Part of our Accounts Receivable guide

What is Notes Receivable?

Notes Receivable is a written promise that gives the entitlement to the lender or holder of notes to receive the principal amount and the specified interest rate from the borrower at a future date. They’re shown in the shareholder’s balance sheet as the current assets if the note is due within one year; else, they will be shown under the now-current head in the balance sheet if the note is due after one year.

If the notes receivable account is credited due to a sales transaction, the company will document it on its income statement. However, the document as such is a current asset if the principal is due to be received within one year of issuing the document. Therefore, it is recorded on the balance sheet.

Notes Receivable Explained

Notes receivable is the written promise which gives the rights to the holder of the note for receiving a specific sum of money at a specified future date. From the side of the maker of the notes, it is known as the notes payable as he must pay the specific sum of money at a specified future date to the holder of the notes receivable. The note provides all the terms and conditions clearly so that there should not be any ambiguity in the future between the two parties. It also clearly mentions the interest required to be paid along with the principal amount, which is the face value of the notes. So, it is an asset for the bank, company, or the other organization which holds it in the form of a written promissory note given by another party.

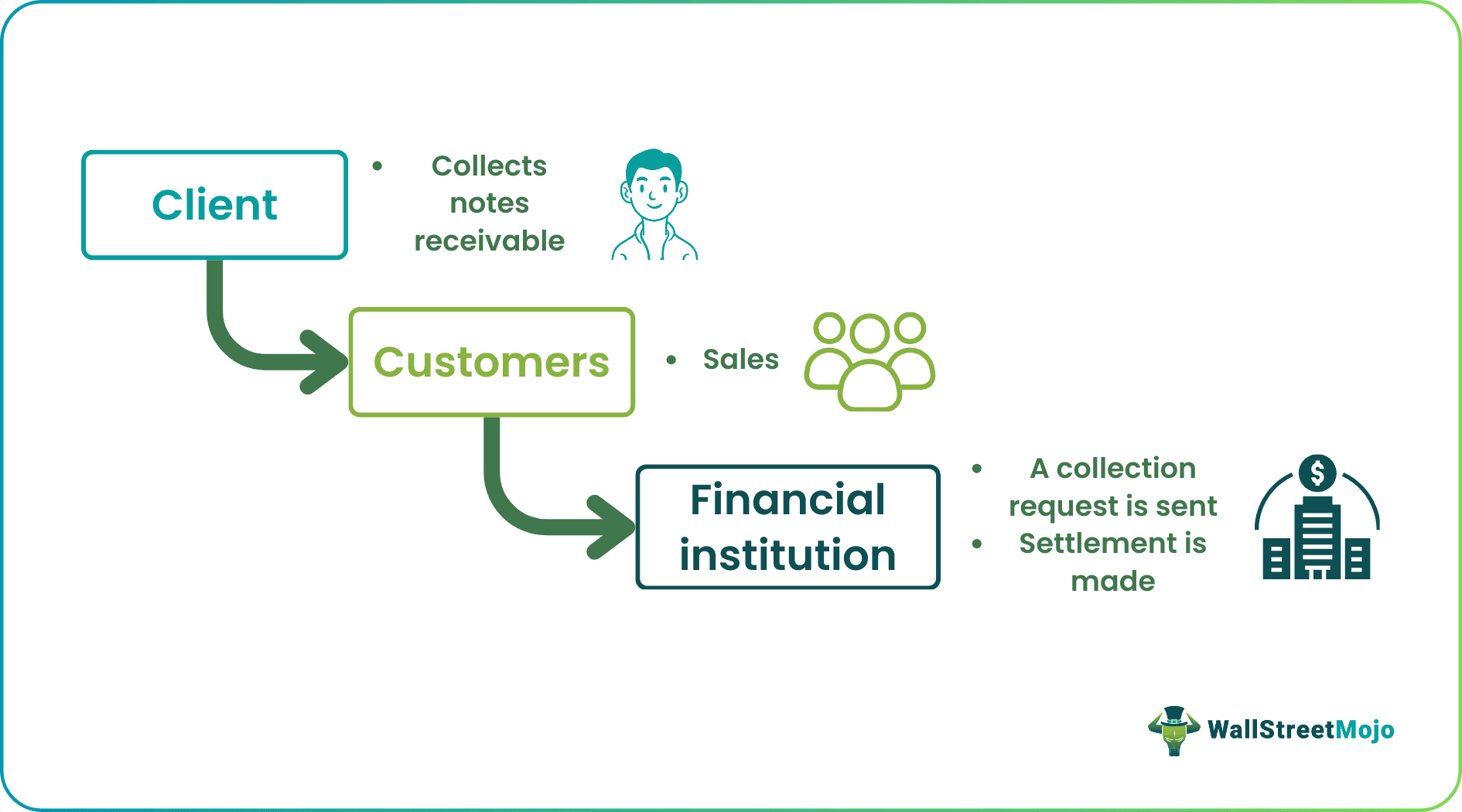

It is a common practice for businesses globally to purchase or sell on credit. When a supplier sells goods on credit, a formal promise to pay on a specified future date is issued. These formal or official forms of the promise are called promissory notes.

When a promissory note is accepted, it is accounted as a note receivable, which becomes a current asset if it is a short-term or a payment that shall be paid within one year.

