What is Post Closing Trial Balance?

Post Closing Trial Balance is the list of all the balance sheet items and their balances, excluding the zero balance accounts. It is used for verification that temporary accounts are properly closed and that the total balances of all the debit accounts and all the credit accounts are equal.

Post-Closing Trial Balance is an accuracy check to verify that all debit balances equal all credit balances, and hence net balance should be zero. It presents a list of accounts and balances after closing entries have been written and posted in the ledger.

Also, it determines whether any balances are remaining in the permanent accounts after closing entries have been journalized. Since these are determined to be temporary accounts, it contains no sales revenue entries, expense journal entries, no gain or loss entries, etc. As part of the closing process, the balances in these movements to the retained earnings account.

Why do you need Post-Closing Trial Balance?

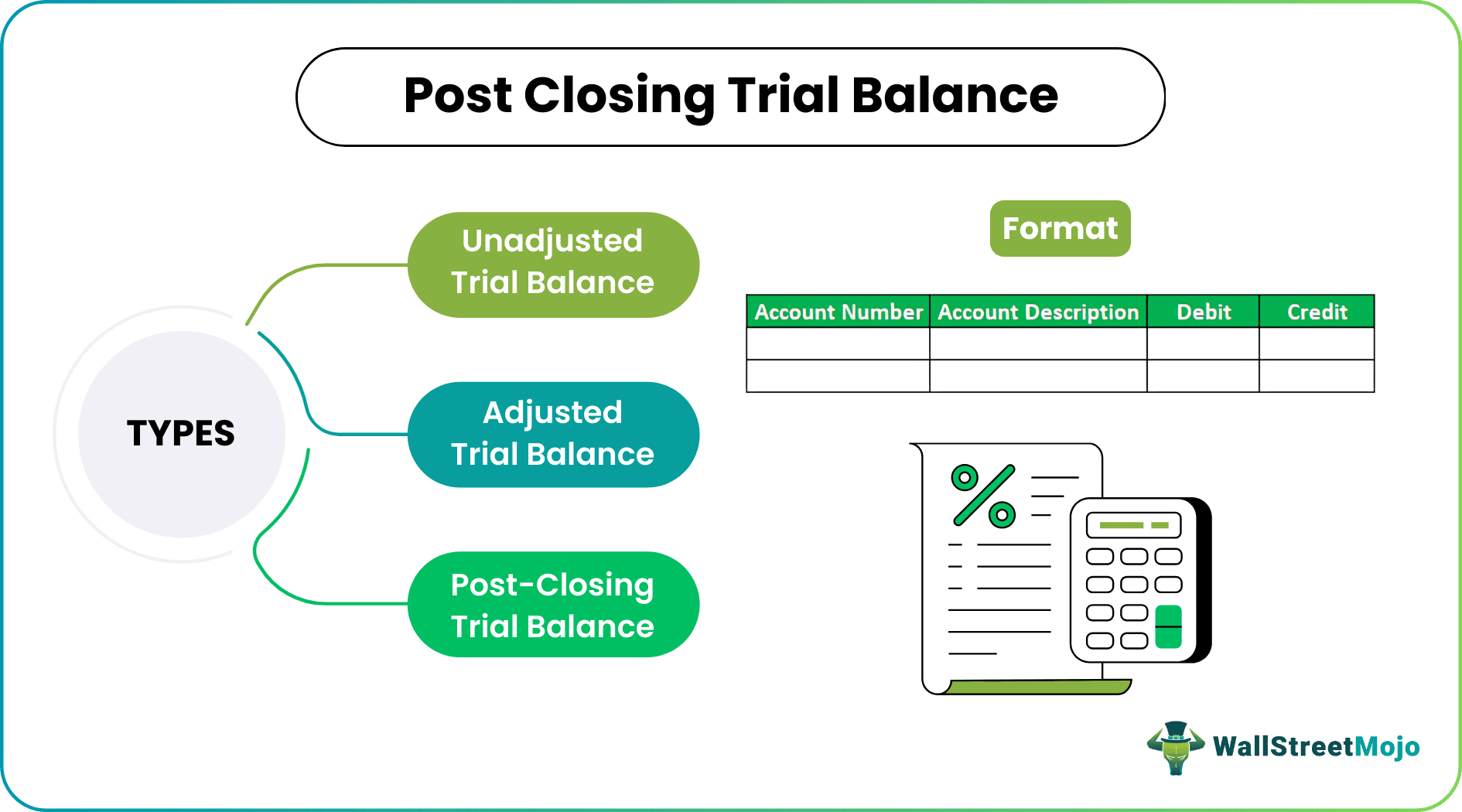

There are three types of trial balance in accounting. They are an unadjusted trial balance, adjusted trial balance, and post-closing trial balance. All of the above tests whether all debits equal all credits.

- The unadjusted trial balance is prepared after entries for transactions have been journalized and posted to the ledger.

- An adjusted trial balance contains nominal and real accounts. Nominal accounts are those which have entries from the income statement, and real accounts are those which have entries from the balance sheet.

- The post-closing trial balance is used to check the debits and credits after closing entries for transactions have been made.

Then the accountant’s job is to determine whether there is a zero net balance, i.e., all debit balances equal all credit balances. Then the accountant raises a flag to ensure that no further transactions are recorded for the old accounting period. Hence, any additional transactions are recorded for the next accounting period. As mentioned above, it ensures that no temporary accounts are remaining and all debit balances equal all credit balances.

Format

It has a similar format to other trial balances. It contains columns for the account number, description, debits, and credits for any business or firm. Various accounting software makes it mandatory that all journal entries must be balanced before allowing them to be posted to the general ledger. Hence it is improbable to have an unbalanced trial balance.

As balance sheet entries are listed in the trial balance, it is done similarly to the balance sheet with first assets, then liabilities, and then equity. Both the debits and credit totals are calculated at the end, and if these are not equal, one can know there must have been some mistake in preparing the trial balance.

Similar to the financial reports, trial balances are prepared with three headings, which list the company name, type of trial balance, and ending date of the reporting period.

Example of Post-Closing Trial Balance

Let’s take an example for a company XYZ.

Recommended Articles

This article has been a guide to Post Closing Trial Balance. Here we discuss the format of the Post-Closing Trial Balance (account number, account description, debit, credit) and its examples. You can learn more about it from the following articles –