Part of our Shareholder Equity guide

What is Shareholders Equity?

A shareholders’ equity refers to the portion of a company’s net worth that the shareholders are entitled to receive when it liquidates. It is calculated by subtracting total liabilities from the firms’ total assets. The result helps determine how stable a company and its financial health are.

The shareholders’ returns are proportional to their investment in a firm. So, for example, if A has a 20 percent contribution and B has a 40 percent contribution, the latter’s share would be more than the former when the company liquidates or makes significant profits.

- Shareholder’s equity is the residual interest of the shareholders in the company, which indicates the extent of rights owners can exercise on the firm they have invested in.

- It is calculated as the difference between assets and liabilities.

- The final statement on the balance sheet reflects the change in the value of shareholder’s equity in a specific accounting period.

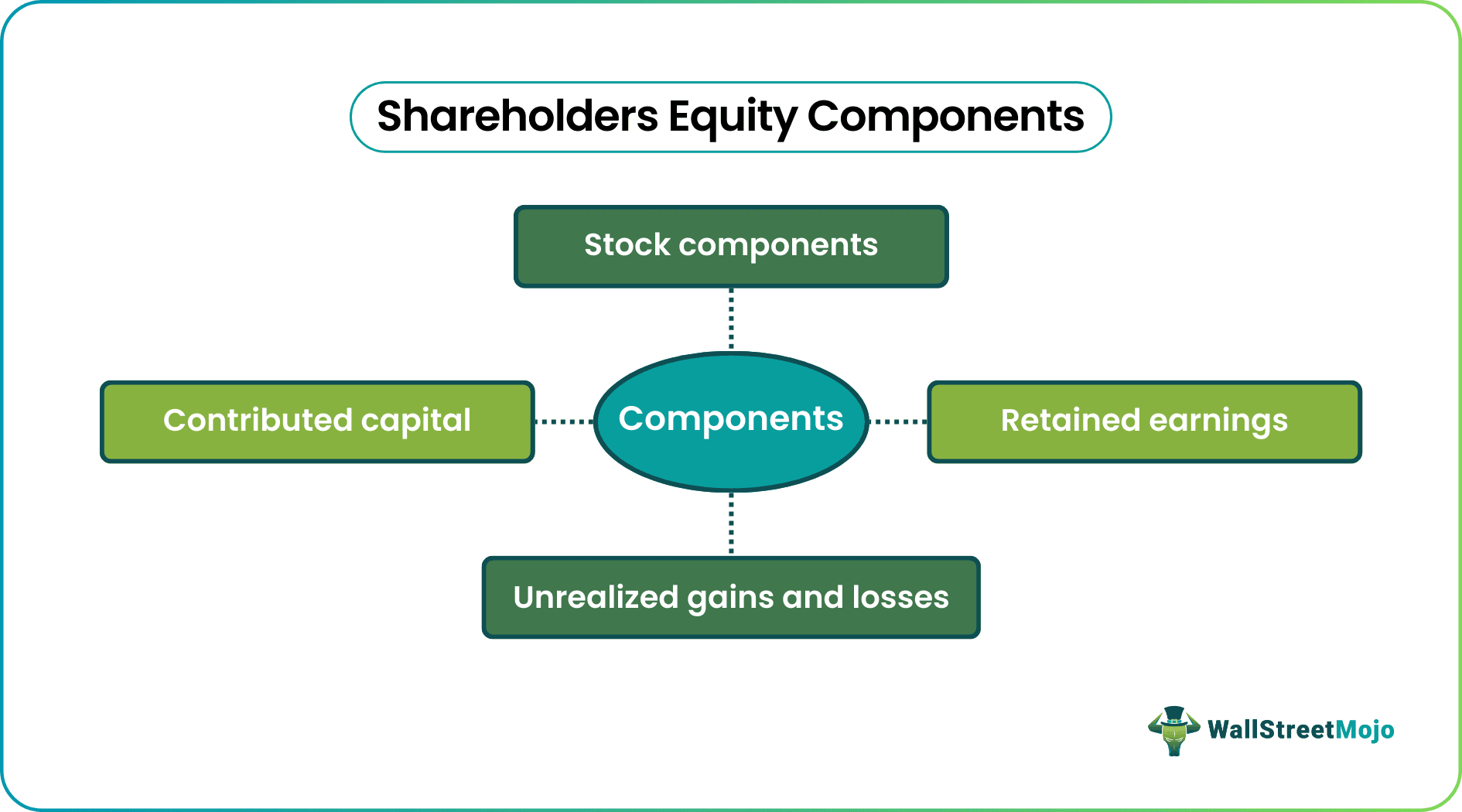

- Stock components, contributed capital, unrealized gains or losses, and retained earnings are a few components with respect to which the equity of shareholders is calculated.

Shareholders’ Equity Explained

Shareholders’ equity is the residual interest of the shareholders in the company they invest in. It includes not only the initially invested amount but also the returns on it, along with the reinvestments they make since the company’s inception. The reinvestment from the shareholders indicates their attitude towards the company, which is positive if the performance is good and as expected.

The total shareholders’ equity is calculated as the difference between the total assets a company has and the total liabilities or debt. While assets are the company’s resources and include everything from cash to physical items, liabilities are the debt it requires repaying. The liabilities count is normally built while the firms arrange funds to spend on assets.

