities.

- Flexibility in terms of credit is much more in revolving credit facilities than a credit card.

Revolving Credit Facilities Vs Term Loans

→ Explore all 83 Loans articles

The above are two different forms of credit facilities that are widely used in the financial market. How ever, it is important to understand the differences between them, which are as follows:

- The former is a flexible form of credit given by revolving credit facility lenders but the latter is a fixed amount of credit given by institutions.

- The main purpose of the former is to meet requirements for short term funds, manage cash flow, inventory, etc. but the latter mainly required to meet long term needs like growth, expansion, investment on projects, etc.

- The revolving credit facility lenders of the former does not give any fixed term and they are open-ended, whereas the latter is given for a fixed term that is specified in the contract and the borrower has to meet the deadline of repayment, failing which will result in penalty.

- The revolving credit facility interest rate varies for the former depending on the benchmark rates followed by the market, whereas the rates for the latter may be fixed or variable.

- For the former, there may be a need for collateral in the form of accounts receivable or inventory of the business, but for the latter, collateral should be in the form of fixed assets like plant and machinery, property, etc.

Thus, the above are some important differences between the two kinds of credit facility. But both are equally important in the financial market because they provide funds to the business either for short or long term. The choice will depend on what is the requirement of the company.

Recommended Articles

Guide to what is Revolving Credit Facilities. We explain its differences with term loans along with examples & how to interpret it.

In the final analysis

The revolving credit facility is a boon for many small business owners. Even giant companies are also taking advantage of this thing.

As an investor, if you want to know where the company has reported its revolving credit facility, look at its annual report and find notes regarding risk management, a credit agreement, or short-term or long-term borrowings.