Part of our Accounting Concepts guide

Double Entry Accounting System Definition

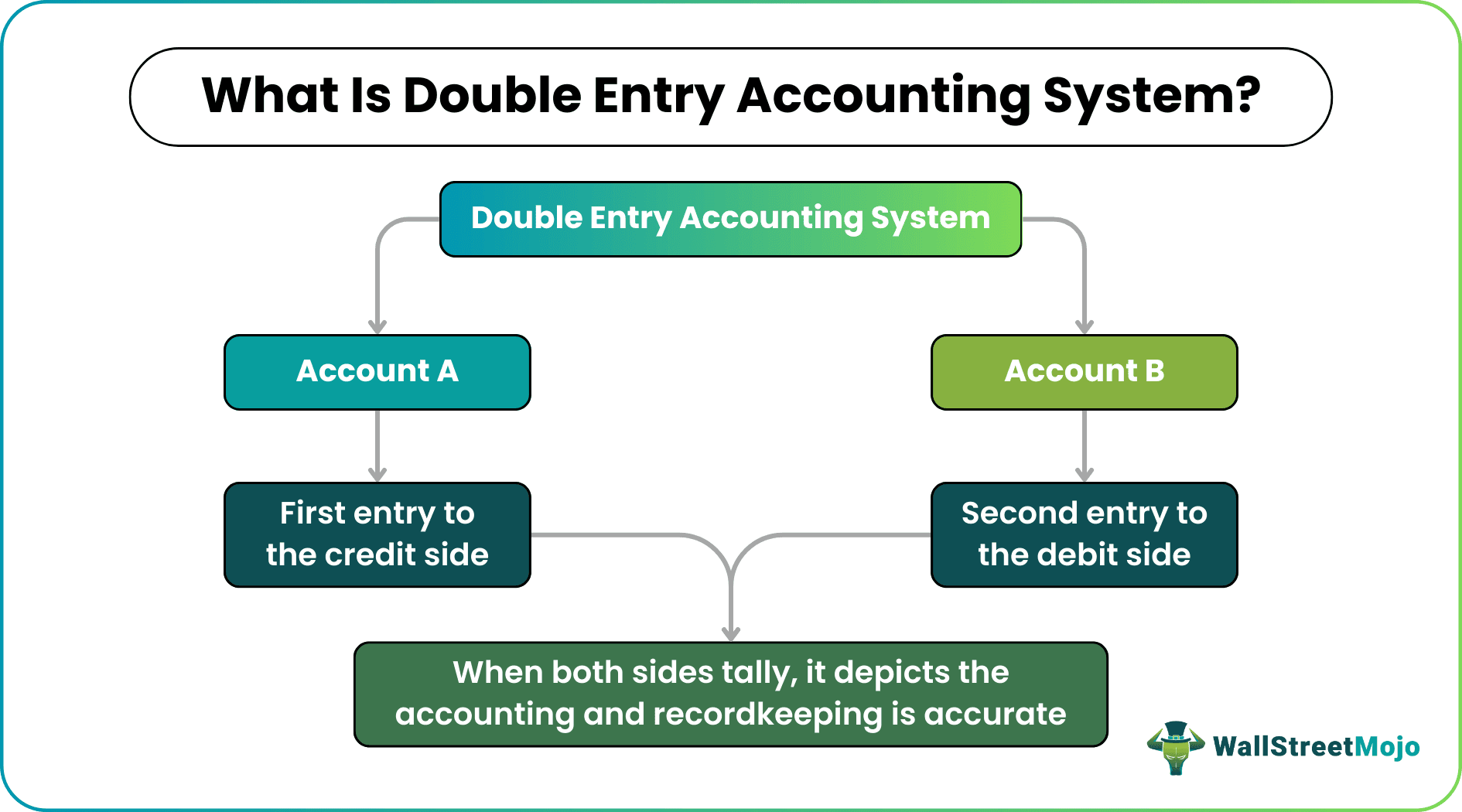

A double entry accounting system refers to the bookkeeping method where two entries are made simultaneously into two different accounts, indicating a firm’s cash inflow and outflow. The purpose is to tally both the accounts and balance the credit and the debit side. This accounting system helps organizations assess their overall performance in a financial year.

It is different from the single entry accounting system, which involves filling in the information in only one account. Only a single entry recording the income and expenses in a cash register helps maintain the financial information to enable businesses to assess their position.

- A double entry accounting system refers to the bookkeeping process in which two entries are made simultaneously in two different accounts to ensure that the credit and debit sides tally.

- It works on the principle that states the company’s financial scenario is efficient if the debit entries and credit entries remain balanced at any given point in time.

