Part of our Banking Products guide

Bank Guarantee Meaning

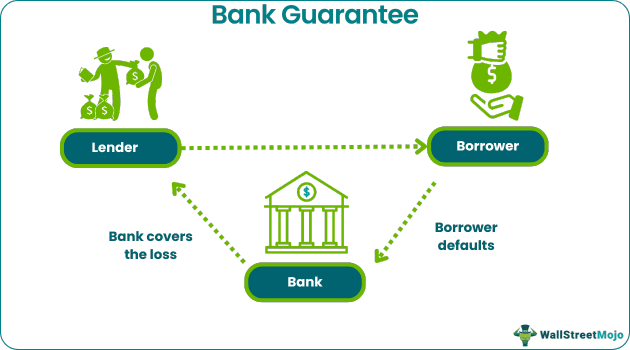

The term “bank guarantee,” as the name suggests, is the guarantee or assurance the financial institution gives to an external party if the borrower cannot repay the debt or meet its financial liability. In such an event, the bank will refund the amount to the party to whom the guarantee is issued.

It offers financial security to the beneficiary, encouraging him to enter into contracts with the applicant without worrying about the financial loss since such risks are secured by a bank guarantee. It increases the borrower’s credibility and secures the business operations too.

- A bank guarantee refers to the security or assurance the financial institution provides to an external party when the borrower cannot repay the debt or satisfy its financial liability. In such cases, the bank refunds the amount to the party who issued the guarantee.

- The two types of bank guarantees are performance guarantees and financial guarantees.

- A bank guarantee provides financial security to the beneficiary, encouraging them to enter contracts with the applicant without worrying about financial loss, as a bank guarantee assures them.

How Does Bank Guarantee Work?

Usually, a person applies for the bank guarantee letter with his regular banker, though he can also use the same with any other banker. Before issuing it, any bank assures itself of its creditworthiness by applying for bank assurance. In addition, creditworthiness can be checked by running CIBIL score, past financial statements, banking behavior, and projected financials.

Sometimes, a bank may also require the applicant to furnish some security instead of a bank guarantee. That is usually done by covering the amount of bank assurance by the issue of a fixed deposit on which a lien is created, and he cannot liquidate the same without the consent of the bank and the person in whose favor it is issued.

The person who is issued works as a security and ensures that bank assurance covers his finances.

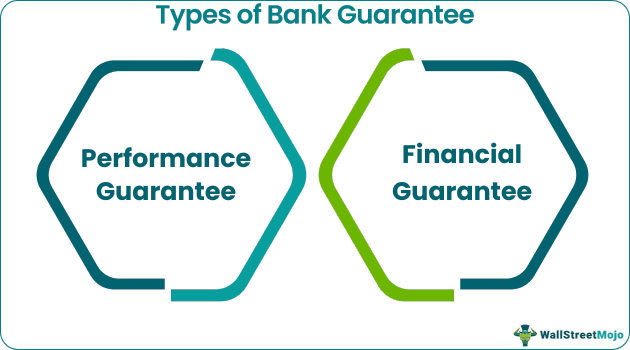

Types

There are two types: performance and financial guarantee.

- Performance Guarantee: It is regarding the performance of an act in the contract. If the applicant cannot perform as specified in the agreement, the issuer bank will recover the loss to accrue to the beneficiary.

- Financial Guarantee: This guarantee is used in those contracts where the applicant must furnish security to the beneficiary. Thus, the applicant provides the beneficiary with a financial guarantee when financial security is given.

Examples

Let us look at a few examples that will explain what financial and performance bank guarantee process looks like.

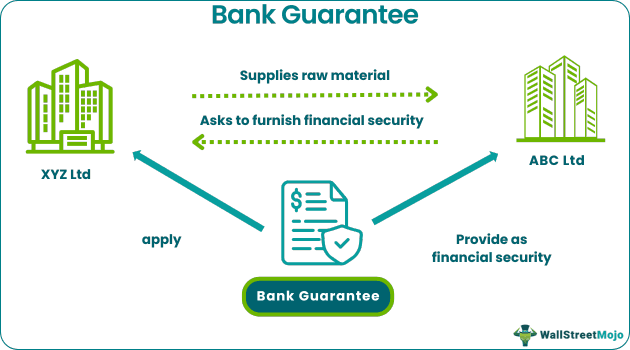

Example #1

ABC Ltd. enters into a supply contract with XYZ Ltd. where XYZ Ltd. is required to make a regular supply of raw materials to ABC Ltd. In addition, ABC Ltd. asks XYZ Ltd. to furnish financial security for the contract to adjust any deficiencies in raw materials.

