Part of our Accounts Receivable guide

What is Accounts Receivable Process?

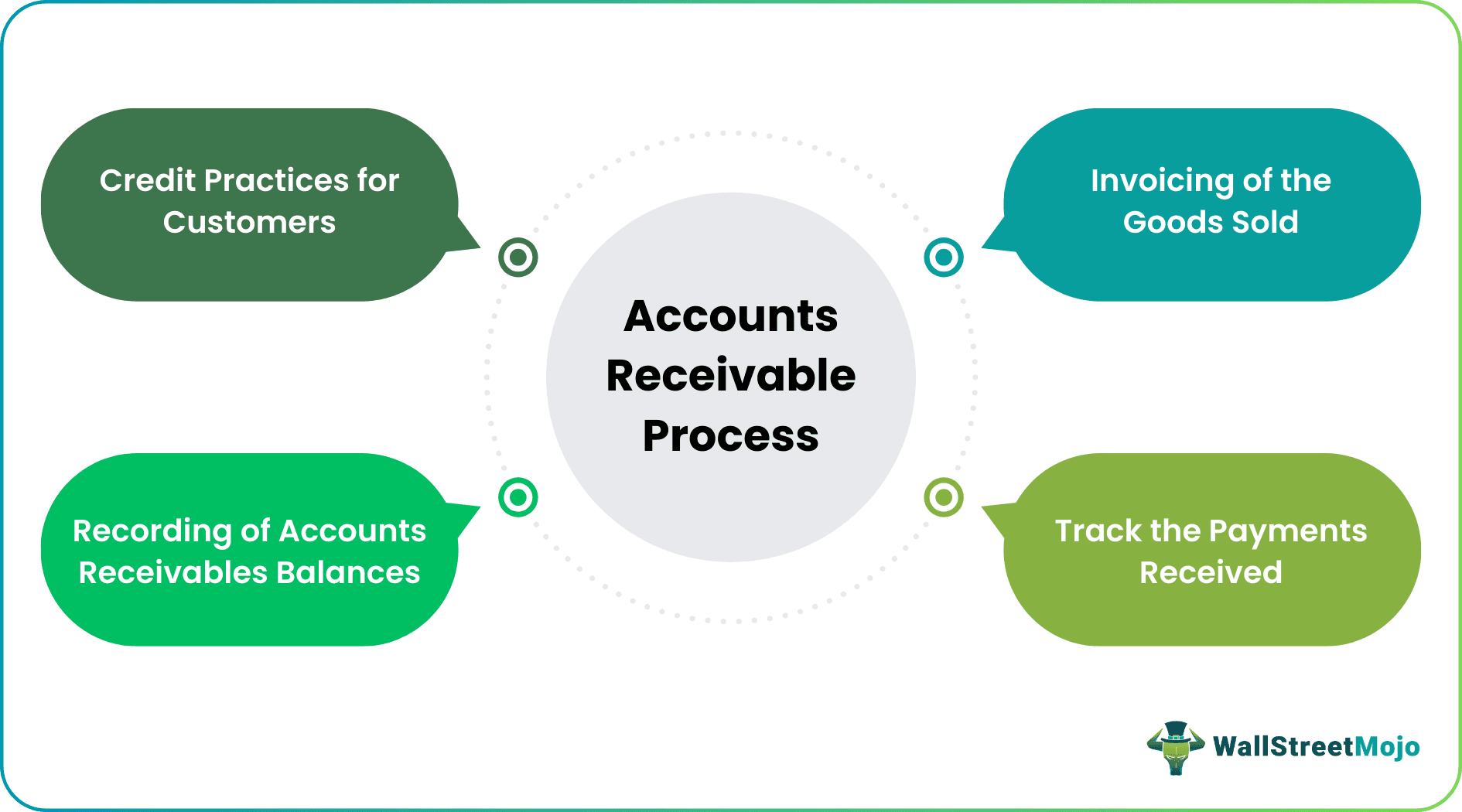

Accounts Receivable Process refers to the four-step procedure that a company must follow for accurate recording and maintenance of accounts receivable data. It starts with the company deciding its credit practices for customers, invoicing of the goods sold to them, tracking the payments received and yet to be received and end with the recording of the accounts receivable balance.