- Every credit entry should have an equal and consecutive debit entry.

- A mismatch of credit and debit sides at any point in time will mean accounting error, which could be easily rectified when the method of accounting used is double entry.

How Does The Double Entry Accounting System Work?

The double entry bookkeeping was introduced between the 13th and 14th centuries, and one of its first mentions is found in Luca Pacioli’s book, published in 1494. He was well-known as the Father of Accounting, and he explained the double entry accounting method in detail to readers.

The double entry accounting system means keeping the transactions in order. It operates on the principle that every transaction in one account has an equal and opposite entry in the other. For example, every amount credited in one account will be a debit record for another. A bookkeeper makes the same entry in two places to reflect two different transaction scenarios. Hence, it is named a double entry bookkeeping system.

The Chart of Accounts, which remains up to date, becomes one of the best sources for accounting professionals to find the breakdown of the transactions and crosscheck the double entries made on the accounts’ credit and debit sides, respectively. Making a dual entry in two different accounts involved in the transaction indicates the net effect of that transaction.

For example, when people buy something, it becomes a debit from their pocket or bank account, but the product goes into their credit record as they receive it in return. Similarly, the shopkeeper records the amount on the credit side, and the product taken out of the inventory becomes a debit record.

Video Explanation of Double Entry Accounting System

Rules

In a double entry accounting system, the total volume of assets must balance with the total number of liabilities and shareholders’ equity a company has at a given point in time.

Thus, the accounting equation of double entry bookkeeping system can also be expressed as:

Total Assets=Total Liabilities+Total Equity

This accounting method works on certain rules or principles, which every accounting professional knows about and users are expected to be aware of. When double entry bookkeeping is done, the following things should be taken into account and crosschecked for accuracy:

- The credit side is to the right, and the debit side is to the left.

- Every debit record has a similar credit entry.

- Debit is the beneficiary; credit is the one who gives benefits.

- In the case of personal accounts, the giver is credited, the receiver is debited.

- The expenses are recorded as a debit for a nominal account, and income is the credit entry.

- In the case of the real account, inflows are debit, and outflows are credit.

