Part of our General Ledger guide

Bookkeeping Meaning

Bookkeeping is the day-to-day documentation of a company’s financial transactions. These transactions include purchases, sales, receipts, and payments. The details are entered in chronological order. Crucial investments, business operations, and financial decisions are made based on performance analysis reflected in these records.

There are two ways of bookkeeping, the single-entry system and the double-entry system. The double-entry system is used more commonly. These records are important for analyzing performance.

- Bookkeeping is the chronological recording of business sales, revenue, purchases, and expenses. This is done on an everyday basis. Entries are made into the company’s ledger.

- Bookkeepers are responsible for entering accounting details. They prepare their firms’ relevant financial statements.

- This documentation can be done via cash or accrual method; however, GAAP prefers that the companies prepare their financial statements on an accrual basis.

- While bookkeeping is a part of accounting, the latter is a more extensive concept. It includes interpreting the accounts prepared by the bookkeepers to derive conclusions and facilitate crucial decision-making.

Bookkeeping Explained

Bookkeeping is an essential process that involves the systematic creation of a company’s accounts ledger. Accountants, managers, directors, and shareholders get vital insights from ledgers. Also, when it comes to external parties like banks, investors, and associates, bookkeeping records are a source of reliable and comprehensive information. Decisions related to lending and business association are also made based on these records. Most firms prefer the double-entry bookkeeping system to record an equivalent credit for every debit aspect.

Bookkeepers are individuals who execute the task of writing down a firm’s financial transactions daily. Bookkeepers’ responsibilities include creating bank reconciliation statements, closing monthly ledger accounts, and preparing annual financial statements.

Even sole proprietary businesses and small firms such as local stores and dealers require bookkeeping for tracing expenses, revenue, sales, and purchases. Many small-scale enterprises nowadays use accounting software like “QuickBooks.” Small businesses prefer hiring bookkeepers over in-house accountants. That would be the cheaper option. Alternatively, they also outsource bookkeeping services to a professional accounting firm.

How To Do?

Bookkeepers must know which form of accounting method to opt for to ensure accuracy and reliability in the results obtained. Hence, they primarily use the following approaches:

- Cash Basis: Cash Basis is a method whereby only the financial transactions facilitated through money exchange can appear in the books. It ignores outstanding expenses and owed income.

- Accrual Basis: Accrual Basis is a more realistic approach for accounting. Therefore, it is mandated by GAAP. In the Accrual method, bookkeepers record the financial transactions immediately. Entries are made as soon as income or sales amount becomes due. Expenses or payments owed are also recorded instantaneously.

