Part of our Balance Sheet guide

What Are Loan Loss Provisions?

Loan loss provisions are the portion of the loan repayments set aside by banks to cover the portions of the loss on defaulted loan payments. It helps the bank balance the income and survive during bad times and is recorded in the income statement as a non-cash expense.

It can manage the earnings by creating large provisions in case of high returns and small provisions during low returns. The bank can withstand the changing economic conditions by providing ample provisions to cover the losses and expenses

Loan Loss Provisions Explained

Loan loss provision ratio is the amount set aside to meet the expected credit loss. It is a systematic way used by the banks to cover the risk. The calculation of provision is based on estimations and calculations.

The information about loan loss reserves and provisions is useful for investors as it provides insights into the bank’s stability in lending and how the bank manages the credit. The bank can also decide the amount of provision that needs to be set aside based on the income

Lending and borrowing are the main businesses of the banking industry. They borrow money from customers, called deposits, and lend these to needy people. Interest out of these lending is the main source of revenue for the banks. According to the conservatism principle, for a business, all losses should be accounted for, whether it is materialized or not. So the banks anticipate loan default payments and provide a portion of loan repayments to balance the loss of default payments.

How To Calculate?

Many factors affect the calculation of loan loss provision ratio. The provision needs to be adjusted frequently as per the available estimates and calculations on customer loan repayment reports.

- Historical Data on Repayments and Default: The bank has to refer to and collect the record of customers’ defaults and repayments of loans.

- Loan Collection Expenses: Loan collection expenses affect the calculation of provisions.

- Credit Losses: The credit loss for late payments.

- Economic Conditions: The prevailing economic recession affects the calculations.

- Business Cycle: The movement of GDP is also a factor.

- Interest Rate: The change in interest rate influence its calculation.

- Tax Policy: The changes in the tax rate.

The process of loan loss provisions accounting is very important for banks and any other financial institution we are engaged in the business of lending out money to individuals or corporates. The above steps are to be kept in mind for such institutions so that they can function successfully.

Example

Let us try to identify the concept of loan loss provisions accounting with the help of a suitable example as elaborated below:

