What Is Unadjusted Trial Balance?

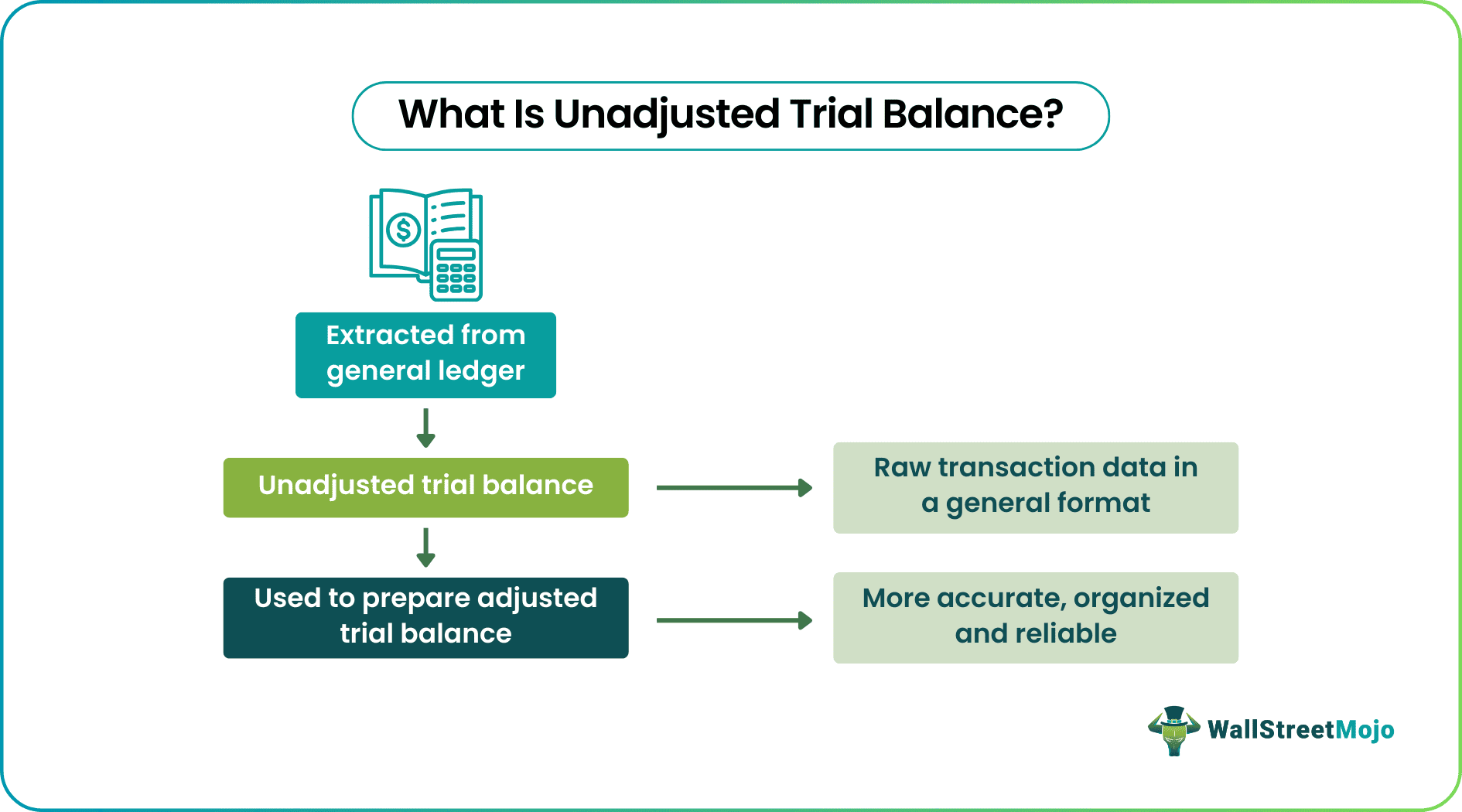

An Unadjusted Trial Balance is the account balance reported directly from the general ledger without adjusting the year-end journal entries. It is a starting point for analyzing account balances and adjusting entries.

It serves to be the source of all financial statements that a company creates. An unadjusted trial balance is prepared to ensure the accounts identify the errors and mistakes that may be present in the records so that the same could be avoided at the later stages.

Key Takeaways

Unadjusted Trial Balance Explained

Unadjusted Trial Balance is a direct report extracted by a business from its Double Entry Accounting system. It includes various payments received/made by the business which are not related to the accounting period for which financial statements are to be prepared and, as such, need to be adjusted to provide a correct picture of the business performance for the period for which financial statements are prepared. Also, it helps verify the balance of debits and credits, which is further reviewed by checking the balance of each account to prepare Adjusting entries as part of the Accounting cycle process, which begins when a transaction occurs and concludes with its inclusion in the financial statements.

Passing of adjusting entries to make an Unadjusted Trial Balance into an Adjusted Trial Balance is the final step after which Financial Statements are prepared, and the correct Adjusting entries must be done, which will ultimately result in the preparation of correct Financial Statements.

These year-end adjusting entries are considered necessary to make an Adjusted Trial Balance and include passing adjusting journal entries which include entries namely:

- Receivables that do not apply to the period for which Accounting records are to be prepared.

- Accrued Expenses /Interest related

- Prepaid Income/Expenses items

- Money received for work that is to be done in another accounting period. For example, Advance payments from clients, Subscription received, etc.