Accounts receivable is a type of account representing an amount receivable by the organization from their customers. Organizations can be engaged in the supply of goods or services. The consideration for such supply may either be received at the time of the transaction or sometimes at a later date.

- Accounts Receivable processes typically involve four steps: deciding on the company’s credit policies for customers; billing the customers for the goods sold to them; tracking payments made and still owed; and finally, recording the balances of the company’s accounts receivables by the accounts department.

- Accounts Receivable is an account that represents money owed to the company by clients. The provision of goods or services is a possible activity for organizations.

- When the customer’s payment is received, the transaction is over. Companies typically make supply on credit based on industry trends. As a result, businesses are required by accounting standards to record such recoverable payments as accounts receivable.

- As the business sells its account receivable to a third party at a discount and receives immediate cash, factoring services might be employed when there is a need for rapid cash.

How Does the Accounts Receivable Process Work?

The accounts receivable process is a cycle that identifies different steps of accounting for the amount that a business is to receive for the products and services sold. When customers buy goods and services from a business, its accounts department records the amount to track what they have received and what is still left.

The customer may pay for the items instantly or may fix a later date to make the payment. Where the consideration is received later, which is between supply and payment, such amount is shown by the organization as accounts receivable (AR). It forms part of the company’s assets and is generally classified under current assets.

If the company has an efficient accounts receivable process, it has a better cash position. It positively impacts marketing, sales, customer service, and overall operations. For faster processing, the company usually adopts different methods like discounts to customers on early payment, outsourcing, and factoring debtors. For example, the company can always start a collection process early by sending reminders and can short the credit period.

Factoring services can be used in cases where an immediate cash requirement arises as the company sells its account receivable to another party at a discount and gets instant cash. Also, through outsourcing, the third party realizes payments from debtors on the company’s behalf and charges a commission for its services.

Steps

The accounts receivable process cycle individually identifies the actions a business requires to take to make the recording and maintenance of the accounts receivables accurate and reliable. Here are the four broad steps of the process flow:

Determining Credit Practices

Before allowing customers to pay at a later date, it is important for businesses to identify those who can be trusted with postponed payment. Offering goods at credit is quite risky as there are chances that the outstanding amount is never received. And this is what becomes of the major challenges of the accounts receivable process. Thus, having proper credit practices is a must.

Businesses can set up some rules to make sure credit is extended to only reliable customers and not all. A thorough credit sales process to assess customer profiles to check if they could be trusted must be there. Based on the type and nature of businesses, the companies can decide on what credit practices to adopt.

Invoicing For The Goods Sold

Preparing an invoice to note down all the goods sold to customers, the payment of which are yet to be received is highly recommended. It helps trace the money coming to the business. The invoices must have columns specifying the date of delivery of the goods and the date of expected payment. The organized invoicing makes retrieval of data when required, easier. Once the data is retrieved, businesses get details in a proper format, which makes the process hassle-free.

Tracking Payments Received

The department arranges and reconciles data to ensure businesses could easily track the payments made. This enables the companies to be aware of who is already paid and who is left. This way, they know how much money they should be expecting from which customers.

Recording Accounts Receivable Balance

Once all the payments made are recorded, the accounts receivable balances are easily recognized. As a result, businesses have a clear dataset that enables and ensure proper accounts receivable balance journal entries.

Example

ABC Pvt. Ltd. sold goods to Mark Inc. worth $ 1,000 on 15 February 2019, and the company allowed credit to Mark Inc. for three months; after that, simple interest will be charged @ 2% monthly, and if payment was received earlier than three months, then a 5% discount will be allowed.

Situation #1

As apparent, this process starts only when supply was made on credit. Inventory should be reduced with the quantity supplied. An account with the name ‘Mark Inc.’ should be created in the system to record the sale in books, and the invoice must be issued after mentioning the agreed terms.

The journal entry would be passed in the books as:

Market Inc. is shown under account receivable grouping as current assets in the balance sheet until the payment was received in the above journal entry. And sales booked are shown under an income statement.

Total Cash Flow in this situation will be Zero as the supply was made on credit.

