Part of our General Ledger guide

Examples of Bookkeeping

The following example outlines the most common types of bookkeeping – Single & Double Entries. Bookkeeping is the systematized recording of financial transactions of a company. It is a recording of day-to-day financial transactions of the business. Bookkeeping brings the books of accounts to the stage where trial balance can be generated. The company’s profit & Loss statement and Balance sheet are prepared from the data recorded in the bookkeeping process.

Types of Bookkeeping with the Examples

The following are the types of bookkeeping with examples.

Single Entry System

In the single entry system of bookkeeping, financial transactions are recorded as a single entry in books of accounts. This system follows the cash basis of accounting, so the important information captured in this system is cash receipts and payments. Assets and liabilities are usually not captured in a single entry system. The single entry system is used for manual accounting systems.

Bookkeeping Example

ABC Corp maintains its books of accounts in a single entry bookkeeping system. The following are the financial transactions in July.

Analysis

In the above-presented case of “ABC Corp.,” only the cash receipts and payments have been considered in the single entry system. Consequently, the corresponding assets or liabilities are not considered in the books.

This system helps ABC Corp to keep track of its cash flow position on a day-to-day basis. However, it can be considered useful only if all the financial transactions happen in cash. If there are any receivables or payables, then tracking the same will be severe in a single entry system as assets and liabilities are not captured.

Double Entry System

In a double-entry bookkeeping system, accounting transactions[ affect two ledger accounts because every entry to an account requires a corresponding entry in another account. The entries may impact the asset, liability, equity, expense, or revenue account. The double entry system has two corresponding sides, known as Debit and Credit. This system follows the accrual basis of accounting.

Accounting Equation:

Assets = Equity + Liabilities

In the double-entry system of bookkeeping, the total amount of assets should always be equal to the total amount of Equity & liabilities at any point in time.

Bookkeeping Example #1

In January 2019, Sam started his business ABC, Inc. The first transaction that Sam recorded for his company was his investment of $50,000 in exchange for 10,000 shares of ABC’s stock. As a result, ABC Inc.’s accounting system increases its cash account by $50,000 and its shareholders’ equity account by $50,000. Both of these accounts are balance sheet accounts.

After Sam enters this transaction, ABC Inc.’s balance sheet will look like this:

Analysis

In the present case, the financial transactions of ABC Inc. are captured from its incorporation. In the double-entry system, every effect in the transaction is captured (i.e.) both debit and credit. When Sam started the business, he invested cash of $50,000 in return for which he got the shares of ABC Inc.

Both asset and liability have been given effect, unlike the single entry system. Since all transactions are recorded entirely, it helps to understand the overall position and performance of the organization. This system helps prepare both Balance sheets and Profit & Loss statements for the business. It gives a proper audit trail.

Bookkeeping Example #2

Joe purchased a car worth $50,000. He made payment for the same from his bank A/c. The financial transaction is recorded as follows:

Analysis

In this case, Joe purchased a car by paying $50,000. In double-entry, both the asset bought (i.e.) Car has been added, and the corresponding reduction from the bank balance has been recorded entirely.

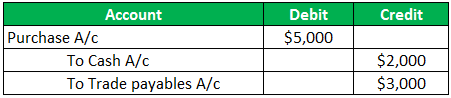

Bookkeeping Example #3

Hannah purchased raw materials for her business for $5,000. She paid $2,000 in cash, and the remaining $3,000 shall be paid after the credit period of 30 days.

After 30 days, Hannah paid the balance of $3,000 to the vendor.

Analysis

Here, the purchase of raw material for $5,000 is recorded, with the cash payment of $2,000, and trade payables of $3,000 are captured. The double-entry system helps track all the credit transactions and helps us know the business’s fund requirements as the credit transactions need to be settled after the due date. It acts as a check for the cash flow position of the business.

Bookkeeping Example #4

X Corp provides consultancy services. They have the credit policy that 50% of the payment shall be paid on receipt of service, and the remaining 50% shall be paid post-credit period of 15 days. They have charged a customer $1,500 for the services rendered.

After 15 days, X Corp receives the remaining 50% payment from the customer.

Analysis

In this case, X corp. Renders service gets paid 50% and gives a credit period of 15 days for the remaining 50% to its clients. The double-entry system captures both the cash receipt for the services rendered and payments to be received from the client after credit days. This system helps keep track of the trade receivables and helps follow up with the appropriate clients.

Conclusion

Bookkeeping is vital for all business models. For example, if proper tracking of financial transactions doesn’t happen, it leads to business failure due to improper financial management. Moreover, as per the present laws, bookkeeping is a must to meet the requirements of audits, tax obligations, etc.

It helps in financial planning for the business. Investors will get a clear picture of how their funds are being utilized. Overall, bookkeeping plays a vital role in the progress and performance of the business.

Recommended Articles

This article is a guide to Bookkeeping Examples. Here we discuss single entry and double-entry bookkeeping types and examples and detailed explanations. You can learn more from the following articles –