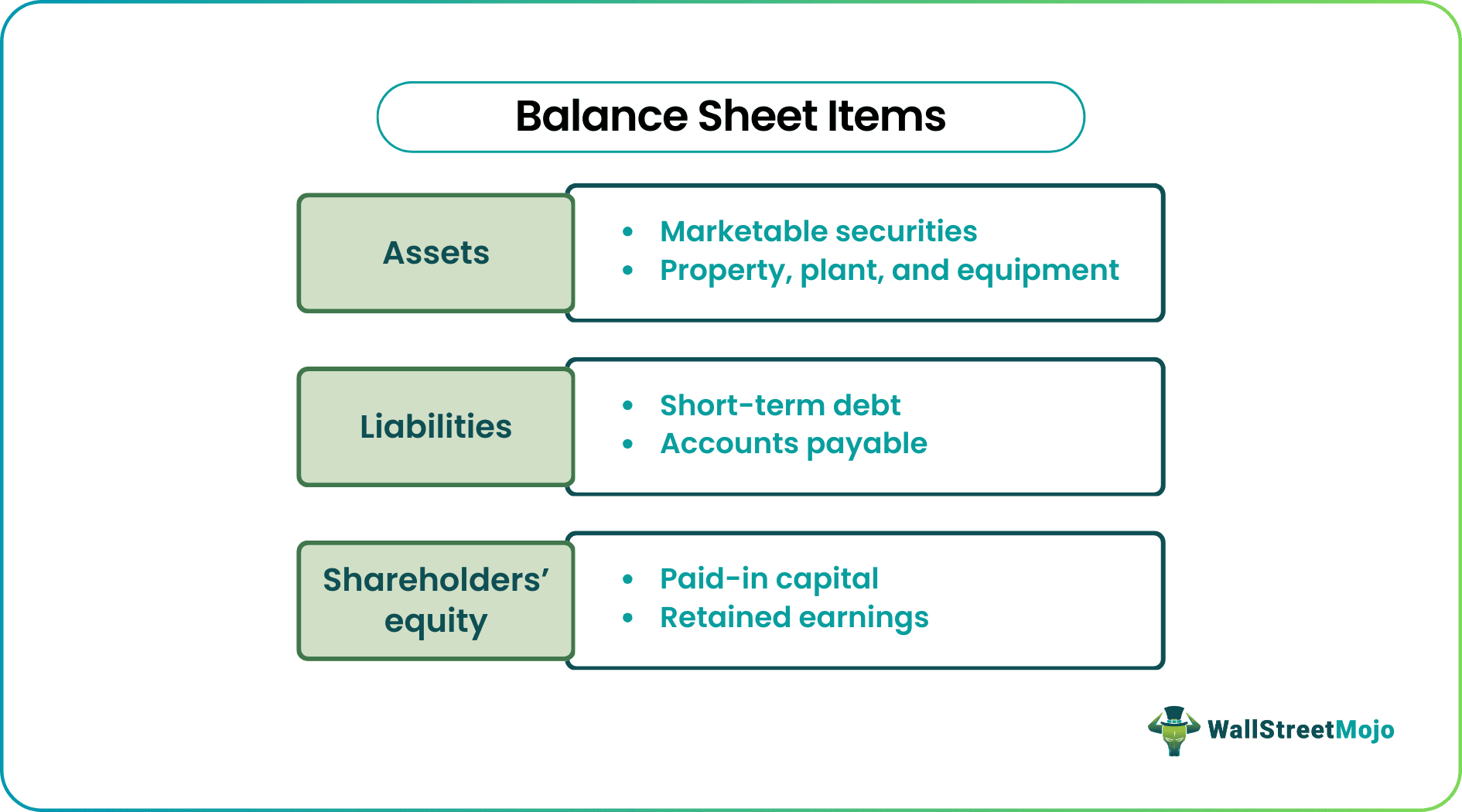

Balance Sheet Items Classifications

The items which are generally present in all the Balance sheet includes:

- Assets like cash, inventory, accounts receivable, investments, prepaid expenses, and fixed assets.

- Liabilities like long-term debt, short-term debt, Accounts payable, Allowance for the Doubtful Accounts, accrued and liabilities taxes payable.

- The Shareholders’ equity-like Share capital, additional paid-in capital, and retained earnings.

The most common balance Sheet items are listed below –

- Cash and Equivalents (Current Assets)

- Marketable Securities (Current Assets)

- Account Receivables (Current Assets)

- Inventories (Current Assets)

- Prepaid Expense (Current Assets)

- Property, Plant, and Equipment (Fixed Assets)

- Intangible Assets (Fixed Assets)

- Account Payable (Current Liabilities)

- Unearned Revenue (Current Liabilities)

- Short Term Debt (Current Liabilities)

- Current Portion of Long-term Debt (Current Liabilities)

- Other Accrued Expenses and Liabilities (Current Liabilities)

- Long term Debt (Long Term Liabilities)

- Paid-in Capital (Shareholders Equity)

- Retained Earnings (Shareholders Equity)

The Balance Sheet is based on fundamental accounting Equations which are below-

- Balance sheet items represent specific categories of assets, liabilities, and shareholders’ equity reported on a company’s balance sheet.

- Common balance sheet items include cash, accounts receivable, inventory, property, plant, equipment (PP&E), accounts payable, long-term debt, common stock, and retained earnings.

- Balance sheet items provide valuable information about a company’s financial position, liquidity, solvency, and capital structure.

- Understanding and analyzing balance sheet items helps stakeholders evaluate the company’s assets, liabilities, and equity and make informed decisions about its financial health.

Top 15 Balance Sheet Items List

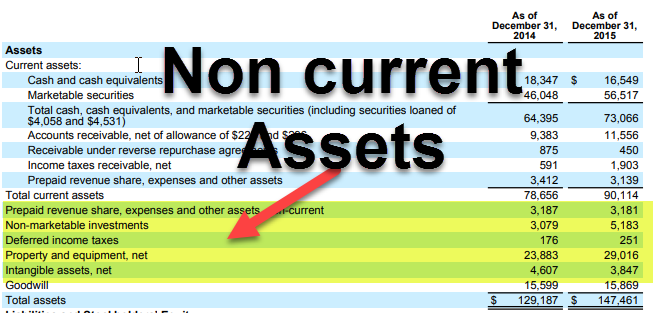

In the Balance Sheet, normally, Assets are shown on the left-hand side with decreasing order of their liquidity. That means Current Assets will come on the top, and then fixed Assets will be shown. Liabilities and equity are shown on the right-hand side. Liabilities are shown before equity and are in decreasing order of liquidity. Shareholder’s equity is shown below liabilities. As shown in IBM’s Balance Sheet,

Below are the main components of the Balance Sheet:-

- Current Assets

- Fixed Assets

- Current Liabilities

- Long Term Liabilities

- Equity

Current Assets

Assets are cash resources or can be converted to cash by selling. Companies can acquire assets using cash; they are known as “Use of Cash.” Current assets are expected to be realized in cash or sold to customers in a given operating cycle or one year. In a typical balance sheet, Current Assets are put before Fixed Assets. Below are the major items in Current Assets-

#1 – Cash and Equivalents

Cash is the funds that are readily available for disbursements. Cash and equivalents are the most liquid asset. Cash equivalents are assets with a maturity period of fewer than 90 days.

#2 – Marketable Securities

Marketable Securities are assets that can be converted into cash in one year and are readily available. In addition, marketable securities provide interest amounts to the firm.

#3 – Account Receivables

The amount which is owed to the entity by its customers. If the amount is owed to parties other than customers, it is known as Notes receivables.

#4 – Inventories

Inventories are assets that a business owner will sell in the future. The company is expected to sell its inventory shortly. That’s why it is put under Current Assets.

#5 – Prepaid Expense

The prepaid expense consists of the expense that the company has already paid, but until now, services for that payment have not been received. The company is expected to get the service shortly. Examples of prepaid expenses can be advanced insurance policy payments or advance salaries to the company’s workers.

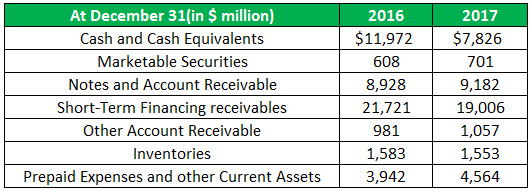

In IBM, below are the items under Current Assets:

Fixed Assets

Assets such as Property, Plant, and Equipment come under this category. These assets have a life of more than one year. Therefore, they are acquired to generate cash flow for many years. Since the cash flow from these assets comes in future years, they are capitalized for their useful life instead of making expenses at the time of purchase.

Fixed Assets can be broadly classified into the following:

#6 – Property, Plant, and Equipment

These are the assets that are tangible and relatively long-lived. It includes Buildings, land, hardware, Computers, etc.

#7 – Intangible Assets

Intangible Assets are assets that cannot be seen or touched physically. An Example of the intangible asset is the firm’s intellectual property, such as a patent or software. The cost of individual assets is also amortized over the years.

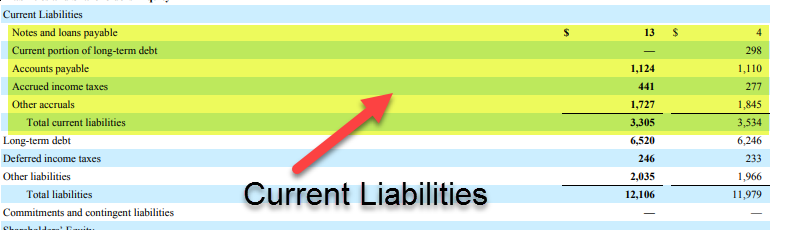

Current Liabilities

Current Liabilities are an obligation for the firm, which must be paid in a given accounting period or one year.

