Part of our Trial Balance guide

What Is Adjusted Trial Balance?

Adjusted Trial Balance refers to the general ledger balances reflecting adjustments, which include accrued expenditure and non-cash expenses. The list and the balances of the company’s accounts are presented after the adjusting journal entries are made at the year-end. Those balances are then reported on respective financial statements.

A trial balance sheet, which in itself, is a complete summary of an organization’s transaction gives a clearer picture of it when adjusted to such expenses. It is an internal document, a non-financial statement.

Adjusted Trial Balance Explained

Adjusted trial balance records the account balances of an organization after adjusting the transaction to various expenses, including the depreciation amount, accrued expenses, payroll expenses, etc. This, in turn, gives businesses a clear picture of where they stand. This trial balance type allows businesses have a summarized view of all the account balances post-adjustment to respective expenditures.

When accounts are prepared at the end of the accounting period, ledger balances must be updated with relevant adjustments, which are the results of the partial transaction, improper transactions, and skipped transactions. Such types of transactions are deposits, Closing Stocks, depreciation, etc. Once all necessary adjustments are made, a new second trial balance is prepared to ensure that it is still balanced. This new trial balance is called the adjusted trial balance.

When it comes to the adjustment made, the adjusted trial balance sheet is left with information that is relevant for a particular period as per the information that the business organization seeks. The adjustments made, however, are classified into different categories, which include – deferrals, accruals, missing transactions, and tax adjustments.

As the adjusted trial balance is prepared for a specific period, transactions not relevant to this requirement are removed. These ate included in deferrals. For example, a prepaid amount is not valid for the current period. So, it is removed, being an inappropriate detail for that period-specific adjusted trial balance sheet.

The next type of adjustment is the accrual, which ensures inclusion of the future payments that the business entity is entitled to make. Such expenses might include paying for a rented space or any upcoming payments in the queue.

There are instances when companies end up missing out mentioning the transactions that have occurred in the bookkeeping records. Such amount can be included in these documents.

Another one is the tax adjustment. As the name suggests, it includes deductions with respect to the tax liabilities.

Purpose

There are multiple financial statements that are prepared by the businesses at the end of a financial year. Still, they prepare an adjusted trial balance as a ready reference. Its purpose is to ensure that the total amount of Debit Balance in the general ledger is equal to the total amount of Credit Balance in the general ledger.

- The primary purpose of the adjusted trial balance is a document that shows the total amount of debt against the total amount of credit. It is not considered as a financial statement because it is only used as an internal document.

- Hence, it is beneficial for big companies to adjust many entries. It also ensures that entries are done correctly; if balances entered into financial statements are incorrect, the financial statements themselves will be inaccurate, and the total must be equal.

- Any difference indicates some error in entries, ledger, or calculations. So it gives a clear picture of the performance of the company. It also helps to monitor the company’s performance as the adjusted trial balance is prepared after considering all adjustments of entries of different accounts.

Accounting

The entries follow a proper adjusted trial balance format. Listed below are the points that show how the entries are made while accounting for these post-adjusted transactions:

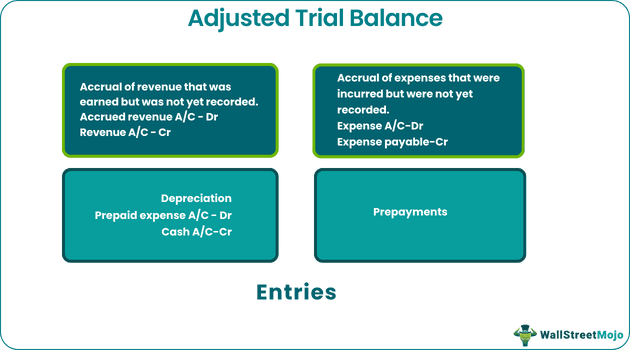

#1 – Accrual of earned revenue but not yet recorded.

It arises when an asset is a sale, but the customer has not yet billed for the same. Eg. Account receivable, accrued interest.

Accrued revenue A/C – Dr

Revenue A/C- Cr

#2 – Accrual of expenses incurred but not yet recorded.

It is an expense recorded in accounts before the payment is made. E.g., Interest payable, salaries, and wages payable.

Expense A/C- Dr

Expense payable- Cr

#3 – Prepayments

Prepayment is the setting of payment before its due date. Eg. Prepaid rent.

Prepaid expense A/C- Dr

Cash A/C- Cr

#4 – Depreciation

Depreciation is a non-cash expense identified to account for the deterioration of fixed assets to reflect the reduction in useful economic life.