Here, XYZ Ltd. can apply for a financial guarantee as it is required to provide financial security.

Example #2

Mr. X contracts with Mr. Y to complete the project within a stipulated time. In addition, Mr. Y must furnish a financial bank guarantee so that if the project is not completed within said time, they can recover the loss incurred by Mr. X.

In this case, Mr. Y shall apply for a performance guarantee as it is linked to the performance of the contract.

Thus, the above examples explain the bank guarantee process clearly.

Importance

It is considered to be important owing to the following reasons: –

- It is a security for the beneficiary since his funds flow from the applicant are secured.

- When small vendors deal with larger business players, they must furnish a bank guarantee. Thus, to ensure business, it becomes necessary for them.

- Getting a security issue shows a bank’s trust in the applicant. Thus, his credibility increases.

Charges

For providing the service of issuing a financial bank guarantee to the applicant, the applicant is charged certain fees based on the amount involved in bank assurance. Also, for providing the service of issuing bank guarantees to the applicant, the applicant is charged certain bank guarantee fee based on the amount involved in bank assurance. Also, charges for financial guarantee are more than performance guarantee as the same is comparatively riskier.

Advantages

- The beneficiary is saved from the financial risk involved in a contract.

- It helps a person secure more contracts since the financial risk is reduced.

- The credibility of the applicant increases on the issuance of the guarantee.

- Ensuring it is an easy process and requires minimal documents.

Disadvantages

- Some banks follow a very rigorous process to assess the applicant’s financial credibility; in such situations, issuing a bank guarantee can be lengthy.

- Banks look for profitability while assessing financial credibility. Thus, allocating a guarantee can be difficult for loss-making enterprises.

- One may be required to furnish security against the issue of guarantee.

Bank Guarantee Vs Letter of Credit

- The financial institution issues a letter of credit on the applicant’s request after receiving the services or goods. Thus, after the buyer accepts the services or goods, the bank makes the payment to the seller based on a letter of credit, and the amount paid is recovered by the bank later along with applicable bank guarantee fee.

- The buyer usually opts for the letter of credit in cases where there is a short-term financial shortage. On the other hand, a bank guarantee promises that if the applicant fails to pay the amount under contract or does not fulfill the performance criteria, the bank will pay the amount to the beneficiary. Thus, in a bank guarantee liability of the banker is secondary and arises only on the applicant’s failure.

Frequently Asked Questions (FAQs)

Frequently Asked Questions

1. What is a performance bank guarantee?

u003cpu003eIn a performance bank guarantee, the bank makes monetary compensation in case of delays in providing the operation or performance. The payment must also be made even if the service offers insufficiently.u003c/pu003e

2. What are bank guarantee charges?

u003cpu003eDepending on the bank guarantee type, fees are usually charged quarterly on the 0.75% or 0.50% bank guarantee value at the time of the bank guarantee validity period. Besides this, the bank must also impose application processing, handling, and documentation fees.u003c/pu003e

3. What is the performance bond vs. bank guarantee?

u003cpu003eA performance bond is a contract construction bond type that ensures a contractor will perform a project per the terms mentioned in the project owner contract, which is also known as the obligee. Moreover, the obligee can be a state, city, local government, private developer, or federal government. In comparison, a bank guarantee happens if the lending financial institution performs as a guarantor and assures to pay the losses if the borrower fails.u003c/pu003e

4. What is an electronic bank guarantee?

u003cpu003eAn electronic bank guarantee or an e-BG means eliminating physical stamping; instead, e-stamping occurs. Under this guarantee, the applicant and beneficiary may view a bank guarantee immediately.u003c/pu003e

Recommended Articles

This article is a guide to Bank Guarantee and their meaning. We explain its types, differences with letter of credit, charges, examples & disadvantages.. You may refer to the following articles to learn more about finance: –