Part of our Balance Sheet guide

Short Term Loan Definition

Short-term loans are defined as borrowings undertaken for a short period to meet immediate monetary requirements. For example, companies often borrow short-term loans using bank overdrafts to arrange money for working capital requirements.

The loan tenure varies based on the debt type. For example, many loans mature in 6-12 months, while others come with a tenure of 1-2 years. The interest rate on inter-bank overnight loans is an essential tool with which central banks control inflation or deflation.

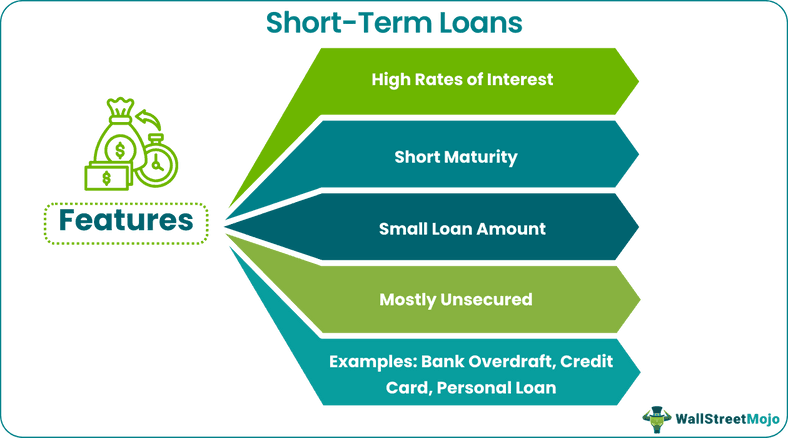

- A short-term loan is a credit facility extended to individuals and entities to finance a shortage of cash. Examples include credit card, bank overdraft, trade credit, payday loans, etc.

- The loan tenure varies based on the debt type. Many loans mature in 6-12 months while others come with a tenure of 1-2 years.

- The annual percentage rates (APRs) or the interest rates are normally set high. Short tenure restricts lenders from making adequate profits which is why they try to compensate it with higher interests.

- Most short-term loans are unsecured as there is no property that can be sold off for recovery if the debtor defaults. As such, loan applicants with a good credit score are preferred.

- Low credit score applicants often have to struggle quite a bit to secure a short-term loan. They are often extended loans at very high interest rates.

How Does A Short-Term Loan Work?

A short-term loan works as a rescue when people need some money urgently. For example, a business cannot finance its daily orders if all its debtors are delaying payments. Banks, credit unions and financial institutions provide many short-term lending facilities to businesses to cover their everyday costs.

These loans come in different shapes and sizes. One can get a short-term loan from banks, financial institutions, and suppliers. Borrowers can apply for short-term loans online or by visiting a branch. The lender checks the loan applicant’s creditworthiness, discusses the terms, fulfills paperwork and releases the money once approved.

Features of Short Term Loan

- The annual percentage rate (APR) or the interest rates are normally set high as a short tenure restricts lenders from making adequate profits. Normally, the tenure is less than a year and in some cases 1-2 years, leading to less accrued interest. Lenders rake in higher earnings with long term debts as repayments usually last for many years, piling up the interest amount.

- Moreover, lenders charge a high interest rate to compensate for the possible default loss as these loans are mostly unsecured. An unsecured loan is not backed with any collateral and so there no property that can be sold off for recovery if the debtor defaults.

- Since many lenders are not asking for collateral, they require borrowers to have a good credit score to ensure their creditworthiness for timely repayments.

- Also, the borrowing amount is usually small as compared to other forms of loans.

- Both the principal as well as the interest need to be repaid in full within the term of the loan. Many have a weekly repayment schedule.

- Many borrowers prefer to get a loan from a direct lender that eliminates any intermediaries such as credit brokers. A delay on the part of the broker could delay an applicant’s loan. In addition, direct lending for short-term loans often come with online facilities, faster approval and loan sanction. As a result, Covid-19 saw heavy demand for direct lenders.

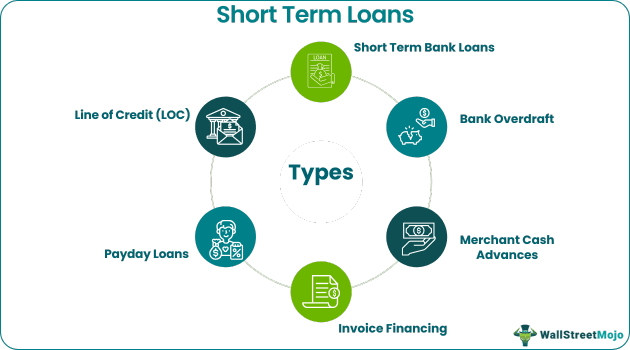

Types of Short-Term Loans

→ Explore all 83 Loans articles

Let us discuss some of the types in detail.

#1 – Line of Credit (LOC)

A line of credit is a kind of loan wherein a bank or financial institution sets a maximum loan amount that an individual is allowed to borrow. The borrower has the flexibility to withdraw the loan amount in a lump sum or instalments. Borrowers cannot withdraw beyond the permitted limit, which is determined based on their creditworthiness.

