What is Allowance For Doubtful Accounts?

Allowance for doubtful accounts primarily means creating an allowance for the estimated part of the accounts that may be uncollectible and may become bad debt and is shown as a contra asset account that reduces the gross receivables on the balance sheet to reflect the net amount that is expected to be paid.

While thinking about what would await shortly, a business must be pragmatic. It has to think about how much they would be paid and never receive it. . If a company starts thinking about the bad debts way too late, it wouldn’t be possible for the company to prepare for it immediately. So, an estimated figure for what may not be received is decided in advance.

- The allowance for doubtful accounts, shown as a contra asset account on the balance sheet and represents the estimated portion of the accounts that may be uncollectible and turn into bad debt, is subtracted from the gross receivables to reflect the net amount that is anticipated to be paid.

- Since bad debt is an expense, we debited the account in the first entry. According to accounting principles, when an expense rises, we debit that account, which is why bad debt gets debited.

- The balance sheet is the only one the second and third journal entries will impact. To do this, we first subtract the amount of the provision from the accounts receivables, and then if any money is collected, we add it back.

- It is one of the typical strategies used by businesses. They observe each of their clients. The company then assigns them a score based on their solvency. The consumers with higher scores are added, and the business calculates how much reserve it should have for potential bad debts.

How To Calculate?

Here are the three methods that organizations use to estimate the allowance for doubtful debts.

- Risk Score: This is one of the common methods companies use. They look at each of their customers. Then as per their solvency, the company assigns them a score. The customers who have higher scores are added, and then the company gets an estimate of how much allowance a company needs to keep for possible bad debts. This method may not be the most accurate one, but it works for most companies.

- Historical percentage – This is another method that organizations use a lot. By using this method, an organization looks at the past results. They look at the past results and determine what percentage of bad debts happened in the past year. They go with the same percentage for the present year as well. It may sound like a simple act, but it’s not a suitable method if you’re looking for accuracy.

- Pareto Analysis -This is, by far, the best method to use while estimating the allowance for bad debts. Italian economist Pareto said that you would get 80% of results from only 20% of your activity. By using the same principle, the organizations calculate their allowance. Here’s how it works. If the total credit sales is of $100,000, then the allowance for doubtful debts would be (as per Pareto principle) = ($100,000 *20%) = $20,000. But this method can be a broad estimation. To become more accurate about how many provisions we should create, we can use double Pareto. We need to use the Pareto principle twice. Extending the above example, if we use 20% of the previous 20% (i.e., 4%), we will get an accurate picture. It means the allowance for doubtful debts account would be $4000, to be precise.

One way to figure out whether one has estimated sufficient balance for the allowance for doubtful debts is to look at the account balance of the doubtful accounts. One would get a solid percentage by looking at the doubtful accounting balance and comparing the whole account balances of the doubtful accounts with the full credit amount and would also understand whether the allowance you estimated is sufficient or not.

Allowance for Doubtful Accounts Video Explanation

Examples

Let us understand the concept of allowance for doubtful accounts with the help of a couple of examples.

Example #1

ABC Company sells raw materials worth $100,000 to its various clients. Even though most of their clients make timely payments, one of their clients does not reply to emails or return calls.

Their payments have been overdue for more than 40 days and ABC’s management was not sure if the payment will ever be made. Therefore, they create an allowance for doubtful accounts in their balance sheet if this client does not make the payment.

Example #2

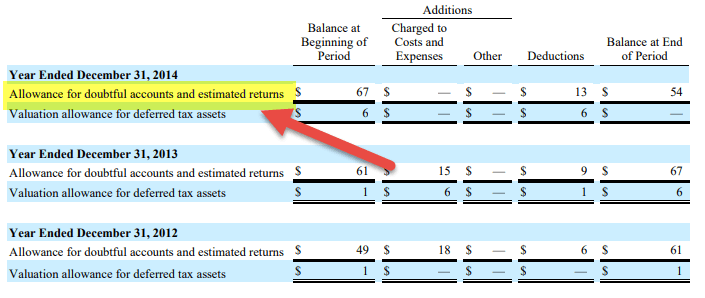

Below is the balance sheet of Colgate, through which we shall understand how major corporate companies curate an allowance for doubtful accounts balance sheet.

source: Colgate SEC Filings

We note that accounts receivables are reported net allowances for doubtful accounts. For example, Colgate reports allowances for doubtful accounts as $54 million and $67 million in 2014 and 2013.

Journal Entries

In this section, we will take a simple example and then illustrate how you should pass accounting journal entries for the allowance for doubtful accounts.

We will take an example of an accrual accounting basis.

Journal Entries # 1

Let’s say that Rough Jeans Ltd. has estimated that the allowance for estimated debts would be around $200,000 for the year. So, based on accrual accounting, we need to pass an entry stating that there can be bad debts shortly.

The journal entry would be –

| Particulars | Debit | Credit |

|---|---|---|

| Bad Debts A/C……………………… Dr | $200,000 | |

| To Allowance for Doubtful accounts Debts A/C | $200,000 |

In the first entry, we debited bad debt account because bad debt is an expense. As per the rule of accounting, if an expense increases, we debit that account; that’s why bad debt is debited. And similarly, we follow the same accounting rule here by crediting the allowance for doubtful debts account. Since they are provisioned and are used as counter-asset, we will credit it.

If the ]credit sales are $10 million, then by recording this entry, we’re offsetting bad debt from the credit sales already.

Journal Entries # 2

Now, let’s say that the company has got the actual figure, and it has seen that $120,000 is bad debt. So, what would be the new entry in this case?

We will pass the following entry –

| Particulars | Debit | Credit |

|---|---|---|

| Allowance for doubtful accounts debts A/C………. Dr | $120,000 | |

| To Accounts Receivables A/C | $120,000 |

In this entry, we are debiting allowance for doubtful debts because, by this amount, the counter-asset has been reduced, and we’re crediting accounts receivables to reduce the outstanding accounts receivables by $120,000.

Journal Entries # 3

Now let’s say that the company has asked a collection agency to try out to recover the bad debts. And they could successfully collect $40,000. So we need to pass another entry to recognize the collection.

We will reverse the previous entry as now there are chances of getting $40,000 as outstanding accounts receivables.

| Particulars | Debit | Credit |

|---|---|---|

| Accounts Receivables A/C…………Dr | $40,000 | |

| To Allowance for doubtful accounts debts A/C | $40,000 |

Effect on Income Statement and Balance Sheet

- The first journal entry above would affect the income statementwhere we need to pass the entrance of the bad debt and the allowance for doubtful debts account.

- And the second and third journal entries will only affect the balance sheet, where we will first deduct the amount of provision from the accounts receivables, and if any amount is collected, we will add that amount back.

Frequently Asked Questions (FAQs)

Are shaky accounts an asset or a liability?

Because it lowers the value of an asset—in this case, the accounts receivable—the allowance for dubious accounts is referred to as a “contra asset.” The allowance, also known as a bad debt reserve, is management’s projection of the number of accounts receivable that customers will not pay.

What distinguishes a dubious account from a bad debt?

A bad debt is an identifiable account receivable that won’t be paid and should be immediately written off. In contrast, a questionable debt could turn bad in the future, so it could be essential to set aside money for shady accounts.

What does “contra account” mean?

An account that lowers the value of a connected account is known as a contra account in a general ledger. They can be used to report a decrease or write down in a different contra account that nets the current book value while maintaining the historical value in the main account.

Recommended Articles

This article has been a guide to what is an allowance for doubtful accounts. Here we explain the journal entries, how to calculate, and examples. You may also have a look at the following recommended articles to learn more about accounting –