Part of our Accounts Receivable guide

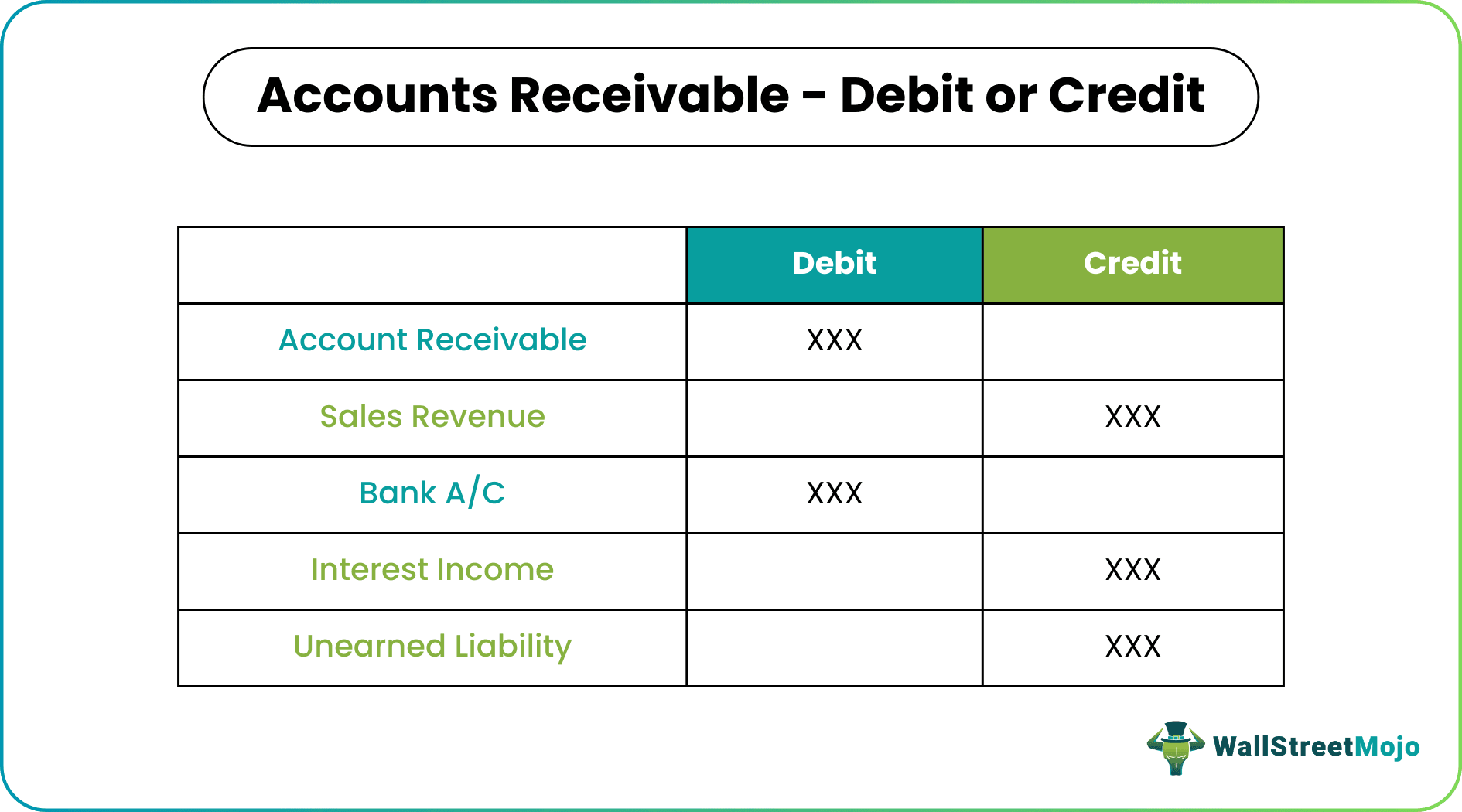

Is Accounts Receivable Debit or Credit?

Account receivables are the cash inflows that the creditor will receive based on the credit period given to the customers as per the prevailing market trend. As per the golden rules of accounting, debitmeans assets, and credit means liabilities. Account receivables represent transaction exposure in the form of cash inflow shortly. The same shows that an entity will benefit from this exposure directly or indirectly. Hence, whether accounts receivables debit or credit is very simple, one can conclude that account receivable should be debited and visible on the asset side.

- Account receivables refer to the cash inflows the creditor obtains according to the prevailing market trend.

- Account receivables show transaction exposure in cash inflow.

- It also displays that an entity benefits from the exposure directly or indirectly.

- In IFRS 15, from January 1, 2018, detailed guidelines are provided to know account receivables and whether the same is debited or credited. Generally, an account receivable is debited if regarded as an invoice post-issuance. Therefore, it must be credited if it concerns the customer’s advance receipt.

Treatment of Account Receivables as Debits or Credits Under IFRS

From January 1, 2018, in IFRS 15, detailed guidelines have been given to recognize account receivables and when the same is needed to be debited or credited.

