Part of our Trial Balance guide

Differences Between Trial Balance and Balance Sheet

→ Explore all 93 Balance Sheet articles

Trial Balance vs. Balance Sheet –The trial balance is an internal document. And the balance sheet is prepared to disclose the company’s financial affairs to external stakeholders.

In simple terms, a balance sheet is an extension of the accounts recorded in the trial balance. When you begin learning a balance sheet, you will be given a trial balance and asked to prepare a balance sheet format using the accounts mentioned in the trial balance.

To understand trial balance, we need to start from debit, credit, journal, and ledger. If these four concepts are digested, trial balance becomes easy.

And from the trial balance, we can make a balance sheet which we will create in this article.

Trial Balance vs. Balance Sheet Infographics

There are many differences between the trial balance vs. the balance sheet. Let’s have a look –

What is Trial Balance?

The trial balance is the total of all the end balances directly taken from the ledger accounts to see whether the total of debit and the total of credit are equal. If debit balances don’t match with credit balances, then the accountant needs to investigate whether there’s an error in the recording or not.

If you understand debit, credit, journal, and ledger, the trial balance is as easy as possible.

Also, you may look at this in-depth article on How to Prepare a Trial Balance in accounting?

So, we will learn these four concepts first before going into the trial balance format with examples.

Debit & Credit

The simple rules of debit and credit are as follows. It would help if you remembered these rules to record all the transactions in the future.

- Debit the account when the assets/expenses increase and the liabilities/revenues decrease.

- Credit the account when the assets/expenses decrease and the liabilities/revenues increase.

We will take an example to illustrate this.

Let’s say Mr. M sells a product in cash.

Here, we have two accounts – “sales” and “cash.”

“Sales” is a revenue account, and “cash” is an asset account.

By following the formula of debit and credit, we can approach this transaction.

First, Mr. M is selling the product; his revenue is increasing. That means the “sales” account is increasing. And as he is receiving cash instead of the product he is offering, the “Cash” account is also increasing.

According to the rule of debit and credit, we will debit the account when the asset increases, and we will credit the account when revenue is increasing.

So, “cash” will be debited here, and “sales” will be credited.

Also, have a look at this detailed article on Debit vs. Credit.

Trial Balance vs. Balance Sheet Video

Journal entry

If you understand debit and credit, a journal entry is easy. In the journal entry system, you need to record the debit and credit accounts properly.

Let’s take a simple example to illustrate this.

Example of Journal Entry

More capital is being invested in the company in the form of cash.

Here, cash is an “asset” account, and capital is a “liability” account, and both are increasing.

According to the rule of debit and credit, if a “liability” account increases, we will credit the account, and if an “asset” account decreases, we will debit the account.

The whole journal entry would be –

Cash A/C……Debit

To Capital A/C……Credit

Ledger Entry

We will record the same example in the ledger entry system.

Ledger entry would be recorded in the “T” format.

Let’s see how it’s done.

The journal entry was –

Cash A/C……Debit…..$10,000 –

To Capital A/C……Credit… – $10,000

Debit Cash Account Credit

| To Capital Account | $10,000 | ||

| By balance c/f | $10,000 |

Debit Capital Account Credit

| By Cash Account | $10,000 | ||

| To balance c/f | $10,000 |

Introduction of trial balance

In the previous example, we found out the end balance of the cash account and capital account. Therefore, these end balances will appear in the trial balance.

And it will look like the following –

Trial Balance of MNC Co. for the year-end

| Particulars | Debit (Amount in $) | Credit (Amount in $) |

| Cash Account | 10,000 | – |

| Capital Account | – | 10,000 |

| Total | 10,000 | 10,000 |

Suspense account

This is a temporary account in the trial balance.

Creating this account balances the trial balance until the error is discovered temporarily.

When you see a suspense account in the trial balance, know that either the debit balance or the credit balance does not match another.

This suspense account is created since a proper account can’t be identified until the error gets discovered.

Here’s an example of a suspense account –

Trial Balance of MNC Co. for the year-end

| Particulars | Debit (Amount in $) | Credit (Amount in $) |

| Cash Account | 10,000 | – |

| Sales Account | – | 60,000 |

| Debtor Account | 40,000 | – |

| Creditor Account | – | 25,000 |

| Salaries Account | 15,000 | – |

| Advertisement Account | 10,000 | – |

| Capital Account | – | 10,000 |

| Suspense Account* | 20,000 | – |

| Total | 95,000 | 95,000 |

*Note: Since the debit balance is less than the credit balance, we created a suspense account to match up debit and credit balances until we find the error.

Example and format of Trial Balance

In this section, we will look at a complete trial balance, and then in the next section, “What is Balance Sheet?” we will make a balance sheet out of it.