Situation #2

Now, if payment is received before the completion of 3 months, let’s suppose 15 April 2019. Then as agreed 5% discount will be given to the customer, and the same would be recorded in books bypassing journal entry as under (hit three accounts simultaneously)

For the above entries,

- Bank/Cash – Net payment will be received after deducting a discount.

- $50 – is the expense for the company shown under the income statement

= $1000 * 5%

= $50 - $1000 – Account receivable will be zero, being the amount realized

In this situation, the total cash inflow will be $950 as the payment was realized early after the deduction of the discount.

Situation #3

If payment is not realized within three months, the company has to follow up by sending reminders for payment, and let’s suppose the amount was received on 15 May 2019, then as agreed, 2% monthly interest will be charged from the customer. It would be recorded in books bypassing journal entries as under (hit three accounts simultaneously):

For the above entries,

- Bank/Cash – Payment will be received, including late payment interest charged

- $20 – Income for the company shown under the income statement

= $1000 * 2%

= $20 - $1000 – Account receivable will be zero, being the amount realized

In this situation, the total cash inflow will be $1,020 as the payment was realized late, including late payment interest.

Situation #4

If payment is not realized for a long time, or there is no certainty of receiving the same either in full or part, then the amount shown as account receivable will be considered a bad debts to the extent of non-realization. (Bad debts, as the name advises, bad debts are the debts or accounts receivable that turn into bad).

Suppose in the above example, if Mark Inc. says that they become insolvent and can pay only 40% amount, then the remaining 60% will be booked as bad debts expense and would be recorded in books bypassing journal entry as under (hit three accounts simultaneously)

For the above entries,

- Bank/Cash – Net Payment to the extent realized

- $600 – Expense for the company shown under the income statement, or it can be deducted out of sales, and net sales/income will be shown in the income statement.

= $1000 * 40%

= $400 - $1000 – Account receivable (i.e., the account of Mark Inc. in the books of a company) will be zero as an amount realized is booked under a bank/cash account, and the amount to the extent non-realizable is being booked bad-debts expenses.

In this situation, the total cash inflow will be $400 as the remaining payment was turned into bad debts.

Improvement Ideas

The process ends when the amount is received from the customer. Based on industry trends, companies usually make supplies on credit. Therefore, companies must recognize such recoverable amounts as accounts receivables per the accounting principles. However, how fast a company can turn its receivables into cash indicates a company’s performance.

Given the significance of this process, here are the best practices that can be adopted to keep the AR smoothly flowing:

- Introduce incentives for making payments on time as promised

- Have a good rapport with customers

- Ensure clear credit rules and policies

- Make sure the data maintained is accurate

- No invoicing error should be made

- Keep things automated for a flawless AR process flow

Accounts receivable are also used for measuring various ratios. One of the critical ratios is the Accounts Receivable to Sales ratio. For example, if any company has an annual turnover of $ 1,000,000. Accounts receivables on the balance sheet date are $20,000. In this case, the company’s accounts receivable to sales ratio will be 20,000*100/1,000,000, i.e., 2.

Suppose the company has a lower ratio compared to the industry’s average ratio. In that case, it means a company can recover the amount from its customer faster than the others. Therefore, a lower accounts receivable to sales ratio is better for the company’s liquidity.

Frequently Asked Questions (FAQs)

What is the complete accounts receivable cycle?

The sale and delivery of a good or service to a customer marks the beginning of the whole cycle of accounts receivable. It’s over when that consumer pays the invoiced amount. Everything in between is crucial to ensure you get paid, on time, and with a good income stream.

What do KPIs for receivables mean?

Accounts receivable KPIs are performance indicators that show how well your company handles and collects cash. Simply said, account receivable KPIs give you an overview of how successfully you’re collecting money owed to you.

What does a monthly AR statement mean?

The Receivables Statements list each invoice, payment, and credit made during a given period to remind the account holder of their account status. Statements can be sent, emailed, faxed, or previewed.

Recommended Articles

This article has been a guide to what is Accounts Receivable Process. We explain its steps/cycle along with the improvement ideas, and how it works with an example. You can learn more about financing from the following articles –

- Is Accounts Receivable an Asset?

- Journal Entries of Accounts Receivables

- Accounts Receivables Factoring

- Notes Receivable

Recommended Articles

Continue with these closely related articles from the same guide.