As per standard, account receivable – credit or debit can be recognized as revenue on the satisfaction on any of the following particulars:

- The customer receives and consumes the benefit provided by the entity as the entity performs at the same time;

- The entity’s performance gives betterment to an asset that the customer controls as the asset is getting developed/supplied.

- The entity creates such a product/provides such a service that has no alternative use, and the entity has an enforceable right to receive consideration for the completed performance.

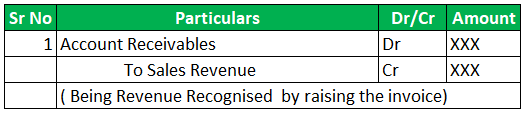

If any of the above conditions are met, the following entry is to be passed:

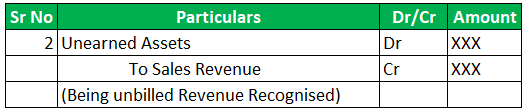

The above account receivables will be disclosed as If an invoice is raised, the above account receivables will be disclosed as Trade receivables under current assets. However, if it is not invoiced, then the same will be disclosed as “Unearned Assets “along with invoiced trade receivables.

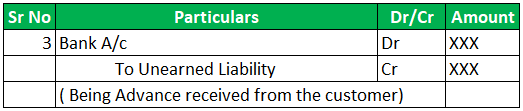

In case of advance receipt from the customers, the standard gives guidance to follow one step ahead of the routine accounting treatment. Standard describes that if there is a significant time gap of more than one year between the advance receipt and the transfer of goods/service provision, there is a loan component in that advance receipt. Otherwise, they will be directly recorded as a liability by crediting it.

Thus, if a creditor receives an advance and the time gap is less than one year, the following accounting entry will be passed.

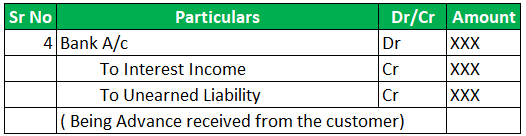

However, if the time gap exceeds one year, the entity will have to identify the interest component and pass the following account entry.

Account receivables post raising of invoices.

Generally, the business will supply the first products/services to the customer. On completing the commitment, the invoice will be issued, and accordingly, cash flow will take place. In this process, if the customer makes payment based on the issue of the invoice, then the figure for trade receivables will always be positive. An entity can receive a specified amount on completing the specified period.

Thus, whenever account receivable figures are accounted for post-completion of obligations, they will be on the debit side and should be parked under the asset side of the balance sheet

Accounts Receivables in case of Advance Payment

In a specific business, the customer always needs to make the advance payment to initiate the supply of products or services. For example, in the telecom industry, customers are purchasing prepaid cards. In such a scenario, they will not raise invoices at the time of receipt of payment.

- The first payment will be received, then products/services will be supplied, and then invoices will be issued.

- In this case, account receivable figures will show a negative figure. It will directly obligate the entity to provide the committed obligations within a fixed period and under specified terms and conditions.

- Such advance payment will be credited as this will be linked with the services/obligations with creditors.

Thus, from the above discussion, it is clear that account receivables post raising of invoices will be debited to Sales Revenue[/wsm-tooltip, and hence will be visible under asset side, under current assets. However, if an amount has been received as an advance before completing a performance obligation, such account receivable will be considered a liability. Therefore, it will be credited to the bank account and disclosed under the liability side, under [wsm-tooltip header=”Current Liability” description=”Current Liabilities are the payables which are likely to settled within twelve months of reporting. They’re usually salaries payable, expense payable, short term loans etc.” url=”https://www.wallstreetmojo.com/current-liabilities/”]current liability.

Conclusion

In the current scenario, account receivable holds one of the most important positions as it is an essential component of current assets. In the past, major scams have taken place by manipulating the accounts receivables, and thus, it is crucial to ensure the proper disclosure of the same. From the above discussion, it can be understood that account receivable generally will be debited if it is to be considered post-issuance of the invoice. However, if it concerns the advance receipt from the customer, it is needed to be credited. Professionals will be needed to use their judgment to identify whether any significant financing portion exists or not in unearned recording liability.

Frequently Asked Questions (FAQs)

Does accounts receivable have a debit or credit balance?

On a balance sheet, accounts receivable are said to be an asset. Therefore, it is a debit balance because its money due will be received soon and benefit from when it arrives.

Should accounts receivable be negative?

Receivables can be either positive or negative. If the result is affirmative, the money belongs to the business. If it’s negative, on the other hand, the business is owing. When a company owes its debtors more money than it has in cash on hand, this situation is referred to as having negative accounts receivable.

How accounts receivable works?

Accounts receivables (AR) are amounts owed to a business for goods or services provided or consumed but not yet paid for by clients. The balance sheet classifies accounts receivable as a current asset. Hence, any sum clients owe for purchases they made on credit is considered AR.

When accounts receivable are collected?

Accounts receivable collections are for earning money from the current customers by collecting what they owe. Major companies collect in 30 days or at least 90 days. In addition, it becomes easier for the company to pay its debts by collecting customers’ money.

Recommended Articles

This article has been a guide to Accounts Receivable – Debit or Credit. Here we discuss IFRS treatment of accounts receivables along with examples & explanations. You may learn more about accounting from the following articles –