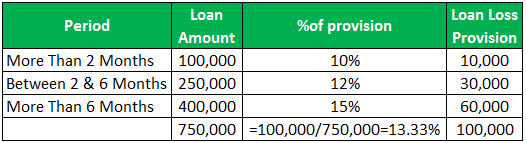

- Loan unpaid more than 2 months=100000, provision 10%

- Loan unpaid between 2and 6 months =250000, provision 12%

- If, Loan unpaid more than 6 months =400000, provision 15%

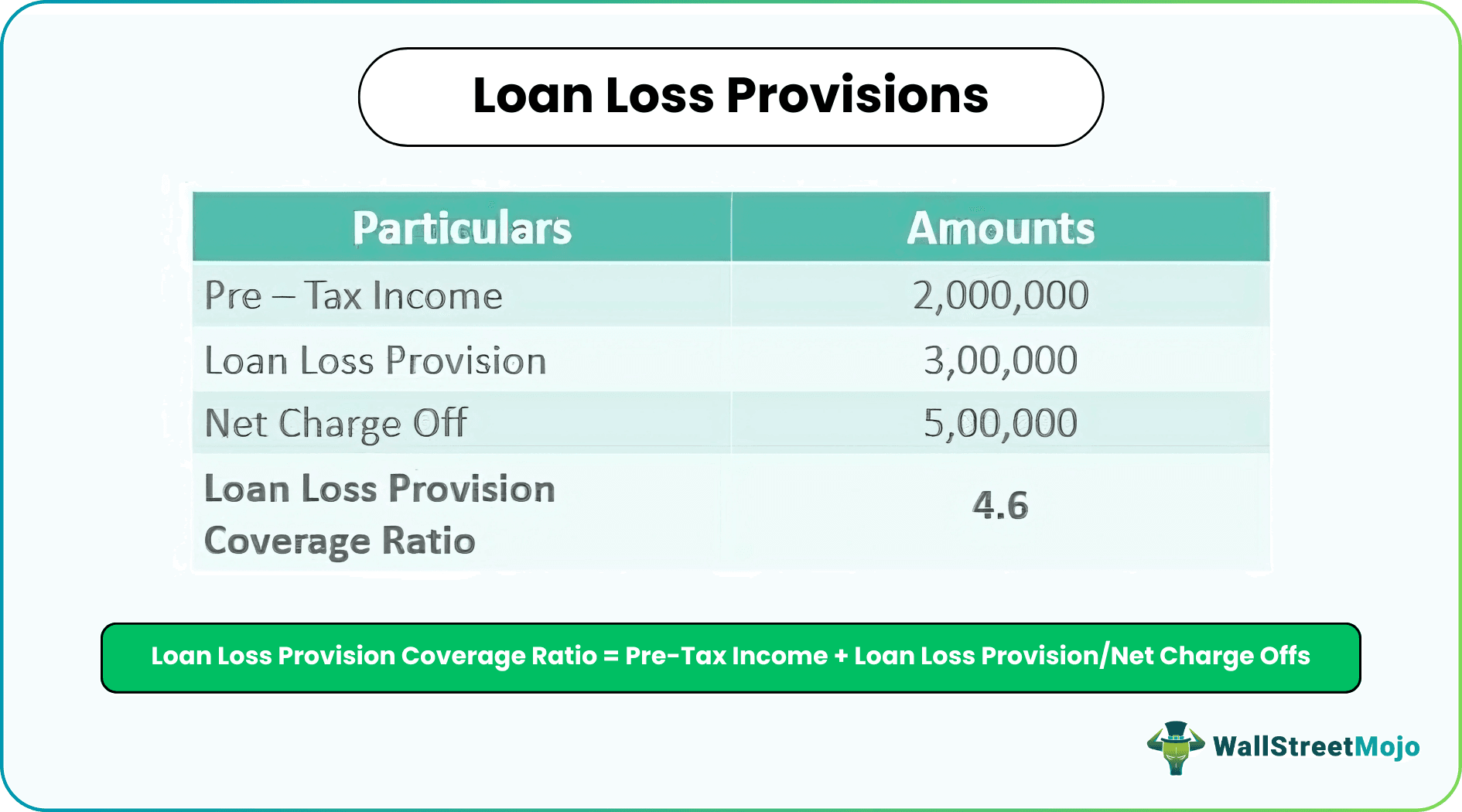

This Ratio of loan loss provision expense is a ratio that indicates the capacity of the bank to bear the loss on loans. A higher rate means a greater ability for the banks to face loan losses.

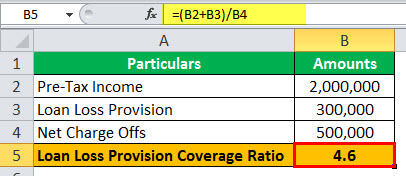

Loan Loss Provision Coverage Ratio = Pre-Tax Income + Loan Loss Provision / Net Charge Offs

Net charges = Actual Losses

- Suppose a bank provides Rs. 1,000,000 loan to a construction company to purchase machinery. After one year, due to the recession in the economy, the company is not able to make full repayment of the loan. The bank expects 70% of the repayment, and it records a provision of Rs.300,000.

- But the bank can collect only Rs.500,000 from the company, and the net charge off is Rs.500,000. Suppose the bank’s recorded pre-tax income is Rs.2,000,000

- =2,000,000 + 300,000 / 500,000

- = 4.6

Loan Loss Provisions Vs Loan Loss Reserves

The above are two different concepts that refer to fund set aside to meet the loan default amount. However, there are some important points of differences between them. Let us try to identify them as given below:

- At the time of the loan issue, the bank estimates a loan loss reserve to cover the default, which is shown in the asset side of the balance sheet deducted from total loans. It is a contra asset, which reduces the amount of loan that needs to be paid back. If the bank thinks it needs to raise the reserve due to some factors, the bank charges an amount from its current earnings to increase the loan loss reserve. It is the loan loss provisions.

- Loan loss reserve is shown on the asset side of the balance sheet as a contra asset account, deducted from the loan. Whereas, Loan loss provision is recorded as a non-cash expense in the income statement.

- Loan loss provision expense is an adjustment to loan loss reserve.

- The loan loss reserve is an appropriation of profit. Bank loan loss provisions is a charge against profit.

- The loan loss reserve is created at the time of providing a loan. Whereas, Loan loss provision is charged if there is a need for an increased reserve.

- Loan loss reserve refers to withholding the amount. The loan loss provision is the amount set aside to meet the default loan payments

Impact

These are expected losses of the bank due to credit risk, charged against the profits, recorded as an expense in the income statement. Bank loan loss provisions affects the regulatory capital of the bank through a profit and loss account.

It is important to understand the fact that this provision can be influenced by changes in the rules and regulation related to the guidelines followed by banks. The accounting standards may be specific to that particular region or jurisdiction. Thus these financial institution needs to remain updated regarding these rules and update their provisions so that they reflect the latest economic and market changes.

Recommended Articles

This has been a guide to what are Loan Loss Provisions. We explain them with example, how to calculate them, differences with loan loss reserves & impact. You can learn more about it from the following articles –