Video Explanation of Shareholder’s Equity

Components

The shareholders’ equity comprises components that play an important part in determining the company’s net worth.

#1 – Stock Components

These include common stocks, preferred stocks, and treasury.

- Common stock is the most important component, with the holders being the company owners. They are the ones who receive the profits and deal with losses after the company pays interest and dividends to preference shareholders. The holders, in this case, also enjoy voting rights.

- Preferred stock is held to offer holders secondary rights in the net assets. They don’t have voting rights, but they are the ones who enjoy a fixed dividend even before anything is given to the common stockholders.

- Treasury shares are the total of all the common shares that the company purchases back. Thus, treasury shares are the opposite of common equity shares. Common stock has a credit balance, whereas treasury shares have a debit balance.

#2 – Retained Earnings

Retained earnings, as the name implies, reflect the gains and losses carried forward to the next financial year. It is the amount left with or kept aside by the company after it pays the dividend from net income. Normally, the investors and firms decide to reuse this amount and reinvest the same in the company.

#3 – Unrealized Gains and Losses

These include components that are not reflected in the income statements but affect the financial health of the companies.

#4 – Contributed Capital

Also known as additional paid-up capital, this component counts the additional amount that shareholders pay above the actual share price.

Examples

The following examples feature the shareholders’ equity statement and show how to calculate shareholders’ equity with respect to all the above-mentioned components.

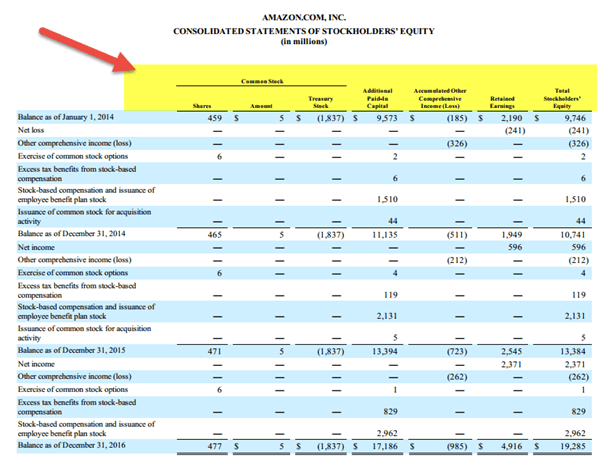

#1 – Statement Example

Let us look at Amazon’s consolidated statement below to check how the detailed breakups are reflected:

#2 – Calculation Example

Stephens has the following information about Company Y –

| Particulars | In US $ |

|---|---|

| Common Stock | 40,00,000 |

| Preferred Stock | 800,000 |

| Retained Earnings | 410,000 |

| Accumulated Comprehensive Income (loss) | (50,000) |

| Treasury Shares | 110,000 |

| Minority Interest | 600,000 |

All the required information is available below. Let us put the values according to the shareholders’ equity formula.

| Particulars | In US ($) |

|---|---|

| Common Stock | 40,00,000 |

| Preferred Stock | 800,000 |

| Retained Earnings | 410,000 |

| Accumulated Comprehensive Income (loss) | (50,000) |

| Treasury Shares | (110,000) |

| Minority Interest | 600,000 |

| Shareholders’ Equity | 56,50,000 |

Shareholders’ Equity vs Market Cap

Both shareholders’ equity and market capitalization or market cap appear to indicate the net worth of a company. However, these two terms have nothing to do with each other and exist independently. The differences between the two are:

| Category | Shareholders’ Equity | Market Capitalization |

|---|---|---|

| Definition | Depicts the ownership rights of the people who have invested in the company | Calculates the cumulative value of the shares/stocks in the company |

| Inclusions | All the components, which contribute to the net worth of the company, including upon liquidation | It is greater in value as it takes into account several factors, like current market trends, sales figures, patents, etc. |

| Value | Lower than the market cap | More than the book value or equity of the shareholders. |

The widening difference between the figures reflecting the two values indicates growth and profits, thereby making more and more investors invest in the firm. On the other hand, if the difference declines, it depicts that the maturity period is around the corner, and there is no scope for further growth.

Frequently Asked Questions (FAQs)

What is total shareholders’ equity?

Total shareholders’ equity is the term used to indicate the shareholders’ equity and is calculated as the difference between the total assets and the total liabilities a company holds. It is also referred to as the book value. This value helps investors identify the company’s financial health and determine whether they should continue investing in it, given its performance.

Is shareholders’ equity an asset?

No, it is equal to the value of the company’s assets. An asset is what a company owns and from which the liabilities are subtracted to obtain its equity value. In short, the asset value can be calculated by adding the firm’s equity and total debt or liabilities.

Can shareholders’ equity be negative?

The value can be both positive and negative, depending on the number of assets the companies own and their liabilities. While the asset value is normally more than the company’s liabilities, there can be instances where the figures reflect an opposite scenario. For example, in scenarios where the debt value exceeds the total assets that the firms own, the shareholders’ equity is negative.

Recommended Articles

This article has been a Guide to what is Shareholders’ Equity & its statement. Here we explain its components, examples along with its differences with market cap. You may also find some useful articles here: