Part of our Time Series Analysis guide

What Is An Autoregressive Model?

An autoregressive model is a process used to predict the future based on accumulated data from the past. It is possible because there is a correlation between the two. Such a model can represent any random procedure where the output is dependent on any previous values.

This model is often used to predict the future trend in stock prices by analyzing past performance. Thus, it assumes that the future result will be similar to the previous years. However, this is only sometimes acceptable because, due to continuous global technological and economic changes, there is no guarantee that the future will reflect the past.

Key Takeaways

- An autoregressive model is a method of forecasting the future based on past values.

- It assumes that the past and future data are perfectly correlated and that the past will accurately reflect the future.

- The model helps in future stock price calculation using the prices analysis from past data.

- This model is not a dependable source of information because, due to continuous economic and technological changes worldwide, it is difficult to assume that the past will accurately reflect the future.

Autoregressive Model Explained

The autoregressive (AR) model predicts the future based on past data or information. It helps in stock price forecasting on the assumption that the prices of previous years will genuinely reflect the end. Because AR frameworks are widely used across statistics, finance, and machine learning, many modern resources explore the foundations of an autoregression model to help practitioners understand how past values influence future predictions in time-series analysis.

In an autoregressive model time series is calculated based on the correlation of past and future data. So, it is a statistical method for any fundamental or technical analysis. But the downside of this model is the assumption that all forces or factors that affected past performance will remain the same, which is unrealistic since change is inevitable in all fields. There is a rapid transformation all around due to endless innovation taking place.

A vector autoregressive model, for instance, consists of multiple variables that attempt to correlate a variable’s present values with its past values and the system’s past data of other variables. Thus, it is a multivariate model. If an AR model is univariate, it is impossible to get a two-way result between the variables.

The use of the autoregressive process to make forecasts is very significant. However, these models are also stochastic, meaning they have an element of uncertainty. Any unforeseen contingency or sudden change and shift in the economy will affect the outcome of future values significantly, which refers to the fact that the result will never be accurate. Nevertheless, it is possible to get the closest possible outcome.

A first-order autoregressive model assumes that the immediately previous value decides the current value. However, there might be cases that the present value will depend on two previous values. Thus, in an autoregressive model, time series plays an important role and is used depending on the situation and desired result.

Formula

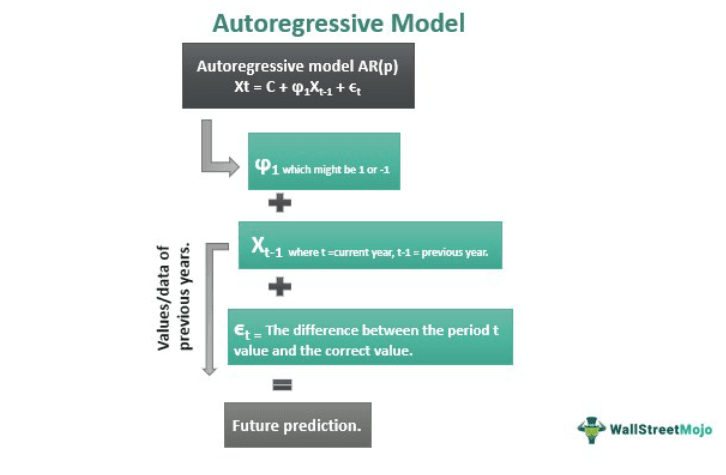

Let us try to understand the autoregressive model equation as mentioned below:

In this model, some specific values of Xt serve as variables. They have lagged values, which means the past or current output will affect future outcomes.

The autoregressive model equation, denoted by AR(p), is given below:

Xt = C + ϕ1Xt-1 + ϵt

where,

- Xt-1 = value of X in the previous year/month/week. If “t” is the current year, then “t-1” will be the last.

- ϕ1 = coefficient, which we multiply with Xt-1. The value of ϕ1 will always be 1 or -1.

- ϵt = The difference between the period t value and the correct value (ϵt = yt – ŷt)

- p = The order. Thus, AR (1) is first order autoregressive model. The second and third order would be AR (2) and AR (3), respectively.

Examples

Here we look at some examples to understand the concept.

Example #1

John is an investor in the stock market. He analyses stocks based on past data related to the company’s performance and statistics. John believes that the performance of the stocks in the previous years strongly correlates with the future, which is beneficial to making investment decisions.

He uses an autoregressive model with price data for the previous five years. The result gives him an estimate for future prices depending on the assumption that sellers and buyers follow the market movements and accordingly make investment decisions.

Example #2

The concept of AR models has gained importance in the information technology field. Google has proposed Autoregressive Diffusion Models (ARDMs), which encompass and generalizes the models that depend on any data arrangement. It is possible to train the model to achieve any desired result. Thus, this method will generate outcomes under any order.

Example #3

The autoregression process can be helpful in the veterinary field; also, the main focus is on the occurrence of a disease over time. In this case, the primary source of information is the systems used to monitor and track the details of animal disease. This data is analyzed and correlated using the model to understand the possibility of any disease occurrence. However, this model has limited use in the veterinary field due to limited data availability and the need for useful software to generate the best results.

Autoregressive Model vs Moving Average

Autoregressive Model

- Use of past data as input.

- The various time slots impact the time.

- It calculates the regression of past time series.

- It puts data from the previous time in the regression equation to get the next value.

- The correlation between the objects of the time series decreases as the time gap increases.

Moving Average

- Use of past errors as input.

- Some external factors affect the period.

- It calculates the residuals or errors of past time series.

- It states that the next value will be the average of all the past values.

- The correlation between the objects of the time series at different points in time is zero.

Frequently Asked Questions (FAQs)

Are autoregressive models stationary?

Depending on specific parameters, an AR model may be stationary or non-stationary. For example, if it is a case of a first order model, where p = 1, if the coefficient is less than one, then the model will be stationary; otherwise, it is non-stationary.

How to interpret autoregressive model?

The AR model is used to forecast the future by using past data. The model presumes that past values will reflect the future. For example, if we look at the equation Xt = C + ϕ1Xt-1 + ϵt, then the model can be interpreted as the value of a period Yt is equal to a part ϕ1 of the previous period Xt-1 plus an unpredictable shock ϵt.

How to use vector autoregressive model?

This model is useful when more than one time series can influence each other. They can be called bi-directional and multivariate and contribute to natural sciences and economics. For example, it helps estimate any economic relationship, like the influence of GDP and the policy rate of a country on each other. It is also valuable for finance and health research.

Recommended Articles

This article has been a guide to what is Autoregressive Model. Here, we explain it in detail with its formula, examples, and difference from the moving average. You may also find some useful articles here –