Part of our Accounts Payable & Receivable guide

Top 2 Practical Examples of Cash Book Entries

The following Cash Book examples outline the most common Cash Books. Cashbook is a financial journal that contains all the cash receipts and cash payments, including the deposit in the bank and withdrawals from the bank. Here all transactions have two sides, i.e., debit and credit. All the cash receipts are recorded on the left side of the cash book entries, whereas all the payments in cash are recorded on the right side. The difference between the sum of balances on the right and left sides shows the cash on hand. There are various examples of the Cash Book entries followed according to the different situations by different companies. In this article, we take two types of examples of cash books – Single Column and Double Column.

Top 2 Practical Examples of Cash Book Entries

Some of the examples of Cash Book entries are shown below in different situations:

Example #1 – Single Column

Under a single column cash book, only cash transactions are done by the business record. Therefore, it has only a single money column on debit and credits on both sides, titled “amount.” As it records only the accounting transaction related to cash, entries that involve banks or discounts such as checks received, checks issued, sales discounts, or purchases discount does not record.

For example:

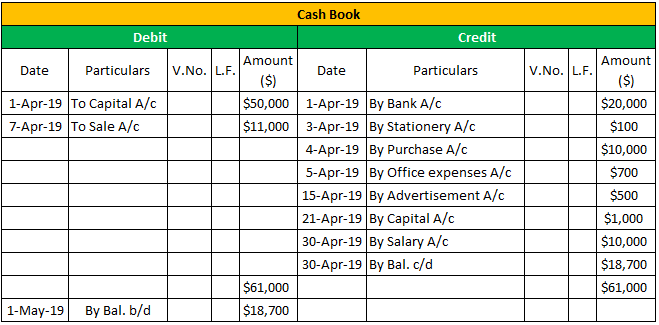

Mr. Y started the business with a capital of $ 50,000 on April 1, 2019. Out of the capital invested, $ 20,000 is deposited in the bank account on the same day. On April 19, he identified the following transactions. Prepare the necessary single column Cash-book using the data as given below:

Solution

Example #2 – Double Column

The transactions done on credit do not record in the cash book. So the transactions Purchased from Mr. X on credit and Goods sold on credit on April 18 are not considered while preparing the cash book entries.

In the present modern world, almost all transactions done are using the company’s bank account. So, it was required to present one more column to the single-column cash book. For this double column cash – the book is used. Under double-column cash books, cash transactions and transactions through banks done by the business are also recorded.

For example:

Mr. X runs a business. On April 19, the following transactions took place in the business. Prepare the necessary double-column Cash-book using the data given below:

Solution

The transactions done on credit are not recorded while preparing the double column cash–book. In the case of double column cash book, the cash column records all the transactions relating to cash, so it works as the cash accounts, and the bank column records all the transactions about the bank, such as checks received, checks issued, etc. So, it works like a bank account.

Conclusion

Cashbook is prepared like a ledger where the company’s cash transactions are recorded and entered according to date. It is a book containing the original entry and the final entry, which means that the cash book serves as the general ledger. In the case of a cash book, there is no requirement of a balance transfer to the general ledger, which is required in the case of the cash account. Entries in the cash book are posted then to the corresponding general ledger.

Recommended Articles

This article has been a guide to Cash Book Examples. Here we discuss various examples of the cash book entries (single and double columns) and provide a detailed explanation. You can learn more about financing from the following articles –