Example

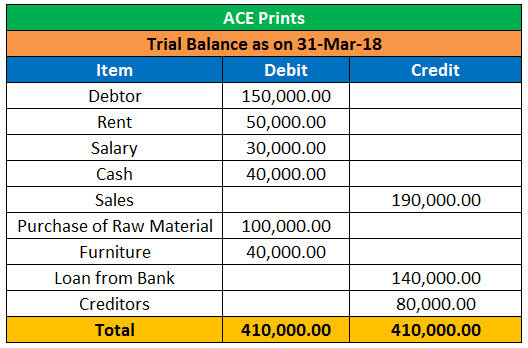

Let us consider the following adjusted trial balance example to understand the concept better:

Suppose a printing company name ACE Prints run a small business of printing, their trial balance as on 31st March’2018 is below:-

We get clear information from trial balance about debit entries and credit entries. But there is some more information required to adjust the trial balance.

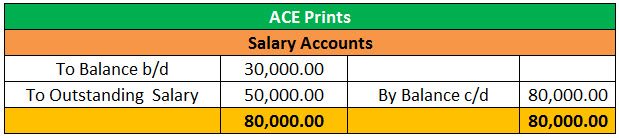

- The salary due to the employee as on 31st March’2018=$ 50,000

- Rent is inclusive of refundable deposit of= $ 20,000

The adjustments need to be made in the trial balance for the above details.

The below entry is done in the Salary account.

Here, the adjustment will be $ 80,000.00 as the total salary payable is $ 80,000.

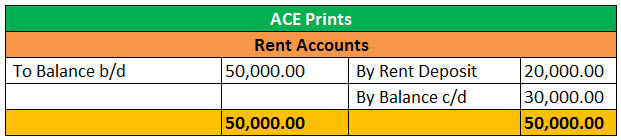

The below entry is done in the Rent account.

Here, the adjustment will be $ 50,000.00 as the rent deposit is $ 20,000, the rent payment will be $ 30,000.

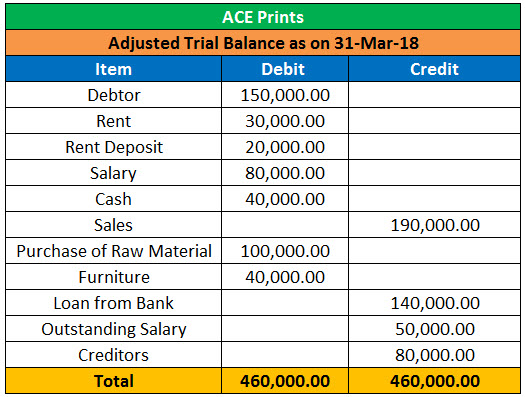

The adjusted trial balance will be as follows:-

The adjustments are made as below:-

- A rent deposit is taken into consideration.

- An outstanding salary also included in it.

Hence, the trial balance includes all considerable adjustments, which is termed as adjustment trial balance.

How to Make?

There are two methods for the preparation –

- The method first is similar to the preparation of an unadjusted trial balance[. The ledger accounts are adjusted for the end of periods adjusting entries, and the account balance is listed to prepare an adjusted trial balance. This method takes a lot of time, but it is very systematic and usually used by large companies where many adjustments need to be made by companies in their ledger accounts.

- The second method is quite fast and straightforward, but it is not systematic and usually used by small companies where less adjustment needs to be done. In this adjustment, entries are directly added to the unadjusted trial balance to convert it to an adjusted trial balance.

Adjusted Trial Balance vs Trial Balance

Financial documents prepared by a company are of multiple types of which is a raw trial balance sheet that it prepared. Below are some of the points of distinctions to identify how it differs from its adjusted version. Let us a have a look at it:

- A trial balance is prepared first, whereas adjusted trial prepared post-trial balance. Trial balance excludes entries like accrued expense, accrued revenue, prepayment, and depreciation, whereas adjusted trial balance includes the same.

- A trial balance is a list of closing balances of ledger account on a particular point of time. In contrast, adjusted balance is a list of general account and their balances at a point of time after the adjusting entries have been posted.

Adjusted Trial Balance vs Unadjusted Trial Balance

Trial balance can be in its adjusted form or unadjusted form. Both these forms have their own set of adjustments and business entities prefer having both of them ready with them for reference as and when required. Let us have a look at the differenced=s between the two:

- The unadjusted form, as the name suggests, is the form of trial balance that is not adjusted to any expenses. On the other hand, adjusted trial balance is adjusted to the liabilities for the period in question.

- The unadjusted version is the one that records all revenues and expenses as it is. On the contrary, the adjusted form records the revenues and expenses after the adjustment are made. These adjustments include payroll expenses, non-cash expenses, etc.

Adjusted Trial Balance Video

Recommended Articles

This article has been a guide to what is Adjusted Trial Balance. We explain it along with example, accounting, purpose, how to make it, vs unadjusted trial balance. You may learn more about accounting from the following articles –