In return, the bank charges only on the withdrawn amount and not the remaining available balance of the loan. When it’s the time to pay the dues, the borrower will not be able to withdraw until the due principal and interests are paid. After paying the dues, the borrower can resume using the line of credit service. LOC works best when one requires a regular supply of credit.

#2 – Short-Term Bank Loans

Unlike a LOC, loans terminate at the end of a fixed tenure. Therefore, if the borrower wishes to borrow once again, they may have to apply for a fresh loan. An example is a personal loan to finance a wedding.

#3 – Bank Overdraft

A bank overdraft is one of the most common types of credit facility. Under this service, if bank account holders have insufficient money in their account than the amount they are trying to withdraw, the bank will provide the rest. In return, the bank charges interest with some setting exorbitant rates.

Businesses have innumerable transactions every day, leading to a fast-falling bank balance. A bank overdraft service avoids operational interruption due to rejected payments on account of a low balance. However, customers need to exercise caution when using bank overdrafts. Some reputed providers have charged unaccrued interests from their customers. Often, these banks have paid millions in fines for such illegalities.

#4 – Merchant Cash Advances

They are suited to businesses with large credit card/debit card sales instead of cash sales, i.e., their customers make card payments during purchases. Under this facility, a financial institution agrees to advance a lump sum amount to the borrower. The lender subsequently recovers this amount as a percentage of the borrower’s daily sales.

#5 – Invoice Financing (Receivables Financing)

Under this facility, a company borrows money from a bank or financial institution against the money due from its customers, i.e., account receivables. When customers take time to pay bills, a company can borrow in the meantime to meet its liquidity requirements. Lenders charge a fee for invoice financing, which they deduct from the lent sum. Receivables can be used as collateral, so if the borrower defaults, the bank can rely on them.

#6 – Payday Loans

With payday loans, the borrowing amount is determined based on the borrowers’ earnings, mostly as a specific percentage of their income. Repayment is to be made upon the receipt of the next paycheck/income. Payday loans come with unreasonably high interest rates and can be acquired either online or from stores.

Advantages

- Avenue for Small Loans: People don’t necessarily have to take a mortgage loan when they are in need of some immediate cash. A short-term credit facility allows people to arrange a small amount of money from financial institutions for needs such as medical emergency, or business expenses.

- Faster Approval: Short-term loan do not require lengthy approval processes as compared to other forms of loans.

- Lower Accrued Interest: As the repayment period is shorter, the amount of interest paid by the borrower is lower.

- Increases Credit Score: Availing such a loan and paying it off without any default can help increase the creditworthiness of the borrower.

- Unsecured: Such loans are usually unsecured, and borrowers do not require any collateral, making it easier to acquire funds at a short notice.

- Economic Well-Being: The interest rates on inter-bank overnight borrowings is an essential tool with which central banks control inflation or deflation. This is because an increase or decrease in short-term lending rates eventually affects the borrowing cost of kinds of all loans. When a central bank intends to increase growth, it lowers interest rates, increasing investment and consumption, leading to higher GDP, wages, and employment.

Disadvantages

- Lower Borrowing Amount: Sometimes, the borrower may require a larger amount which cannot be availed under short-term credit.

- Small-time Borrowers Plight: Several payday loans charge up to 400% interest in a year. High APRs make it difficult to manage repayments for those with humble means. Any interest rate hike or penalties may cause a further strain which may result in default and subsequent lower credit score.

- Unfair Means: Over the years, many payday and credit card lenders have made headlines for harassing their debtors. As per a 2020 study, over 3000 borrowers were issued an arrest warrant over payday loans, vehicle title, and other expensive lending.

- Credit Score: Due to unsecured nature of the loans, those with low credit score often struggle to acquire funds from reputed sources. With years many short-term loan providers have surfaced who provide loans to those with a bad credit score. They charge heavy interest rates to compensate for the lack of creditworthiness. With more expensive loans, the chances of default increase which can further damage the credit score.

FAQs

What is a short-term loan?

People don’t necessarily have to take a mortgage loan when they have an immediate need for some cash. A short-term loan allows people to arrange a small amount of money from financial institutions for needs such as medical emergencies or business expenses. The loan amount is small, and maturity is usually a year long.

What is an example of a short-term loan?

An example of a short-term loan is a bank’s overdraft facility. Under this scheme, if the borrower’s account holds insufficient funds to make a payment, the bank extends additional funds. In return, the bank charges the borrower for the service.

How can I get a loan for a short time?

There are many avenues to get a loan in a short time, one being many banks providing an online facility to apply for the loans. If approved, some personal loan providers can lend money within 24 hours. In addition, some institutions provide attractive rates to those with a high credit score.

Recommended Articles

This article has been a guide to what is Short Term Loans are and their definition. Here we discuss the Top 6 types of short-term loans, including Credit Line, Bank Over Draft, PayDay Loans, etc., along with examples, benefits, and disadvantages. You can learn more about accounting from the following articles –