- Payments are made for periods other than the period for which accounting records are being prepared—for example, Insurance Premium, etc.

Purpose

The unadjusted trial balance is prepared at the end of the reporting period as a rough draft of the financial transactions, which are organized in order later on in the form of financial statements, which are more reliable and accurate.

- The primary purpose is to discover the errors and mistakes that occurred during the bookkeeping process.

- It is also the basis for finding occurred errors for any of the reasons below,

- Errors of Omission

- Error of Commission

- Error of Principle

- Compensating errors

How To Prepare?

There are eight steps in the accounting cycle, the fourth step being the preparation of an unadjusted trial balance. Companies have to have an organized and adjusted trial balance before they prepare their financial statements to reflect the liabilities, assets, revenues, and expenses of the organization.

However, before every transaction is presented in an organized manner, there is a rough list of transactions accommodated in the unadjusted trial balance. This is the document that lists the accounts and balances before the last adjustments have been made. This unadjusted financial document is prepared based on the general ledger or other sources recording the transactions.

The steps to prepare this unadjusted trial balance in accounting are:

- A table with three distinct columns is created and labeled as Accounts, debit, and Credit starting from the leftmost column. This is a general format where the Accounts column has the names of the accounts, the Debit column has the debit balances, and the Credit column has credit balances. The separation of columns helps tally or check mismatches between the credit and debit balances and totals.

- The first account name on the table is of the assets followed by liabilities and then shareholders’ equity. While the former has a debit balance, the rest two reflect the credit balances.

- Then, the next step is to list down the revenue and expense, which when synchronized make up the income statement. Here, the revenue account will have debit balances, and expense accounts will have credit balances.

- In the unadjusted financial document, check the credits and debit balances, and add them all, mentioning the total at the bottom.

If there is a mismatch in the totals on both sides, the next step is to rectify the errors in the records and prepare an accurate dataset for creating a reliable financial statement.

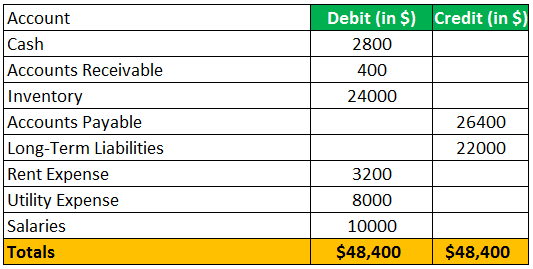

Example

Let us consider a hypothetical example to understand the unadjusted trial balance meaning better:

ABC Company records its journal entries and posts them to ledger Accounts. Below is the Unadjusted Trial Balance as of Dec 31, 2017

- Rent Expense includes payment of $ 1200 for January 2018

- The Utility Expense bill of $ 8000 is due in January 2018

Adjusting entries to be passed to adjust the above two expenses are as follows:

- Rent Expense

| Date | Particulars | Debit | Credit |

|---|---|---|---|

| Dec 31 2017 | Prepaid Rent | $1,200 | $1,200 |

| Cash | $1,200 |

- Utility Expense

| Date | Particulars | Debit | Credit |

|---|---|---|---|

| Dec 31 2017 | Utilities Expense | $8,000 | |

| Accrued Expense | $8,000 |

After that, Adjusting Entries will be passed in the relevant accounts to prepare Adjusted Trial Balance, which is the last step before Financial Statements are produced.

Advantages

With unadjusted trial balances, accounting professionals try to remove errors that may occur while recording transactions. As a result, when adjusted, these records are more organized and proper. Let us have a look at some of the advantages of this method of accounting:

- It can be used to evaluate the internal control of the business accounting system.

- It will be a base for finding the errors and posting adjusting entries by skilled persons.

- It will also be a base for preparing financial statements after proper adjustment entries.

- It also supports the audit team in preparing a proper audit program based on the capacity of accountants.

Disadvantages

Besides the benefits, this method also has some flaws, which one must know of before trusting it completely. Let us have a look at a few of them:

- It cannot be a base for any references to prepare the final reports of the company without further adjustments.

- Possibilities of errors may be high in the unadjusted trial balance as the works have been done with the primary data.

- Passing the adjustment entries will be based on identifying errors in the books.

- The accountant requires high knowledge of accounting standards and applicable GAAP to post the adjusting entries.

Unadjusted Trial Balance vs Adjusted Trial Balance

Both unadjusted and adjusted trial balances have an important role to play when it comes to being the source of transactions companies undertake. However, the way of presenting the information differs. While the former is about noting down the transactions roughly, the latter is the means of presenting data in proper order.

The difference between the adjusted and unadjusted trial balance, apart from the one mentioned above, has been listed below:

- Unadjusted trial balance is the financial document that is a rough dataset and not the final one. On the other hand, the adjusted trial balance has the entries that are adjusted and finalized for the preparation of financial statements further.

As the name suggests, the unadjusted version has entries that are not adjusted or in order, while the adjusted ones are used to adjust the two sides of the ledger – the debit and credit. Plus, the adjusted trial balance has one extra account mentioned, i.e., net/loss of income.

Recommended Articles

This has been a guide to Unadjusted Trial Balance and its definition. Here we discuss its examples, uses, advantages, and disadvantages. You may also have a look at these articles below to learn more about accounting –