Components

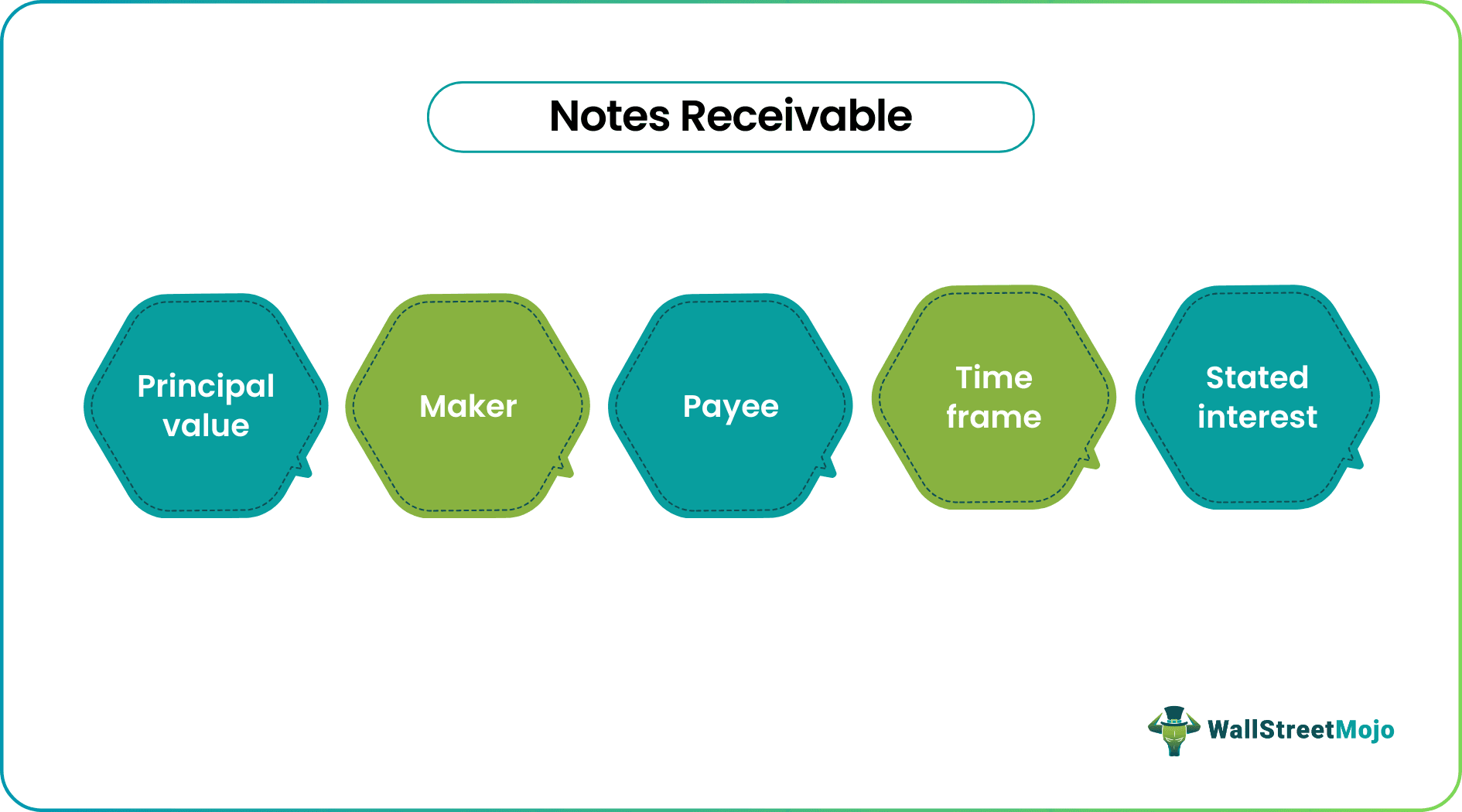

Notes receivable accounting is an elaborate process with different parties and terminologies involved. Let us understand the components through the discussion below.

- Principal Value: It is the note’s face value.

- Maker: The maker is the person who prepares the note. By preparing notes, the maker promises to pay the specified amount to the holder of notes. For the maker, the note will be classified as the note payable.

- Payee: The person to whom the maker issues the note is known as the payee. The payee holds the note with the right to receive the payment from the maker. For the maker, the note will be classified as the note receivable.

- Stated Interest: In addition to the principal amount, the note maker must pay the interest amount due at the interest rate, which is predetermined in the notes receivable. This predetermined interest rate is known as the stated interest.

- Time Frame: The length of time within which a note needs to be repaid is known as the time frame.

Examples

Let us understand the intricacies of how a notes receivable account is maintained and the details of the entries with the help of a couple of examples.

Example #1

X ltd. sold machinery to Y Ltd for $ 500,000 with the terms that payment against purchase will be made within 35 days from the date of sale. However, even after 35 days, Y ltd could not make the payment of the specified amount to the X ltd. Hence, with the consent of both of the parties, it was decided that X ltd will receive the notes receivable with a principal amount of $ 500,000 and a 10% interest rate to be issued by Y Ltd. It had a condition that $ 125,000 would be paid along with interest due at the end of each month for the next four months.

It will be treated as notes receivable in the balance sheet of X ltd. (payee) and will be treated as notes payable in the balance sheet of Y Ltd. (maker). The principal value of the note is $ 500,000, $125,000 of which will be paid monthly for four months (time frame) along with the agreed annual interest rate of 10% (stated interest).

Example #2

SEACOR Marine Capital Inc., specializes in a wide range of offshore marine vessels. In march 2023, in their financial declaration, they had mentioned a sale with a company called MexMar for $28.8 million in July 2022.