Trial Balance of ABC Co. for the year-end

| Particulars | Debit (Amount in $) | Credit (Amount in $) |

| Cash Account | 45,000 | – |

| Bank Account | 35,000 | – |

| Investments Account | 100,000 | – |

| Equipment Account | 30,000 | – |

| Outstanding expenses | – | 15,000 |

| Prepaid Expenses | 25,000 | – |

| Debtor Account | 40,000 | – |

| Creditor Account | – | 25,000 |

| Shareholders’ Equity | – | 210,000 |

| Long term debt Account | – | 50,000 |

| Plant & Machinery Account | 45,000 | – |

| Retained Earnings | – | 20,000 |

| Total | 320,000 | 320,000 |

What is the Balance Sheet?

The balance sheet balances two sides – assets and liabilities.

For example, MNC Company took a loan from a bank of $20,000 in cash. The effect of this transaction would be on two sides –

- First, on the asset side, there would be the inclusion of “cash” of $20,000.

- And then, on the liability side, there will be a “debt” of $20,000.

You can see that the transaction has two-fold consequences which balance each other. First, under the balance sheet, these two accounts get balanced.

This is a very high level of understanding of the balance sheet.

Let’s understand each concept under the balance sheet.

Assets

Let’s look at assets first.

Under assets, first, we will consider “current assets.”

Current assets are assets that can easily be liquidated into cash. Here’re the items that we can consider under “current assets” –

- Cash & Cash Equivalents

- Short-term investments

- Inventories

- Trade & Other Receivables

- Prepayments & Accrued Income

- Derivative Assets

- Current Income Tax Assets

- Assets Held for Sale

- Foreign Currency

- Prepaid Expenses

Have a look at the example of current assets –

| L (in US $) | O (in US $) | |

| Cash | 3500 | 2600 |

| Cash Equivalent | 1900 | 1900 |

| Accounts Receivable | 2400 | 2200 |

| Inventories | 1400 | 1200 |

| Total Current Assets | 9200 | 7900 |

After current assets, we will look at “non-current assets,” also called “fixed assets.” These assets pay off for more than one year.

Under “non-current assets,” we would include the following items –

- Property, plant, and equipment

- Goodwill

- Intangible assets

- Investments in associates & joint ventures

- Financial assets

- Employee benefits assets

- Deferred tax assets

If we add up “current assets” and “non-current assets,” we will get the “total assets.”

Liabilities

Under the liability section, we will first talk about “current liabilities.”

Current liabilities are liabilities that can be paid off within a year. We will consider the following items under current liabilities –

- Financial Debt (Short term)

- Trade & Other Payables

- Provisions

- Accruals & Deferred Income

- Current Income Tax Liabilities

- Derivative Liabilities

- Accounts Payable

- Sales Taxes Payable

- Interests Payable

- Short Term Loan

- Current maturities of long term debt

- Customer deposits in advance

- Liabilities directly associated with assets held for sale

Let’s have a look at the format of current liabilities –

| L (in US $) | O (in US $) | |

| Accounts Payable | 4100 | 2500 |

| Current Taxes Payable | 1700 | 1400 |

| Current Long-term Liabilities | 2900 | 1000 |

| Total Current Liabilities | 8700 | 4900 |

Now, we will talk about “non-current liabilities.”

Non-current liabilities include the following items –

- Financial Debt (Long term)

- Provisions

- Employee Benefits Liabilities

- Deferred Tax Liabilities

- Other Payables

If we add up “current liabilities” and “non-current liabilities,” we will get “total liabilities.”

Now, if we remember the equation of the balance sheet, which is –

Assets = Liabilities + Shareholders’ Equity

We will now look at shareholders’ equity to complete the above equation.

Shareholders’ Equity

Here’s the format of shareholders’ equity. If you can remember this format, forming the shareholders’ equity statement would be simpler –

| Shareholders’ Equity | |

| Paid-in Capital: | |

| Common Stock | *** |

| Preferred Stock | *** |

| Additional Paid-up Capital: | |

| Common Stock | ** |

| Preferred Stock | ** |

| Retained Earnings | *** |

| (-) Treasury Shares | (**) |

| (-) Translation Reserve | (**) |

If we add up “total liabilities” and “shareholders’ equity,” we will equate the total amount with the total amount of “total assets.”

Example of Balance Sheet

We will now look at the trial balance we saw in the previous section. From that trial balance, now we will form a balance sheet.