Types

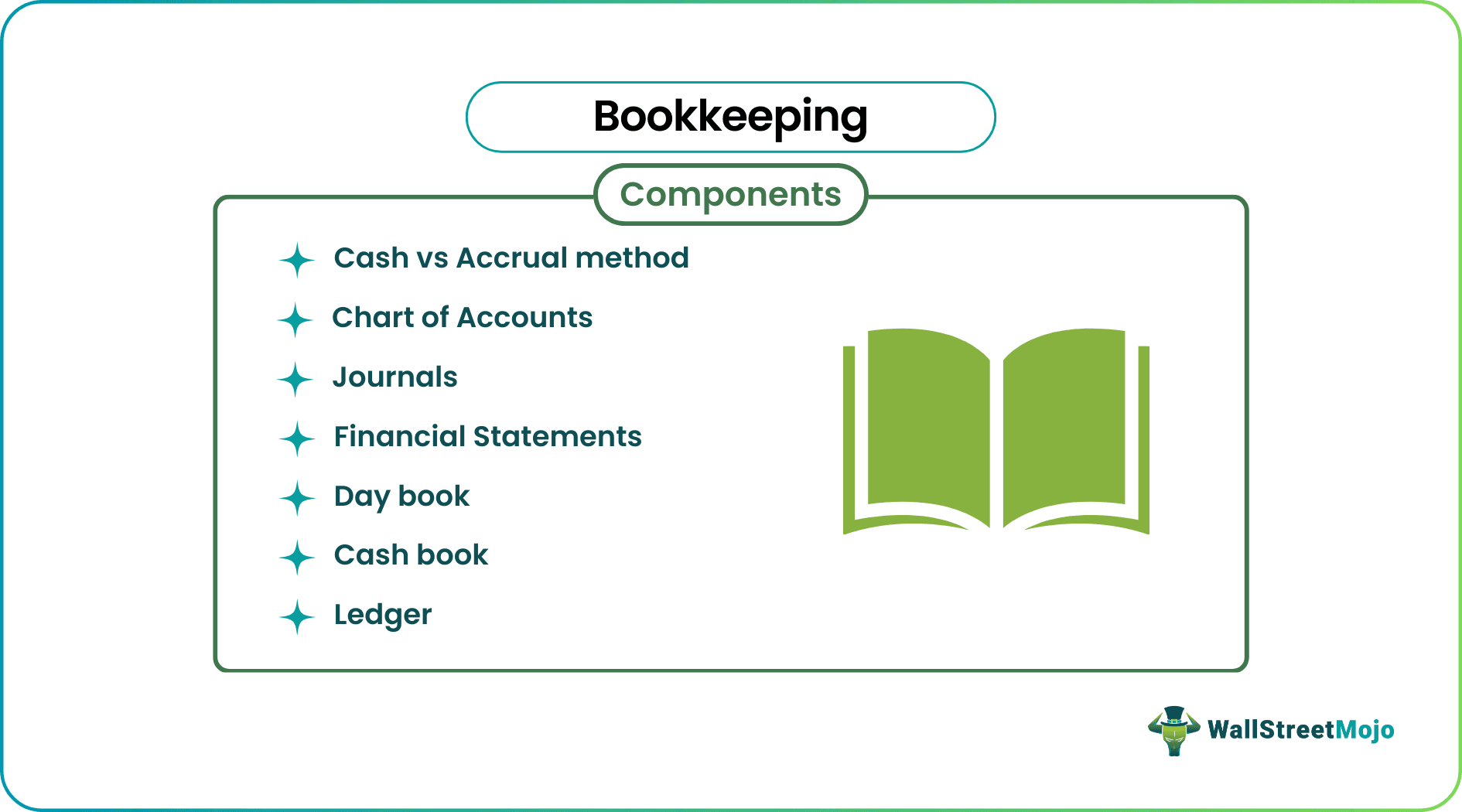

It is important to understand the components or types of bookkeeping that play a vital role in the bookkeeping procedure:

- Chart of Accounts: COA is a detailed worksheet containing guidelines and a framework for what kind of expense should go to which general ledger account. It helps bookkeepers pick the correct expense code while posting any journal entry.

- Journal: Journal entries primarily record the financial impact of any business transaction, where the debit equals credit aspect.

- Ledger: A ledger is the primary book of accounts that shows the debit and credit transactions related to one account. This is for a particular period and is recorded in a summarized format. It also contains the opening and closing balances by evaluating all the debits and credits of an account. It facilitates the creation of a Trial Balance.

- Cash Flow Statement: All the cash and cash equivalent changes from financing, investing, and operating activities are summarized in a cash flow statement.

- Income Statement: This is commonly known as a Profit and Loss Account. The income statement puts forward the net profit or net loss in a particular period.

- Balance Sheet: The balance sheet is the statement that shows a summary of shareholders’ equity, assets, and liabilities. The balance sheet summarizes data for a particular financial year. Therefore, it resembles the organization’s financial position.

