Part of our Accounts Receivable guide

Advance From Customer Meaning

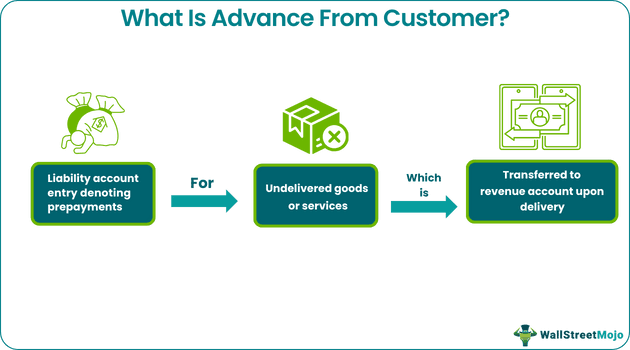

Advance From Customer refers to a current liability that records all the prepayments received from buyers before the delivery or provision of their respective goods or services. Upon delivery of such goods and services to the customer, the amount recorded under this head is transferred to the revenue account.

Any advance payment received from a customer is treated as deferred or unearned revenue since the company still needs to fulfill its obligation in exchange for this prepayment. However, such an obligation can be considered a long-term liability if the delivery of related goods or services is expected to take more than 12 months.

- An advance from customer is a company’s liability pertaining to the money received from the client for the goods or services that are deliverable in the near future.

- It is treated as deferred revenue until the goods are handed over, or the service is rendered to the respective customer.

- The advance from a customer in a company’s balance sheet is shown as a current liability, i.e., unearned revenue, if the company fulfills its obligation to deliver the goods or services within 365 days.

- However, after 12 months, such an amount is considered a long-term liability and transferred to the customer deposit account.

Advance From Customer Explained

The advance from customers is not the direct revenue of a business since the company has yet to fulfill its obligation in return. Therefore, such earnings, which will be recognized in the future at the time of delivery of the goods or services, are often considered deferred or unearned revenue. For companies, advances contribute to immediate funds, sustaining financial stability and a healthy cash flow for day-to-day business operations. Moreover, customers paying advances demonstrate a higher commitment to the transaction, reducing the likelihood of order cancellations.

Customer advances are expected in the conditions mentioned below:

- Lengthy order cycles: When the order processing cycle is long, businesses prefer to demand advance payments from customers to be assured of non-cancellation later on.

- Customized orders: When products or services involve customization, businesses may seek an advance to secure the order and cover initial costs.

- Large projects: Extensive projects with significant upfront expenses may prompt businesses to request a partial payment upfront to commence work without financial strain.

- Materials and supplies: Businesses, especially in manufacturing or construction, might need an advance to purchase necessary materials or supplies.

- Reservation or booking: In industries, for example, hospitality or event planning, an advance secures reservations and confirms the customer’s commitment. For example, businesses can use tools like AI Phone Calls to say hello to customers with personalized, automated voice greetings during the booking process, enhancing the initial interaction and reinforcing commitment to the reservation.

- Credit risk mitigation: Businesses may seek advances to mitigate the risk of non-payment, especially when dealing with new or high-risk customers.

- Service retainers: Service-based businesses might require a retainer to reserve time or resources for a customer, ensuring availability.

- Cash basis accounting: Industrial clients adhering to the cash basis accounting may opt for early payments to recognize expenses promptly, thus reducing their reportable income in the current tax year.

That said, in the event of order cancellations or delivery issues, issuing refunds for advance customer payments complicates the accounting and financial management process. Moreover, managing advance payments requires extra administrative efforts for constantly tracking and reconciling the books of accounts for revenue recognition and customer deposits. In addition, some customers may be unwilling to pay in advance, potentially resulting in lost sales opportunities.

Examples

The customer advances are often stated as unearned or deferred revenue in the company’s balance sheet. Let us now understand the journal entries made in this context and the significance of such prepayment in business:

Example #1

Suppose ABC Services Ltd. receives a $900 payment in January 2024 from XYZ Corp. for a service contract spanning from January to March 2024. ABC Services Ltd. records this $900 as deferred revenue or unearned revenue by passing the following advance from customer entry in its books:

| Date | Particulars | Debit | Credit |

| January 01, 2024 | Cash A/c Dr. To Unearned Revenue A/c(Being advance from customer received) | $900 | $900 |

As each month progresses, ABC Services Ltd. fulfills its service obligation, allowing it to recognize $300 of revenue each month ($900 / 3 months = $300 per month).

