Part of our Accounts Receivable guide

Overview of Accounts Receivable Journal

Accounts receivables are the money owed to the company by the customers. The accrual accounting system allows such credit sales transactions by opening a new account called accounts receivable journal entry.

Accounts receivables can be considered an investment made by the business that includes both risks and returns. Returns in the form of easily acquiring new customers and risk in the form of non-payments called bad debts.

- Accounts Receivables are asset accounts in the seller’s books because the customer owes him an amount of money to pay against the goods and services already delivered by the seller. Conversely, it creates a liability account in the books of customers called Accounts Payables.

- The Balance Sheet categorizes Account Receivables as a current asset because sales made on credit are expected to get paid soon per the credit terms mentioned in the invoice issued by the seller.

- Generally, financial statements are prepared using the accrual accounting method made mandatory by both GAAP & IFRS. Accrual accounting requires recording the revenues as for and when they are earned, whether payments in cash are received or not.

- The “accounts receivable” refers to the money customers owe a company in exchange for goods or services sold. To record these sales, the company debits the accounts receivable account and credits the Sales account.

- It is an investment the business makes that includes risks and returns. Returns as quickly acquiring new customers and stakes in non-payments are called bad debts.

- When a customer buys from a seller and doesn’t pay immediately, it becomes an asset and a liability for the customer. It is recorded in accounts receivable and accounts payable, respectively.

Accounts Receivable Journal Entry

→ Explore all 30 Journal Entries articles

E.g., The Indian Auto Parts (IAP) Ltd sold some truck parts to Mr. Unreal on credit. Since IAP has already incurred various expenses called the cost of goods sold (COGS) for his sales but has not been paid.

When Mr. Unreal pays off his billing amount, the accounts receivable journal entry records the receipt of cash by reducing the accounts receivable balance. However, if payment is not received or is not expected to be received shortly, considering it to be losses, the seller can charge it as expenses against bad debts.

Let’s elaborate above example of Indian Auto Parts (IAP) Ltd and journalize the related transactions step by step:

- On Jan 1, 2019, IAP ltd sold some truck parts to Mr. Unreal on credit. The calculated amount of the invoice, including all expenses and taxes, was $10000, to be paid on or before Jan 31, 2019. Mr. Unreal made a full payment of $10000 on Jan 28, 2019.

- The accounts receivable journal entry below records the credit sale when IAP provides credit terms to its customers. Consider credit terms as 2/10 net 30i.e., if paid within ten days, a discount of 2% is offered; otherwise, payment must be made within 30 days without any discount.

Mr. Unreal pays his billing amount on Jan 8, 2019, and avails the discount.

Video Explanation of Journal vs Ledger

Accounting for Bad Debts

Once an accounts receivable journal entry is recorded for a credit sale, the company recognizes that not all debtors may pay their outstanding balances in full, resulting in bad debts. Bad debts expenses can be recorded using two methods viz. 1.) Direct write-off method and 2.) Allowance method.

#1 – Direct Write-Off Method

Bad debts provision is recorded as a direct loss from defaulters, writing off their accounts and transferring in full amount to the P&L account, thus lowering your net profit.

E.g. Mr. Unreal passed away and will not be able to make any payment.

#2 – Allowance Method

Charge the reverse value of accounts receivables for doubtful customers to a contra account called allowance for doubtful account. It keeps the P&L account unaffected from bad debts, and reporting the direct loss against revenues can be avoided. However, writing off the account at a future date is possible. For example:-

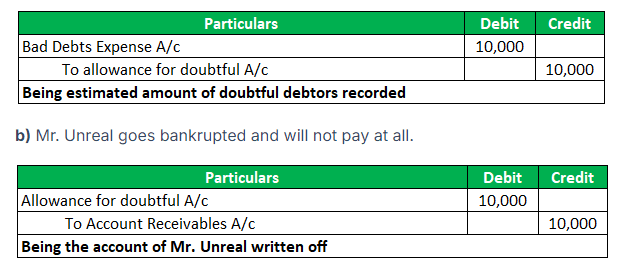

a) Mr. Unreal incurred losses and cannot make payment at due dates.

b) Mr. Unreal goes bankrupted and will not pay at all.

c) Mr. Unreal has recovered from initial losses and wants to pay all its previous debts.

Frequently Asked Questions (FAQs)

How to decrease accounts receivable journal entries?

The provision for doubtful accounts in the contra-asset account is deducted to write off bad debt. The likelihood that the firm will never receive payment for that loan will decrease the number of account receivables on the balance sheet.

Is accounts receivable a debit or credit?

Accounts receivable is an amount of money owed to a business by an individual or entity, recorded as a debit.

What are the four functions of accounts receivable?

Building monthly financial statements, doing account reconciliations, producing invoices and account statements, and managing the billing system are some of the many tasks an accounts receivable department carries out.

What is the importance of managing accounts receivable?

Managing accounts receivable is crucial for maintaining healthy cash flow and ensuring the financial stability of a business. Efficient AR management helps to reduce the risk of bad debts, improves collection times, minimizes the need for borrowing, and provides funds for business operations and investments.

Recommended Articles

This has been a guide to Account Receivables Journal Entry. Here we discuss the overview of Accounts Receivables, journal entries examples, and we will also discuss the Effects of credit sales on inventory and its balance. You can learn more about firms from the following articles –