Part of our Accounts Receivable guide

What Is Invoice Financing?

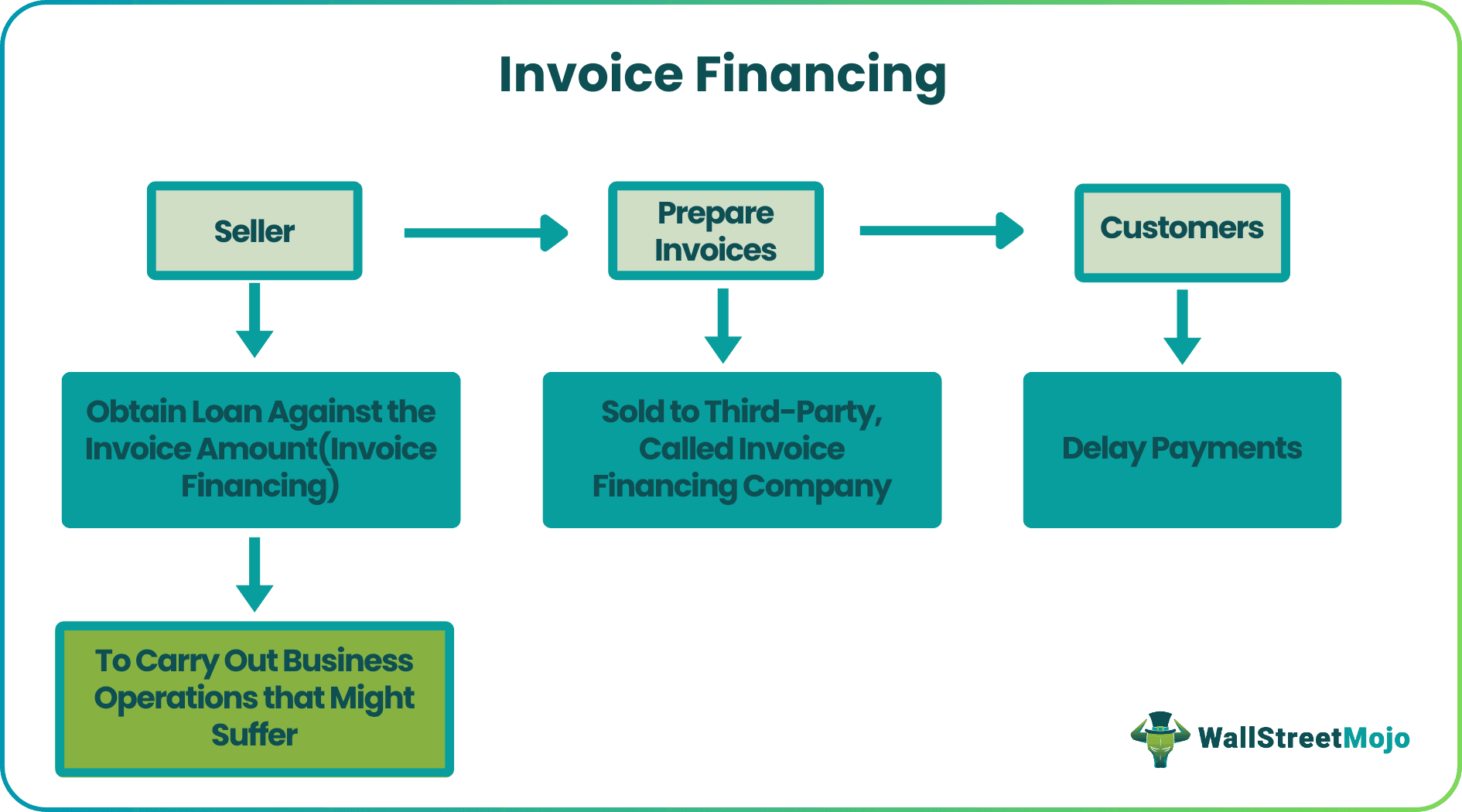

Invoice financing is the process through which a firm obtains immediate funds from a third party against the outstanding payments from customers for the goods and services sold. This provision of borrowing money helps companies make pending payments to suppliers and employees without any delay.

Firms can borrow finances by showing the invoices to the invoice financing companies and paying a portion of the invoice amount as a fee to them. In short, invoice financing helps companies not to hold further operations due to a lack of funds when the payment is stuck with customers. Instead, they can keep using the funds coming from the account receivables.

- Invoice financing is financing the short-term liquidity needs of a company using its outstanding invoice dues, also called receivables.

- Invoice discounting and invoice factoring are two types of receivables financing available to firms.

- It can lower the time spent on the administration if the lender takes control of collecting the receivables.

- There is no specific formula to decide which invoice financing a company should use. It all depends on the kind of needs and the position of the company to fund its working capital needs.

How Does Invoice Financing Work?

Invoice financing, also referred to as accounts receivables financing or receivables financing, lets companies arrange for funds when customers are yet to pay or fail to pay on time. While customers have the option to delay the payment, firms that sell goods and services to them cannot postpone the business operations as it would delay the supply of products, hampering their market image. Obtaining funds from these financing options helps them tackle delays in payments from the customer end.