Examples

Let us consider the following examples to understand how bookkeeping in accounting works:

Example 1

Every transaction comprises a debit and credit value to create an equilibrium. Only then can an entry be validated. This is why the double-entry accounting method is considered the best. In addition to that, bookkeepers should always stick to the following golden rules of accounting:

| Account Type | Any Increase | Any Decrease |

|---|---|---|

| Assets | Debit | Credit |

| Liabilities | Credit | Debit |

| Income | Credit | Debit |

| Expenses | Debit | Credit |

| Equity | Credit | Debit |

Example 2

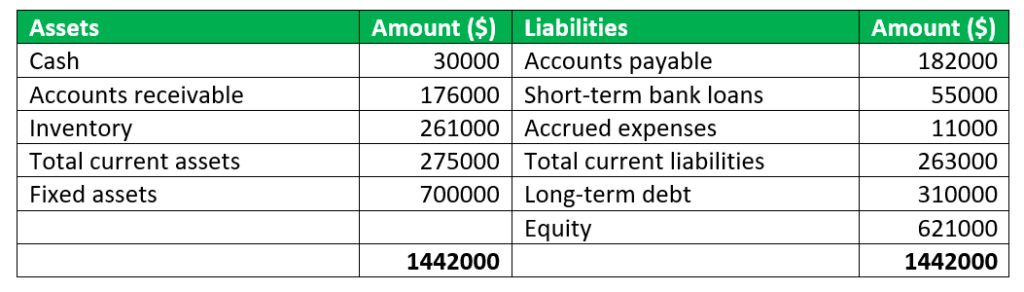

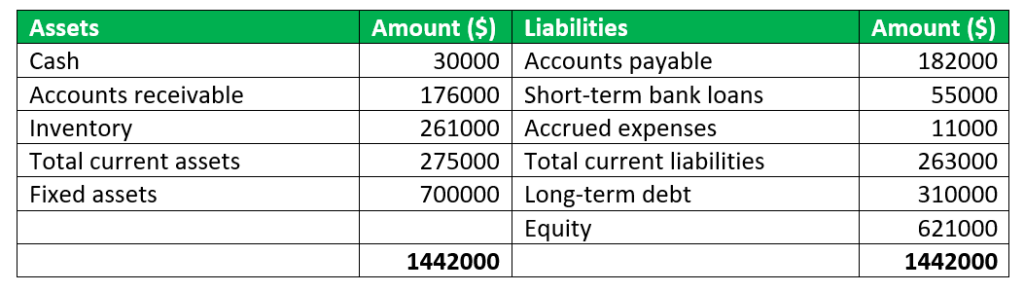

Given below is the balance sheet of the PQR enterprises:

Balance Sheet

For March 31, 2020

Following are the financial transactions for the financial year 2020-2021:

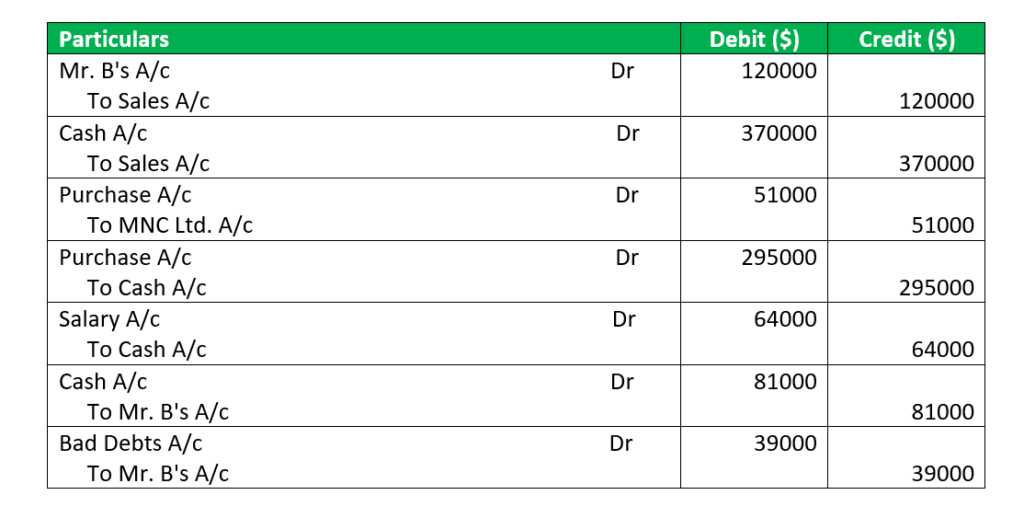

- Credit Sale to Mr. B of $120000

- Cash Sale of $370000

- Credit Purchase of $51000 from MNC Ltd.