Balance Sheet of ABC Company

| 2016 (In US $) | |

| Assets | |

| Cash | 45,000 |

| Bank | 35,000 |

| Prepaid Expenses | 25,000 |

| Debtor | 40,000 |

| Investments | 100,000 |

| Equipment | 30,000 |

| Plant & Machinery | 45,000 |

| Total Assets | 320,000 |

| Liabilities | |

| Outstanding expenses | 15,000 |

| Creditor | 25,000 |

| Long term debt | 50,000 |

| Total Liabilities | 90,000 |

| Stockholders’ Equity | |

| Shareholders’ equity | 210,000 |

| Retained Earnings | 20,000 |

| Total Stockholders’ Equity | 230,000 |

| Total liabilities & Stockholders’ Equity | 320,000 |

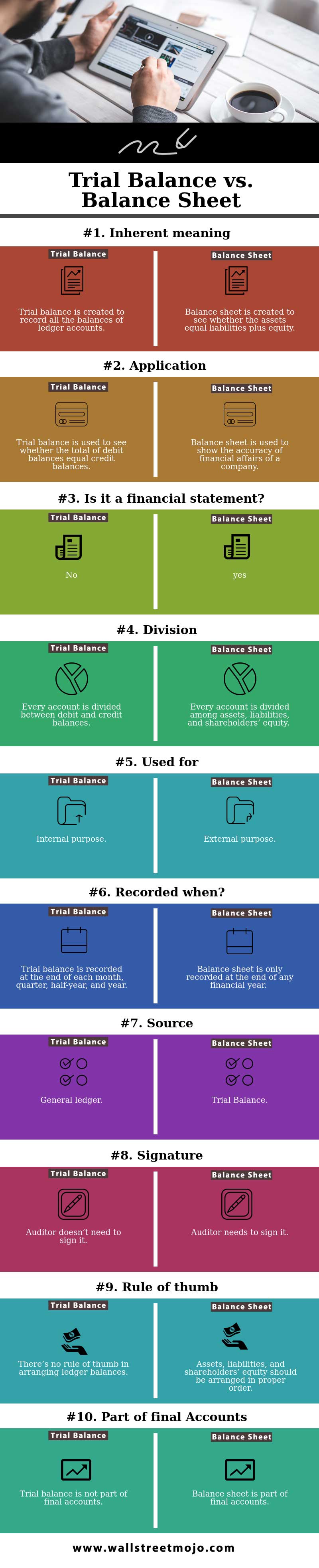

Key differences – Trial Balance vs. Balance Sheet

There are many differences between the trial balance vs. the balance sheet. Here are they –

- Trial balance is an internal statement. A balance sheet is an external statement.

- The trial balance is divided among two types of accounts – debit and credit. Undertrial balance, the debit balance, and the credit balance should be equal. A balance sheet is divided into assets, liabilities, and shareholders’ equity. The balance sheet should always maintain the “assets = liabilities + shareholders’ equity.”

- Trial balance is done by taking the end balances from general ledgers. A balance sheet is done by using the trial balance as a source.

- A trial balance is created to ensure the accuracy of financial affairs. A balance sheet is created to show the right picture of financial affairs to the stakeholders.

- The trial balance doesn’t need any sign from the auditor. But a balance sheet must be signed by the auditor.

- Trial balance is recorded every month, quarter, half-yearly, and annually. On the other hand, the balance sheet is prepared at the end of every financial year.

Trial Balance vs. Balance Sheet (Comparison Table)

Here is a quick comparison chart highlighting the Trial Balance vs. Balance Sheet differences.

| The basis for Comparison – Trial Balance vs. Balance Sheet | Trial Balance | Balance Sheet |

| 1. Inherent meaning | Trial balance is created to record all the balances of ledger accounts. | A balance sheet is created to see whether the assets equal liabilities plus equity. |

| 2. Application | Trial balance is used to see whether the total of debit balances equal credit balances. | The balance sheet is used to show the accuracy of the financial affairs of a company. |

| 3. Is it a financial statement? | No. | Yes. |

| 4. Division – Trial Balance vs. Balance Sheet | Every account is divided between debit and credit balances. | Every account is divided into assets, liabilities, and shareholders’ equity. |

| 5. Used for | Internal purpose. | External purpose. |

| 6. Recorded when? | Trial balance is recorded at the end of each month, quarter, half-year, and year. | The balance sheet is only recorded at the end of any financial year. |

| 7. Source | General ledger. | Trial Balance. |

| 8. Signature | The auditor doesn’t need to sign it. | The auditor needs to sign it. |

| 9. Rule of thumb – Trial Balance vs. Balance Sheet | There’s no rule of thumb in arranging ledger balances. | Assets, liabilities, and shareholders’ equity should be arranged in proper order. |

| 10. Part of the final accounts | Trial balance is not part of the final accounts. | The balance sheet is part of the final accounts. |

Conclusion

There are significant differences between the trial balance vs. the balance sheet. But trial balance and balance sheet are always connected. So even if the trial balance is prepared just for internal use and to see whether the transactions are accurately recorded, the balance sheet couldn’t be recorded properly without a trial balance.

Understanding the trial balance and balance sheet would be much easier if you understood debit, credit, journal, and ledger.

It’s all about understanding the fundamentals and applying them whenever required.

Recommended Articles

This has been a guide to Trial Balance vs. Balance Sheet. Here we discuss the top difference between trial balance and balance sheet, infographics, and a comparison table. You may also have a look at the following articles –