As on December 2022, the outstanding payments from MexMar was $15 million. In an agreement, MexMar became the borrower, DNB Capital LLC and another financial institution became the lenders and provided the funds to complete the payments through notes receivables.

Advantages & Disadvantages

Let us understand the advantages and disadvantages of a notes receivable account through the discussion below.

Advantages

- All the terms and conditions are in writing, so there will be no doubt about the borrower’s obligations after making notes. Also, it clearly outlines the rights of the lender.

- The borrower must sign the notes that protect the fraudulent alterations to the notes receivable.

- The notes avoid the risk of default for the business as they have everything mentioned.

Disadvantages

- Suppose the borrower cannot pay the specified amount even after the due date. In that case, he is liable to pay the principal and interest for the whole period, and the same keeps on accumulating until all the dues get cleared.

- If the amount remains unpaid even after the due date, the holder can even sue the maker in court as the notes receivable is the written document, which makes it risky.

Importance

In a world where a lot of business growth and daily sales are driven by providing credit, it is important to understand the importance of notes receivable accounting and its intricate details. Let us do so through the discussion below.

- Usually, the note receivable is not subject to the prepayment penalties. In this case, the note maker can freely pay off the amount before the maturity date, which can save the interest amount.

- They generally require a debtor who makes the notes to pay the interest, and the period of the notes extends typically for 30 days or more.

- Businesses often allow their customers or debtors to convert their overdue accounts into notes receivable. It provides more time to the debtor for repayment. They are shown in the shareholder’s balance sheet as the current assets if the note is due within one year; else, they will be shown under the non-current head in the balance sheet if the note is due after one year.

- The holder’s interest portion is shown as the interest expense in its profit and loss account. Thus such receivables that have an interest also affect both the balance sheet and profit and loss account of the holder of the same.

Recommended Articles

For more on Accounts Receivable, explore these related articles from our Accounts Receivable guide.