- Cash Purchase of $295000

- Salary Paid: $64000

- Sales Amount Received: $81000

Additional information:

- Closing stock $313000

- Mr. B’s bad debts $39000

Bookkeepers prepared the following financial statements:

Journal Entries

For the year ending on March 31, 2021

Balance Sheet

For the year ending on March 31, 2021

Note:

Accounts payable = 182000 + 51000 (MNC Ltd.) = $233000

Equity = 621000 + 93000 (Net Profit) = $714000

The business realized it had made a profit of $93000 but was losing money to Mr. B (one of the debtors), i.e., bad debts of $39000. Therefore, the management decided not to provide goods on credit to Mr. B in the future.

The bookkeeping patterns of Amazon and Godaddy follow the accrual method of accounting. Therefore, their accounting periods coincide with the calendar year from the 1st of January to the 31st of December.

Advantages

Some of the advantages of bookkeeping services are as follows:

- Bookkeepers assist with financial analysis. Auditors and accountants can now easily extract, interpret, and access financial statements thanks to documentation.

- Bookkeepers adhere to accounting procedures and corporate laws. They ensure the legal viability of the business accounts.

- The documents related to financial information appear in chronological order, that is, in a date-wise sequence. This makes it convenient for the user to locate a particular transaction.

- Preparing an accounts ledger is quite easy, and standard formats for recording financial data are available.

- Bookkeeping is the primary process in accounting. It, therefore, paves the way for other accounting activities like summarizing, analyzing, and reporting a firm’s finances. It is a source of transparent, real-time financial information.

- Many operations like decision-making tax planning, bank financing, and loans rely on documented data.

- The financial statements prepared by bookkeepers can be used for comparative study. The system also provides all the payroll details and deductions made.

Disadvantages

Bookkeeping also has some flaws, which one must know of. Some of these include:

- Bookkeeping is still prone to human error. If a wrong entry is made in the journal, it will affect the final accounts. Thus, such faulty statements may mislead analysts and accountants.

- Bookkeepers add to the company’s costs on top of the high remuneration paid to accountants, which is why many businesses opt for outsourced accounting & bookkeeping services as a more cost-effective solution.It is a form of non-operating expense for organizations.

- Bookkeepers can deceive their employers by engaging in forgery or fraudulent practices. They can even tamper with financial statements or crucial information to take advantage of their firms.

- Financial software is often more feasible and faster than hiring bookkeepers.

Bookkeeping Vs Accounting

Though the terms refer to processes that lead to achieving the same objective, they differ widely in terms of how they are maintained and used. Some of the differences between bookkeeping and accounting are as follows:

| Category | Bookkeeping | Accounting |

|---|---|---|

| Foundation | It is the basic method of maintaining daily records. | It is a complete process of recording, interpreting, and analyzing the performance of a company through its financial records. |

| System | It is part of the whole accounting process. | It is a complete process of recording, interpreting, and analyzing performance of a company through its financial records. |

| Objective | Provide data for accounting. | Prepare financial statements for performance analysis |

Frequently Asked Questions (FAQs)

What is bookkeeping?

It is the method of documenting the daily financial transactions of an organization. Ledger entries are made in the order of their occurrence. Additionally, bookkeepers reconcile bank records and report employers’ financial information in an organized format.

What is the difference between accounting and bookkeeping?

Accounting is a broader phenomenon; bookkeeping is just a small part of the accounting system. Accounting comprises organizing, recording, classifying, summarizing, and reporting business transactions. In comparison, bookkeeping is limited to recording and organizing financial information.

What do you need to be a bookkeeper?

Bookkeepers need not be highly qualified; instead, individuals can start documenting immediately after passing high school. However, to gain specialization, bookkeepers can get a certification or diploma. Some go as far as an associate’s or bachelor’s degree in accounting to stand out. Additional certification does result in higher remuneration.

Recommended Articles

This article is a guide to Bookkeeping and its Meaning. We explain the differences with accounting, its examples, how to do it, types, and advantages. You can learn more about financing from the following articles –