Advantages

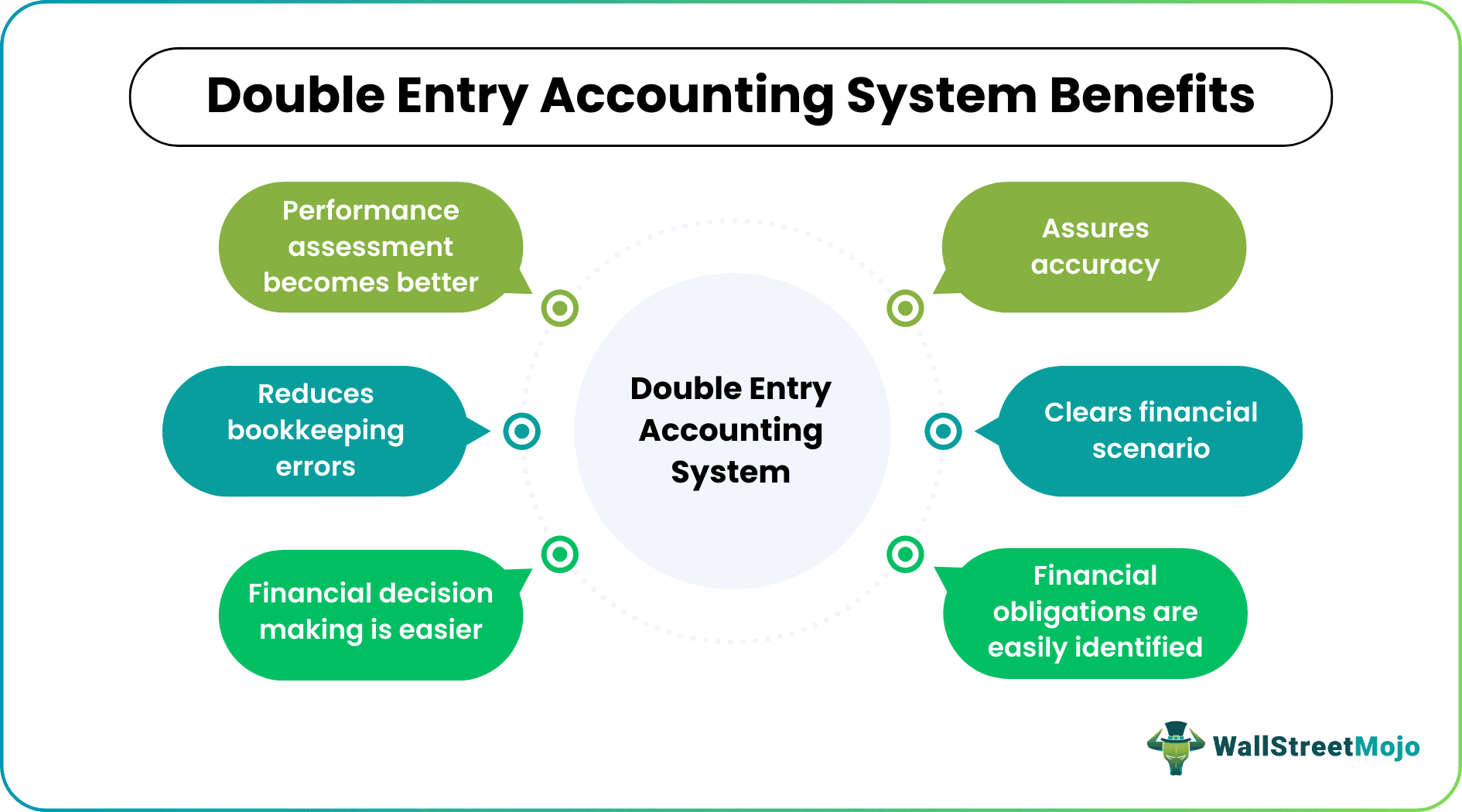

The double entry accounting method offers a number of benefits to organizations adopting it all in terms of accuracy, systematic organization, and better performance monitoring.

Some of the advantages of the double entry accounting system are as follows:

- When the credit and debit sides tally, it ensures that the recordkeeping is up to the mark.

- If there is a mismatch in the records, it is quick enough for accounting professionals to identify errors and rectify the same.

- This accounting system sets the recordkeeping standards for all financial firms and industries.

- There is a unique reporting structure, and, therefore, the records remain well-organized.

- All similar types of information are put together, making it easier for people to create a balance sheet.

- As the liabilities are well mentioned, it is easier to identify the financial obligations.

- When the overall financial scenario is crystal clear, making financial decisions is easier as decision-makers remain well informed.

Example

Let us consider the following example to understand the double entry bookkeeping process:

Dan booked an office table for his new set up at $2,000. He paid $1,000 in advance, and $1,000 was due upon delivery after the table was ready. Here is how the entries were posted in the double entry system of accounting on that particular date:

The first case denotes a debit record and a corresponding credit, indicating a net effect, which comes to zero. Although three accounts were given effect in the second case, the net entry between debit and credit is 0. Hence, the double-entry system of accounting suggests that every debit should have a corresponding credit.

When Dan booked his office table, he paid only $1,000. As a result, the unpaid amount for the day becomes accrued in Accounts Payable A/c (which means it is supposed to be paid later).

On delivery of the table, the payment is made, and the effect of entries looks like this:

Single Entry Accounting vs Double Entry Accounting System

Recordkeeping is handled as single entry accounting and double entry accounting. The former deals with making a one-time entry into an account, be it an expense or income. On the contrary, the latter is about making two entries simultaneously to two different accounts and marking both the debit and credit sides.

The double entry system is more organized and helps assess the overall financial scenario of a company. Hence, the tax authorities trust and accept the method for tax purposes. However, a single entry accounting method is less trusted and not acceptable for tax computation by the authorities.

With single entries, fraudulent activities become common, and tampering with the record is usual for companies. On the other hand, it’s easy to track accounting errors and issues in a double-entry bookkeeping system when the credit and debit sides don’t tally.

The single entry accounting system is suitable and could be recommended for only small businesses, while the other one is suitable for companies of all types and sizes.

Frequently Asked Questions (FAQs)

1. What is a double entry accounting system?

A double entry system of accounting is a bookkeeping process where there is an equal and opposite entry made in two different accounts simultaneously. The debit and credit sides are recoded simultaneously to be tallied for accuracy when required. Any mismatch, if identified, will indicate a bookkeeping error, which could easily be rectified as the records are organized in a proper pattern.

2. Who introduced the double entry system of accounting?

Luca Pacioli introduced the concept of double entry accounting somewhere between the 13th and 14th centuries through his book published in 1494.

3. How are the double entry accounting system and the duality concept related?

In accounting, the duality concept, also known as the dual aspect concept, refers to how each transaction made affects a business in two aspects. This effect tends to be equal and opposite. The double entry accounting method is based on this concept of duality.

Recommended Articles

This article is a guide to what is Double Entry Accounting System and what it means in bookkeeping. Here we explain its rules & advantages along with examples. You may also learn more about basic accounting from the following recommended articles –