Part of our Balance Sheet guide

What Is A Cash Receipt?

A cash receipt is a printed acknowledgment of the cash received during a transaction involving the transfer of money or cash equivalent. The original copy of this receipt is given to the customer, while the seller keeps the other copy for accounting purposes.

In other words, it is generated when a vendor accepts cash or cash equivalent from an external source, such as a customer, an investor, or a bank. Usually, the cash is acknowledged when money is taken from a customer to adjust the outstanding accounts receivable balance generated when the credit sale transaction happened. Therefore, it can be seen as a collection of money that increases the cash and cash equivalent balance on its company’s balance sheet.

Cash Receipt Explained

A cash receipt is not only used as a proof of ownership but also used for various other purposes. For example, there are instances where the retailer would ask a customer to produce the cash receipt so that the exchange or return of purchased items can be approved. In the case of product warranty, the vendor may ask for the receipt issued at the time of product sale.

Another primary but essential benefit is the completeness of the accounting records that support the existence of recording transactions. One of the significant reasons for an audit is the lack of documents (such as cash receipts). This is because such credentials support the presence of the transaction. Having such receipts and proper filing will avoid the risk of audit issues. Without these receipts, the accounting record is incomplete, which can be risky in the long run.

Also, a receipt asked during purchases or payments can be validly used to claim as an expense and then utilized as a sales tax deduction if the purchaser is a sales tax registered. If the benefit of input tax (sales tax on expenses) exceeds the output tax (sales tax on sales), then the vendor can claim a refund on the excess or difference.

Another importance of cash receipts is that, at certain times, they can also be useful for tax purposes. It can be used to minimize or decrease tax payable legally. Since it can be used as expenses deducted from sales, it will reduce the payment due to lower net income.

Template

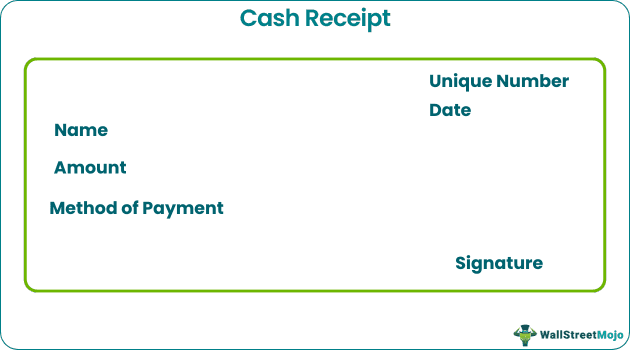

A cash receipt is prepared keeping in mind certain considerations, which becomes the standard cash receipt format. Inherently, the following information features in this receipt:

- The date on which the transaction happened

- The unique number assigned to the document for identification

- The name of the customer

- The amount of cash received

- The method of payment, i.e., by cash, cheque, etc.;

- The signature of the vendor

Examples

Below we have taken some examples of cash receipt journals.

Example #1

Let us take an example of a cash sale transaction.

Let us assume that a lemonade stand has been set up in the neighborhood during the summer to cater to customers during the weekends. It is a plain vanilla business model where the vendor sells a glass of lemonade for $5 to expect customers to pay the money immediately.

The lemonade vendor does not sell any glass of lemonade on credit; instead, an immediate cash receipt is recognized with the sale (debit the cash account, credit the sales account). In this example, the vendor sells each glass of lemonade against a $5 cash payment from the customer, and then the vendor issues the cash receipt to the customer.

Example #2

Now let us look at an example associated with a credit sale that results in receivable.

Let us assume that there is a big distributor of televisions who sells a variety of different brands of TV. The distributor has been in the business for a long time and has a strong business network. The distributor purchases the televisions from numerous television manufacturers. Due to the long-standing relationship, the distributor offers favorable credit terms that allow him to order televisions as and when required. The credit period provided is for 30 days. In this example, a television manufacturer would record a sale to the distributor after shipping the televisions to him; however, this is not when the manufacturer would record the receipt.

Instead, the manufacturer would record the sale transaction in the income statement and recognize a balance in the balance sheet, which is due in 30 days (debit the receivable account, credit the sales account). The receipt would be finally issued only when the actual payment is realized in cash or cheque. In that case, the outstanding receivable balance reduces, and the cash balance would increase (debit the cash account, credit the receivable account).

Cash Receipt Vs Cash Disbursement

To understand the cash receipt meaning, it is important to check out how it is different from cash disbursement. Let us look at some of them:

- Both cash receipt and disbursement are part of cash controls that organizations deploy to keep track of its cash flow.

- Cash receipts identify the money to be received after the sale of goods and services. On the other hand, cash disbursement is the amount paid out for purchasing items to be used by the company.

- Each cash receipt activity should be documented such that the number of items purchased matches the value paid for it. On the contrary, the examples of cash disbursements include paying for raw materials, inventory, etc.

Recommended Articles

This article has been a guide to what is Cash Receipt. Here we explain its template along with examples, and its differences with cash disbursement. You can learn more about accounting with the following articles –