Invoice financing for small businesses is quite effective as they might need funds when a huge amount of money is stuck with customers. When the sellers sell goods and services to people, they generate an invoice to mention the outstanding amount payable by customers. The payments might get delayed, which, in turn, could hugely affect the business operations, affecting the demand and supply network adversely. Receivables financing, in such a scenario, allows firms to borrow money from third-party entities against the invoice amount.

The sellers pay the third-party entities a commission, a percentage of the invoice amount. They buy the invoice and give the former the required amount to continue business operations until the payments are received.

However, there are certain factors that these third-party firms consider before approving the finances. These determinants include the company size, past track record, quality of clients with receivables, invoice practices, and financial stability and strength.

Types

Invoice financing comes in two forms – invoice factoring and invoice discounting.

1. Invoice Factoring

The method uses short-term money by pledging its receivables to a lender. Here, the lender is responsible for collecting the payments from the business’ customers.

As the lender is responsible for collecting the payments, the fees charged for this financing are slightly more. The fees also include the due diligence charges that the lender charges to measure the creditworthiness of the customers. Moreover, the customers need to know that their payments will be collected by a third-party lender, not the company that lends its products/services to its customers. However, the involvement of a third party in the collection might hamper the relationship between the seller and its customers.

2. Invoice Discounting

Another one is invoice discounting, where the company which needs the money can retain the right to collect the dues while receiving the money by showing their invoice dues. As the collection right is still with the company, the fees charged to fund its short-term liquidity needs are slightly lower than invoice factoring. There is no due diligence charge here because the process of collecting money still lies with the company. Though the lender checks the clients’ creditworthiness, the transaction happens majorly on the company’s reputation and financial strength.

Examples

Let us consider the two scenarios to understand the invoice financing meaning:

Scenario #1 – Invoice Factoring

Suppose company A has receivables of $5000, which is due in 90 days from the customers. Thus, it goes to financial institution B for immediate invoice financing rather than waiting for so long. B checks the creditworthiness of A’s customers, and with due diligence, it decides to lend 85% of the requirement, accounting for $4250.

Once B collects the entire $5000 from A’s customers, it pays back the remaining 15% after its fee deduction. Therefore, B returns $550 to A and gets $200 as fees. In contrast, A gets to fund its working capital needs quickly without having to wait for its customers to pay them.

Scenario #2 – Invoice Discounting

Company A, with receivables worth $5000 due in 45 days, needs quick money to fund its employees’ salaries. It goes to bank B and asks for invoice financing after showing its receivables invoices. It agrees to pay a fee of 3% to B. The latter lend 80% of the total receivables, i.e., $4000 to A, which it uses to fund its needs immediately. A’s customers pay back their dues of $5,000. A sends $4,150 to B and keeps the remaining with them. So overall, B gets its own money back and 3% of fees on $5,000, which is $150. Businesses seeking efficient ways to manage invoice transactions often benefit from custom solutions tailored to their needs. A custom commercial invoice template by Invoice Simple can be an excellent resource for organizations looking to streamline their invoicing process, accurately reflect the terms of trade, and enhance the financing options available to them throughout different scenarios. Utilizing such templates not only aids in maintaining organized financial records but also supports transparent communication between companies and financing institutions.

Invoice Financing vs Factoring

The comparison between factoring and invoice financing results in the comparison of invoice factoring and invoice discounting, which is also a part of receivables financing. While differentiating the two terms, the latter is considered synonymous to invoice discounting. Here are the differences between the two:

| Category | Invoice Financing | Invoice Factoring |

|---|---|---|

| Ownership | Same as invoice discounting, where the companies themselves retain the invoices | The buyer, i.e., the third party involved in providing finance, becomes the invoice owner. |

| Collection | Companies collect the pending payments | The third-party firms collect the payment from the customers as owners. |

| Process | The invoice amount backs the loan received. | The factoring company buys the invoice at a discount and then pays an upfront fee to the selling firms. |

Frequently Asked Questions (FAQs)

How much does invoice financing cost?

The cost of financing varies widely. It is determined based on various factors, including the invoice amount, the creditworthiness of the firms, the days financed, the relationship shared between the parties involved, etc. The third-party entities decide on the receivables financing fee depending on the parameters.

Is invoice financing a good idea?

Yes, opting for this kind of financing is a good idea. For example, there are times when delayed customer payments put business operations on hold, thereby affecting the production of goods and services. When such a financing option exists, companies can prepare an invoice and borrow the required amount against the value from a third-party entity. In short, the invoiced amount backs the loan to be taken. As a result, all functions are smoothly carried out without interruption.

How does one account for invoice financing?

It is the method of accounting that helps businesses obtain finances against their accounts receivables. It helps generate immediate cash flow for businesses, so they do not run short of funds while customers delay paying them for the goods bought. However, once the customers pay them, they can repay the third-party firms with interest.

Recommended Articles

This has been a guide to What is Invoice Financing & its meaning. We explain how it works, its types, examples, & comparison with factoring. You can learn more about financing from the following articles –

- Pro Forma Invoice – Meaning

- Vendor Financing Example

- In House Financing Example

- Blank Invoice Template in Excel

- Shrinkage Formula

Recommended Articles

Continue with these closely related articles from the same guide.