#8 – Account Payable

Accounts Payable is an operating liability that the company needs to pay its supplier for the goods and services received.

#9 – Unearned Revenue

If the revenue has been generated and still services/goods need to be delivered, it is accounted for under unearned revenue.

#10 – Short Term Debt

Debt whose maturity is less than one year comes under this category.

#11 – Current Portion of Long-term Debt

When companies take long-term loans such as bonds, they will have to pay interest or coupon payments for that loan each year. That amount that needs to be paid in a year will come under Current Liabilities.

#12 – Other Accrued Expenses and Liabilities

It could include money owed to employees etc.

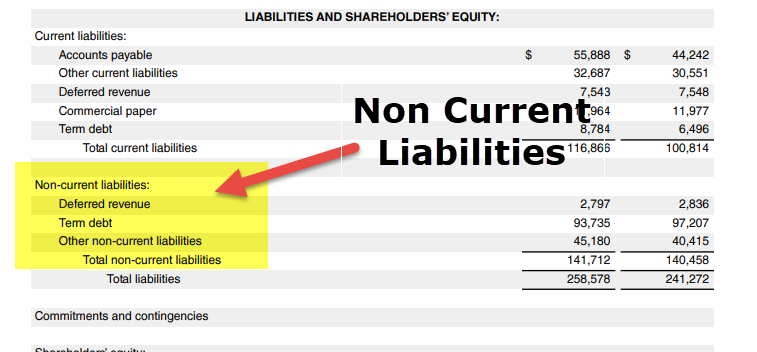

Long term Liabilities

Long term liabilities are the firm’s liabilities and are not expected to pay within one year.

#13 – Long Term Debt

Long-term liabilities include Long term debt and bonds issued by companies. Long-term debt can be taken from many sources such as banks, and will have a different interest and repayment structure. Bonds are the longer-term debt such as 30 years, in which the firm issues the bond to lenders and then makes coupon payment each period as stated in the bond structure. At the time of maturity, lenders get the last coupon payment and a face amount of bond.

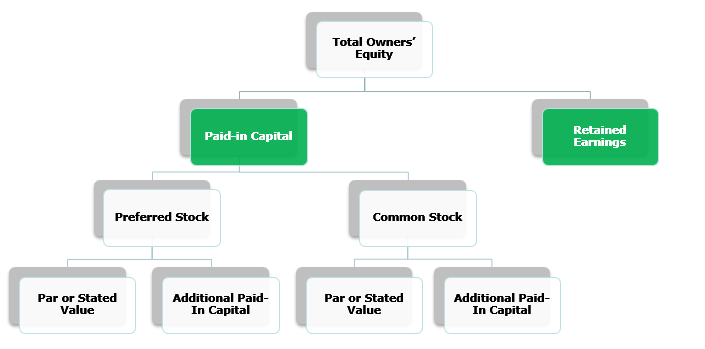

Shareholder’s Equity

Shareholder’s Equity is the difference between the Firm’s Assets and liabilities. It is a residual value to its shareholders. Shareholders’ equity mainly consists of Share Capital and Retained Earnings.

#14 – Paid-in Capital

Paid-in capital is the value of shares that the company has made by issuing shares to its shareholders. Shares can be of 2 types Common Stock and Preferred Stock. Preferred Stockholders have preferential rights to assets for the company before common shareholders. Stocks have a very negligible par value. Their additional paid-in capital is the difference between the value the company sells to shareholders and par value.

#15 – Retained Earnings

Retained Earnings are the amount that comes from the company’s internal profit. The firm has two options for net income either to pay the dividend or retain it to invest in some projects. Retained Earnings are the difference between Net Income and dividends paid.

Balance Sheet Video Explanation

Final Thoughts

As an investor, one should understand the meaning of all the balance sheet items, and it is interconnected with the Income Statement and Cash Flow Statement. Balance Sheets are also most prone to accounting adjustment (or we can say that manipulation), so we should also read the footnotes carefully in company reports to find out how the numbers are put in the accounts.

Frequently Asked Questions (FAQs)

What are current assets, and why are they important?

Current assets are balance sheet items expected to be converted into cash within one year or the business’s operating cycle. They include cash, accounts receivable, inventory, and short-term investments. Current assets provide insight into a company’s liquidity and ability to meet short-term obligations.

What are intangible assets, and why are they significant?

Intangible assets are non-physical assets that lack a physical presence but hold value for a company. Examples include patents, trademarks, copyrights, brand names, and goodwill. Intangible assets are important because they can contribute to a company’s competitive advantage and overall value.

Why is long-term debt a significant balance sheet item?

Long-term debt represents borrowed funds that are due beyond one year. It includes bonds, mortgages, and other long-term loans. Long-term debt is significant because it reflects the company’s obligations over an extended period and indicates its ability to manage and repay long-term financial commitments.

Recommended Articles

This article is a guide to Balance Sheet Items. Here we discuss the list of top 15 balance sheet items and practical examples and explanations. You may learn more about accounting from the following articles –