On January 05, 2024, $300 would be recognized as revenue, reducing the deferred revenue to $600. The underlying journal entry is as follows:

| Date | Particulars | Debit | Credit |

| January 05, 2024 | Unearned Revenue A/c Dr. To Revenue A/c(Being $300 recognized as revenue) | $300 | $300 |

This process repeats monthly until March 2024, when the entire $900 is recognized as revenue, and the deferred revenue becomes zero.

Example #2

Moderna Inc. surprised financial analysts by reporting an unexpected profit of 19 cents per share, defying expectations of a $1.77 per share loss. The company attributed this positive outcome to higher-than-expected revenue in the first quarter from deferred orders for its COVID-19 vaccine. While maintaining its initial forecast of $5 billion in COVID-19 vaccine sales for 2024, Moderna revealed ongoing discussions regarding potential new contracts in Europe, Japan, and the U.S., which could further enhance vaccine revenue.

Now, let us go through the following extract from the financial statements of the company:

It is seen that as of March 31, 2023, the company reports $1.8 billion in deferred revenue concerning customer deposits for scheduled vaccine delivery in 2023. Apparently, it anticipates $1.2 billion of revenue recognition within the following year. Sales recognition for COVID-19 vaccines is contingent upon factors such as product delivery, manufacturing, and marketing approval timing.

The company foresees a reduction in COVID-19 vaccine sales in 2023, attributing it to the market’s shift toward an endemic seasonal pattern. The increase in working capital by $115 million is attributed to a decrease in short-term deferred revenue and accrued liabilities, partially offset by a reduction in short-term investments by $1.2 billion, primarily for operating activities and stock repurchases. The $1.8 million deferred revenue was a result of the company’s efforts and engagement in supply agreements since 2020’s third quarter.

Journal Entry

→ Explore all 30 Journal Entries articles

In accounting, any advance payments received from customers are treated as a liability until the underlying goods are supplied, or services are offered to the respective clients. It is crucial to pass the respective journal entries for such unearned revenue to ensure accuracy, fairness, and transparency in the books of accounts. Let us now understand the various journal entries and their timelines for advance received from customers:

Step 1: Initial Recording of Customer Advances

When a business receives an advance payment from a customer, the company debits the cash or bank account to recognize the increase in funds and credits the customer’s advances or unearned revenue account as a liability, indicating the obligation to provide goods or services:

| Date | Particulars | Debit | Credit |

| – | Cash A/c Dr. To Unearned Revenue A/c(Being advance from customer received) | $ | $ |

Step 2: Revenue Recognition

On the date of delivering the goods or rendering the services, the business recognizes the customer advances or unearned revenue as sales or revenue in the books of accounts. While the customer advances or unearned revenue account is debited to decrease the associated liability effectively, the revenue account is credited with the same amount to acknowledge the sales generated through the delivery of the respective product.

That said, such revenue does not need to be recognized at once since the goods or services may be partially delivered in different timelines, emphasizing the need to pass multiple revenue recognition entries:

| Date | Particulars | Debit | Credit |

| – | Unearned Revenue A/c Dr. To Revenue A/c(Being revenue recognized) | $ | $ |

Frequently Asked Questions (FAQs)

1. How to record advance from customer in Quickbooks online?

The process of documenting customer advances in QuickBooks Online starts with verifying that the customer is listed in QuickBooks. If not, visit the Sales section and select Customers to generate a new customer profile.

The process of documenting customer advances in QuickBooks Online starts with verifying that the customer is listed in QuickBooks. If not, visit the Sales section and select Customers to generate a new customer profile.

2. Is advance from customers a debit or credit?

During the initial recording of an advance customer payment, the unearned revenue or customer advances account is credited for the amount received by the company in cash or bank account. However, while the related revenue is recognized, the customer advances account is debited for the amount transferred to the revenue account.

3. Is advance from customers treated as deposit?

Suppose the company doesn’t deliver the goods or provide the services within 12 months or 365 days. In that case, the deferred revenue or advance customer payment is shifted to the customer deposit account, which appears as a long-term liability on the company’s balance sheet.

Recommended Articles

This article has been a guide to Advance From Customer and its meaning. Here, we explain the concept along with its journal entry and examples. You may also find some useful articles here –